1-888-601-9980

1-888-601-9980The Best Life Insurance in Canada: Company Reviews (2024)

We’ve rated the Best Life Insurance Companies in Canada to help you figure out which provider you should choose. We looked at overall performance and features like the best options for couples and families, no-medical options, and more. Use this list as a guide to help you compare and shop for the best life insurance policy in Canada.

The best life insurance companies in Canada include Manulife, Canada Life, Desjardins, Empire Life, BMO, RBC, and more.

Each company has their own benefits and features that can suit different needs.

That’s why we’ve reviewed and rated the top providers to bring you our list of the 16 Best Rated Life Insurance Companies in Canada.

What are the best life insurance companies in Canada?

After careful research, our expert insurance advisors have created a list of the best companies for term life insurance in Canada.

We have years of experience profiling and analyzing the best of what the industry has to offer. In this article, our team of experts have provided real insight on different life insurance providers and how they can meet your needs.

The following list of the top life insurance companies in Canada will help you to expertly compare and choose your best term life insurance options.

List of Top 16 Best Term Life Insurance Companies In Canada

The best life insurance company for you depends on your unique needs. But, if you’re looking for term life insurance coverage, our team recommends:

- Assumption Life: Best for simplified issue

- Beneva: Best for combo coverage

- BMO: Best for affordability

- Canada Life: Best for financial strength

- Canada Protection Plan: Best for non-medical

- Desjardins: Best for stability

- Empire Life: Best for personalization

- Equitable Life: Best for families

- Foresters: Best for giving back

- Humania: Best for quick issue

- Industrial Alliance: Best for flexibility

- ivari: Best for layering

- Manulife: Best for digital innovation

- RBC: Best for value for money

- Sun Life: Best for buying in-person

- Wawanesa: Best for price

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

Ratings and reviews of the top rated life insurance companies in Canada

Best for Simplified Issue: Assumption Life

Our Assumption Life rating and review:

We’ve given Assumption Life Insurance Company 5 stars and rated them as the best life insurance provider for Simplified Issue policies. These policies do not ask you to do a medical exam, but may have some simple medical questions on the application.

Assumption Life offers 4 different types of non-medical policies, making them a great option for people who may have health issues. You can also get bigger amounts of coverage if you opt for full underwriting.

Assumption Life pros and cons

| Pros | Cons |

|---|---|

| Multiple term coverage options | Wide range of options can be confusing |

| Simplified, non-medical issue options available | High policy fees and rider fees on non-medical policies |

| Quick, easy electronic process | |

| Decreasing option available for mortgage coverage | |

| Online access to account | |

| Digital e-policy | |

| Exchange and conversion options to convert to longer term products or permanent coverage |

Best for Combo Coverage: Beneva

Our Beneva rating and review:

We’ve given Beneva Life Insurance 4 stars and rated them as the top provider if you want combined coverage. Their insurance products, riders, and features let you get a lot of different types of insurance in one place.

Beneva is rare in that they include an Extreme Disability Benefit for free in all of their life insurance plans. You get double the coverage than usual, and that’s unique!

Beneva pros and cons

| PROS | CONS |

|---|---|

| Built-in Extreme Disability Benefit (rare in the market) | Longer turnaround times for policy approval |

| Options to add critical illness and monthly disability indemnity for comprehensive financial protection | |

| Several optional riders: accidental death and dismemberment and children’s term coverage | |

| Preferred rates available starting at $250,000 | |

| Online access to account | |

| Digital e-policy | |

| Top 10 largest insurance company based on annual premiums |

Best for Affordability: BMO Insurance

Our BMO Insurance rating and review:

We’ve given BMO Insurance 5 stars and rated them as the best company if you’re looking for affordable coverage. Most of their policies have good prices and can be used for multiple purposes.

BMO’s term life insurance is a great option for just about anyone — individuals, couples, or business owners. On top of their great pricing, their plans cover most of the standard features expected in a life insurance plan in Canada.

BMO Insurance pros and cons

| PROS | CONS |

|---|---|

| Great value for cost | No online account |

| Multiple term coverage options | Only issues paper policies, no digital option |

| Can exchange 10-year term into longer term products | Longer-term life insurance policy (25 and 30-year) not renewable |

| Compassionate benefit program — death benefit advance in event of terminal illness | |

| Options to convert into permanent coverage | |

| Electronic contract delivery | |

| Multi-policy discount available | |

| Top 10 largest insurance company based on annual premiums |

Best for Financial Strength: Canada Life

Our Canada Life Insurance rating and review:

We’ve given Canada Life Assurance Company 4 stars and rated them as the top choice for financial strength. Which is to be expected considering they’re the biggest insurance companies in Canada.

