1-888-601-9980

1-888-601-9980Life insurance for diabetics – lower rates, tips for Type 1, Type 2 diabetes

As a person with diabetes, finding a life insurance policy can be tricky, but it is not impossible. Many patients with well-maintained diabetes actually qualify for fully underwritten policies, with greater coverage and lower premiums. For those that don’t qualify, no medical life insurance is also a reliable option for diabetics, though premiums will be higher.

As one of the almost 2.5 million Canadians with diabetes (source: Statistics Canada), you may have hit some stumbling blocks or even brick walls on your search for insurance of any kind. Getting life insurance when you are diabetic can be a little less straightforward than for those without it. But, it is possible to obtain life insurance for diabetics, and maybe less expensive than you assumed.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

Why does diabetes affect insurance rates?

Diabetes is a disease that affects how your body uses and produces insulin, a hormone produced by your pancreas.

As you no doubt know – there are multiple types of diabetes:

- Type-1 diabetes, also known as insulin-dependent diabetes, is an auto-immune disorder. For Type-1 diabetics, their pancreas no longer produces insulin, a hormone that helps your body convert sugar to the energy you need. You need to administer synthetic insulin to cover for the food you eat.

- Type-2 diabetics produce insulin but their body does not use or recognize it correctly. They can deal with the condition through oral medication or diet. Type-2 diabetes is the most common form of diabetes in Canada, with approximately 90% of diabetics living with Type-2.

- Gestational diabetes is a temporary form of diabetes associated with pregnancy. The body cannot produce an adequate amount of insulin, leading to an increase in the amount of blood sugar. In most cases, gestational diabetes goes away post-pregnancy.

So why would diabetes affect life insurance policy premiums? Well, the stress of constantly fluctuating blood sugar levels puts stress on your internal organs like your heart and kidneys. The added stress means they are prone to failure in your older years, thus approving your application takes on added risk factors and adds to the cost of life insurance.

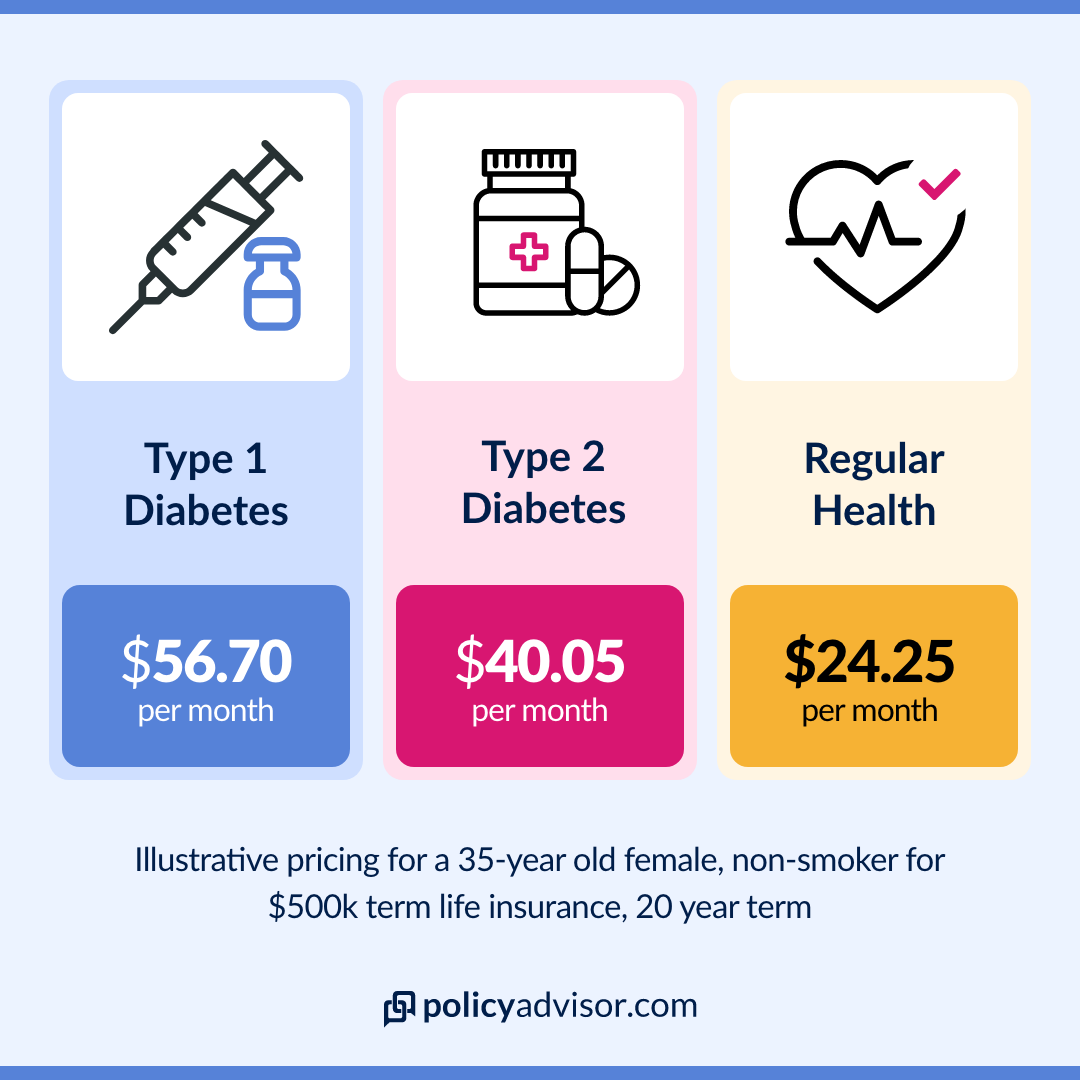

More specifically, Type-1 insulin-dependent diabetes is usually diagnosed in childhood and puts a lifetime of stress on one’s body. This is why insurance rates for Type-1 diabetics are higher.

Type 2 diabetes is more prevalent in individuals after the age of 40, and its effects can be quickly remedied by diet; organ stress is not as great of a factor in medical underwriting.

Gestational diabetes does not usually affect insurance rates, as most expecting mothers opt to do any medical underwriting before or after their pregnancy.

Can diabetics get life insurance?

Diabetics in Canada have many options when it comes to getting a life insurance policy. Diabetics who are in good health, with consistent medication levels, and who keep their blood sugar levels in control can qualify for standard, medically underwritten life insurance coverage. In medically underwritten life insurance, the life insurance company will arrange for a blood test and likely request for a physician’s report to evaluate and screen for a pre-existing condition and grant approval for a life insurance policy. This process may provide more monetary coverage (a higher death benefit) for a lower premium, than no medical life insurance.

Much like anyone with a pre-existing health condition, no medical life insurance is another choice for diabetics. No medical life insurance is a policy that is issued without the insured having to undergo a medical exam. It usually has the added advantage of a simpler and faster issuance process that doesn’t require details for every medical condition one may have.

The two most common types of no medical life insurance are simplified issue and guaranteed issue. Read more about simplified vs guaranteed.

Best life insurance for type 1 diabetics