Canada Life earns billions in annual premiums, with $396 billion in assets and a financial strength rating of A+ from A.M. Best. They’re extremely stable, and they have great life insurance policy options to boot.

Canada Life Insurance pros and cons

| PROS | CONS |

|---|---|

| Multiple term coverage options (5-50 years) | Minimum $100,000 coverage or $500 annual premium required |

| Multiple rider options for single and joint policies | Limited access to online account features |

| Options to convert into permanent coverage | |

| Digital e-policy | |

| Top 10 largest insurance company based on annual premiums |

Best for Non-Medical Policies: Canada Protection Plan

Our Canada Protection Plan rating and review:

We’ve given Canada Protection Plan 5 stars and rated them as the best provider for No-Medical policies. These plans do not ask you for a medical test or have medical questions, but usually cost a bit more.

Like Assumption Life, Canada Protection Plan also gives you great options if you’re looking for life insurance coverage without doing medicals. They have both simplified or guaranteed insurance policies available.

Canada Protection Plan pros and cons

| PROS | CONS |

|---|---|

| Multiple products offering simplified, no-medical coverage | Premiums can be more expensive than competition |

| Most products available through an easy online application without any medical tests | Max. coverage of $1 million |

| Multiple term coverage options | Coverage ends at age 80 (most other Canadian providers end at 85) |

| Affordable premiums, including no-medical policies | |

| Available to temporary residents such as those on a student or work visa | |

| Most plans offer life protection | |

| Customers can pay annual premiums by credit card | |

| Options to convert into permanent coverage | |

| Decreasing term option available (ideal for covering mortgage debt) | |

| Digital e-policy |

Best for Stability: Desjardins Insurance

Our Desjardins Insurance rating and review:

We’ve given Desjardins 4 stars and rated them as the best company for stability. Saying that they’re a well-established company would be putting it too mildly.

Desjardins is one of Canada’s top ranked life insurance companies and financial groups, one of the biggest and oldest providers, and one of the world’s 50 safest banks and financiers. Their term life products can meet a wide range of needs.

Desjardins pros and cons

| PROS | CONS |

|---|---|

| Several optional riders and benefits | Limited term options |

| Robust suite of critical illness, disability, and permanent life insurance available | Premiums can be more expensive than competition |

| Allows multiple applicants on the same policy; 1 policy can cover the needs of an entire family | |

| Options to convert to permanent coverage | |

| Multi-policy discount available | |

| Digital e-policy | |

| Top 10 largest insurance company based on annual premiums |

Best for Personalization: Empire Life

Our Empire Life rating and review:

We’ve given Empire Life 5 stars and rated them as the best insurer for personalization. They give you a lot of leeway to choose the options that work best for you. This is flexible and affordable coverage that can suit many Canadians perfectly.

Their Solution series offers 10-year, 20-year-, or 30-year term insurance, or permanent insurance that covers you up to age 100. Or you can get an annual renewable term that lasts for 1-year increments.

Empire Life pros and cons

| PROS | CONS |

|---|---|

| Some of the most versatile coverage options in Canada | Limited term options |

| Options to exchange into longer term coverage | Max. annual renewable term coverage of $499,999 |

| Instant approval possible | |

| Highly competitive premiums | |

| Comprehensive rider options | |

| Solution 100 term policy has cash value (rare in the market) | |

| Online access to account | |

| Digital e-policy |

Best for Families: Equitable Life

Our Equitable Life rating and review:

We’ve given Equitable Life 4 stars and rated them as the best company for families. They make it easy for you to add coverage for multiple people on one policy. This helps families save on fees and put some cash back in their wallets.

It’s also great for a strategy called “laddering”, where you only pay for coverage as you need it. This is another way Canadians can save a little bit more on their life insurance coverage.

Equitable Life pros and cons

| PROS | CONS |

|---|---|

| Options to add critical illness insurance and other term life riders | Limited term options |

| Options to convert into permanent coverage, regardless of health | Moderate premium costs |

| Preferred clients automatically qualify for EquiLiving critical illness insurance | Limited term offerings |

| Can create family plan by adding child term rider | |

| Online access to account | |

| Digital e-policy | |

| Top 10 largest insurance company based on annual premiums |

Best for Giving Back: Foresters Financial

Our Foresters Financial rating and review:

We’ve given Foresters Financial 4 stars and rated them as the best company for giving back. Many of their products come with a unique perk: a charitable benefit feature where they will donate to a charity of your choice on your behalf.

Foresters is also a great choice if you have changing needs. Their term insurance is simple and straightforward, but they also have options that give you better coverage if your needs change in the future and you need insurance to match that.

Foresters pros and cons

| PROS | CONS |

|---|---|

| Multiple term coverage options | Premiums can be more expensive than competition |

| Simplified and quick fulfillment options available | No online access to policy details |

| Options to convert to permanent coverage, including participating and non-participating | |

| Unique community membership benefits | |

| Digital e-policy |

Best for Quick Issue Options: Humania

Our Humania Assurance rating and review:

We’ve given Humania Assurance 4 stars and rated them as the best company for quick issue policies. Their main term life insurance product is designed to make it easy for you to get approved fast.

Humania’s policies usually don’t have many requirements. Most are done online and can be approved on the spot. They also let you choose coverage for multiple terms, up to a maximum of 30 years or until age 80.

Humania pros and cons

| PROS | CONS |

|---|---|

| Competitively priced premiums | No preferred pricing available clients in better health |

| Multiple term coverage options | Conversion only available until age 65 |

| Options to exchange into longer term products | No online access to policy details |

| Simplified and quick fulfillment options available | Term coverage only available until age 80 |

| Digital e-policy | |

| Non-medical coverage options available | |

| Automatic approval for critical illness and debt disability coverage for those with standard health |

Best for Flexibility: Industrial Alliance

Our iA Financial Group rating and review:

We’ve given Industrial Alliance (iA) 5 stars and rated them as the best for flexibility. They’re one of the few insurers that lets you customize your term length with their unique Pick-A-Term product.

You can pick anywhere between 10-40 years for term coverage with iA Financial Group, letting you match your term insurance with any specific number of years, like if you’re using life insurance to cover your mortgage.

Industrial Alliance pros and cons

| PROS | CONS |

|---|---|

| Flexible plans allow personalized coverage | Premiums can be more expensive than competition |

| Pick-a-term feature (rare in the market) | |

| Both level and decreasing options | |

| Optional disability rider — can be used with decreasing coverage for mortgage protection | |

| Non medical coverage options: simplified and guaranteed | |

| Online access to account | |

| Digital e-policy | |

| Underwriting can be more accommodating than competitors | |

| Top 10 largest insurance company based on annual premiums |

Best for Layering: ivari

Our ivari rating and review:

We’ve given ivari 3 stars and rated them as the best provider if you want to do a layering strategy. Laddering is when you buy multiple term life policies that end at different times. You can terms of 10, 20, or 30 years with this company.

ivari makes it easy for you to get multiple policies that overlap, so you can create custom coverage that is just perfect for you. You can get just one term life policy, or you can combine policies with more terms or different types of insurance.

Ivari pros and cons

| PROS | CONS |

|---|---|

| Several optional riders, including children’s insurance | Premiums can be more expensive than competition |

| Multiple term coverage options | Limited flexibility for term length |

| 30-year term has flexible options upon maturity | |

| Online access to account | |

| Digital e-policy |

Best for Digital Innovation: Manulife

Our Manulife rating and review:

We’ve given Manulife 5 stars and rated them as the best for digital innovation. This company almost needs no introduction. It’s one of the biggest insurers not just in Canada but in the entire world — an industry leader in every sense.

Manulife was one of the first companies to take more of the life insurance process online in Canada. Their underwriting uses advanced technology to approve up to $2 million in life insurance without needing a medical exam.

Manulife pros and cons

| PROS | CONS |

|---|---|

| Offers a fully electronic, digital fulfillment | Limited term options |

| Digital e-policy | Premiums can be more expensive than competition |

| Offers cash advance in event of terminal illness | |

| Options to exchange into longer term products | |

| Option to increase coverage up to 5th anniversary of certain term policies (rare in the market) | |

| Top 10 largest insurance company based on annual premiums |

Best for Value For Money: RBC Insurance

Our RBC Insurance rating and review:

We’ve given RBC Insurance 5 stars and rated them as the best company if you want value for money. They have some of the most competitive premiums in the Canadian life insurance market.

RBC Insurance offers a best-in-class term life insurance product. They already beat the competition on price alone. And you can choose from different term lengths and coverage amounts.

RBC pros and cons

| PROS | CONS |

|---|---|

| Affordable premiums — among the most competitive in the industry | Only available to Canadian citizens and permanent residents |

| Max. coverage of $25 million | |

| Flexible term lengths and coverage amounts | |

| Pick-a-term feature (rare in the market) | |

| Flexibility allows for insurance laddering | |

| Multiple rider options | |

| Renewable term life policies | |

| Quick, easy application process: just 10 questions for coverage under $1 million | |

| Online access to account | |

| Digital e-policy | |

| Top 10 largest insurance company based on annual premiums |

Best for In-Person Purchase: Sun Life Financial

Our Sun Life Insurance review and rating:

We’ve given Sun Life Insurance 3 stars and rated them as the best for buying in-person. Their products are most often sold in-person through a professional like an insurance broker or advisor.

Sun Life’s term policies have standard features and optional benefits that can compete in the market. But their premiums may cost more than some other companies charge.

Sun Life pros and cons

| PROS | CONS |

|---|---|

| Multiple rider options | Limited term options available (only 4) |

| Multiple options to convert to permanent coverage up to age 75 (most competitors stop at age 70 or 71) | Limited flexibility for term length |

| Non-medical coverage options available | Premiums can be significantly more expensive than competition |

| Max. coverage of $1 million for anyone legally living in Canada — not just citizens and permanent residents | Stricter underwriting process for pre-existing health conditions |

| Online application process | |

| Digital e-policy | |

| Top 10 largest insurance company based on annual premiums |

Best for Price: Wawanesa

Our Wawanesa rating and review:

We’ve given Wawanesa 4 stars and rated them as the best for price. Their premiums are often among the lowest in the industry, and you get your pick of either term policies from 10-30 years or up to age 80.

Wawanesa can also be a good option if you want to layer your coverage. You can get a base term plan then add up to four term life insurance riders with different term lengths. You can do this all in one policy.

Wawanesa Life pros and cons

| PROS | CONS |

|---|---|

| Multiple term coverage options | Longer turnaround times for policy approval |

| Affordable premiums — among the most competitive in the industry | Policies can only be converted into non-participating permanent products |

| Range of coverage options allows for insurance laddering | |

| Renewable term life policies | |

| No policy or rider fees | |

| Coverage up to $500,000 approved without medical exam for those under age 45 | |

| Digital e-policy | |

| Top 10 largest insurance company based on annual premiums |

Methodology: How did we rank life insurance companies?

Our life insurance company rankings were the result of in-depth research into key factors like:

- Coverage amounts

- Term lengths

- Premium rates

- Application process

- Online access

- Rider options

- Key features

- Financial strength rating

- And more

Our team of licensed insurance advisors worked together to carefully assess the different policies available in Canada. Using this, we narrowed down a list of the best insurance company for life insurance products that meet diverse needs.

Which insurance company should I choose?

You should choose an insurance provider whose products:

- Meet your needs

- Offer you value in a way that works just right for your family

We can’t recommend a catchall provider as the ultimate best life insurance company in Canada because it depends on your unique needs. That’s why we researched and wrote the reviews in this article, so you can take a look at what they’re offering and decide for yourself which one you want to work with.

But, if you need help, give us a call! A licensed expert at PolicyAdvisor.com will be happy to listen to your needs and help you find your ideal match.

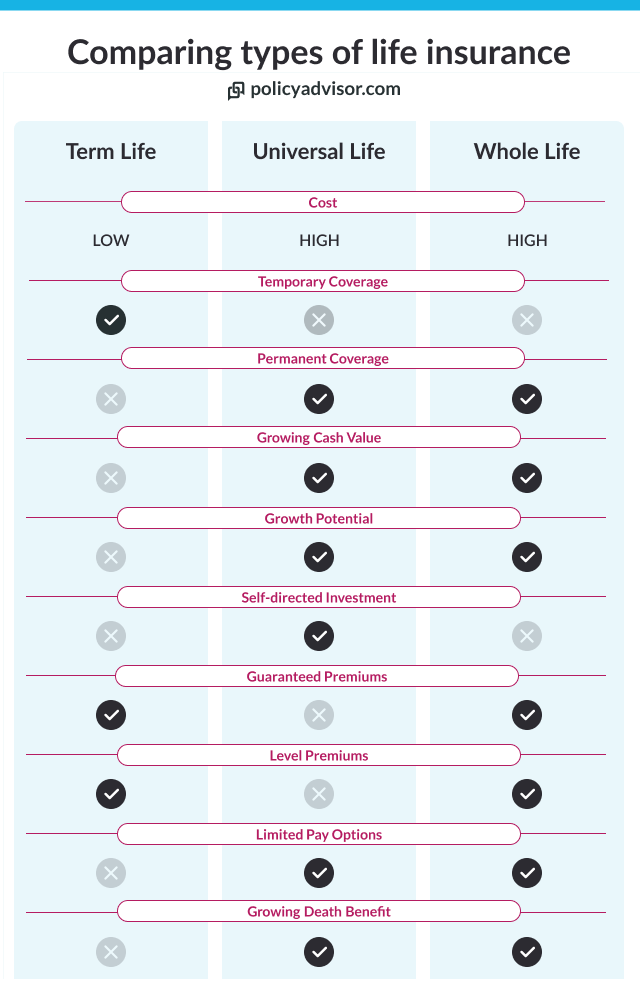

What’s the best type of life insurance?

The best type of life insurance policy again depends on your own circumstances, needs, and goals. It will be different for everyone. For example:

- Term life insurance — Best for you if you’re fairly young and you have short-term needs. Many Canadians choose this option.

- Whole life insurance — The best type of insurance for you if you want lifelong coverage, and you want to earn a little extra savings too. This type of policy comes with an investment component you can use during your life.

- Universal life insurance — Might be best if you want lifetime coverage like a whole life policy, but you want to manage the investment component yourself.

- No-medical life insurance — Best if you have health concerns or you don’t want to answer a lot of medical questions.

If you’re unsure, book some time with one of our licensed advisors to get expert advice on which type of policy would best fit your needs.

How to get the best term life insurance Canada?

You can find the best insurance policies for your needs on PolicyAdvisor.com. Check out our recommendations below then use our platform to compare quotes from Canada best life insurance companies in under a minute.

Our platform lets you shop the best prices from more than 30 of the country’s best providers. Compare policies at a glance, so you can easily make the best choice for your family.

Or, if you prefer to speak to a professional, book a call with one of our licensed insurance agents. We’re happy to help and you have no obligation to buy!

Frequently asked questions

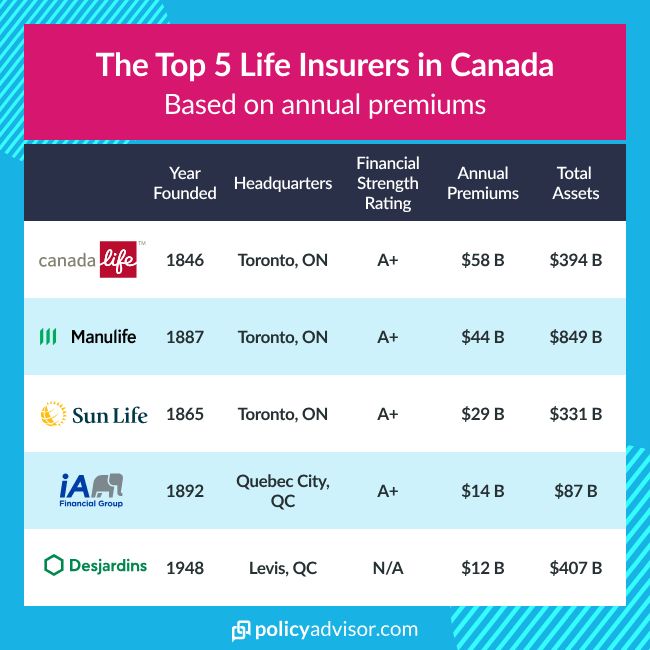

The top 5 life insurance companies in Canada are Canada Life. Manulife, Sun Life, Industrial Alliance (iA), and Desjardins if you’re looking at size and financial strength alone.

In our ratings, we looked at more than just financial strength, though. Other policy details matter when you’re figuring out which ones are the best Canadian life insurance companies.

Term life insurance is the cheapest type of insurance policy in Canada. Premiums are lower because coverage is temporary and the policies don’t have extra options like a savings & investment component — the way whole life insurance does.

Life insurance premiums depend on your personal details as well as your policy details. In general, you’ll get the lowest life insurance rates if you are:

- Young

- Healthy

- Non-smoker

- Female

You should get enough life insurance to cover your family’s needs. The general rule of thumb is to get 10-12 times your annual income. But, you may need more.

The best way to find out how much life insurance you should buy is to use our life insurance calculator. It will ask you some questions then tell you the best amount for your needs.

You can find the best quotes for term life insurance on PolicyAdvisor.com. Our online platform lets you easily customize your plan and compare quotes from leading providers in under a minute.

Save time and money when you shop and compare online. Click the button below to get started now.

Contact us

If you’re still looking for the best term life insurance direct for Canadian families, reach out to our team of experts! We’re happy to talk one-on-one to find out what your unique needs are help you figure out your best options.

If none of the providers that made our list are right for you, there are still many other good life insurance companies Canada and we can help you find one.

- The best life insurance company varies depending on you and your family's needs

- You can find the best policy by shopping and comparing quotes on PolicyAdvisor.com

- The top 5 best providers are Canada Life. Manulife, Sun Life, Industrial Alliance (iA), and Desjardins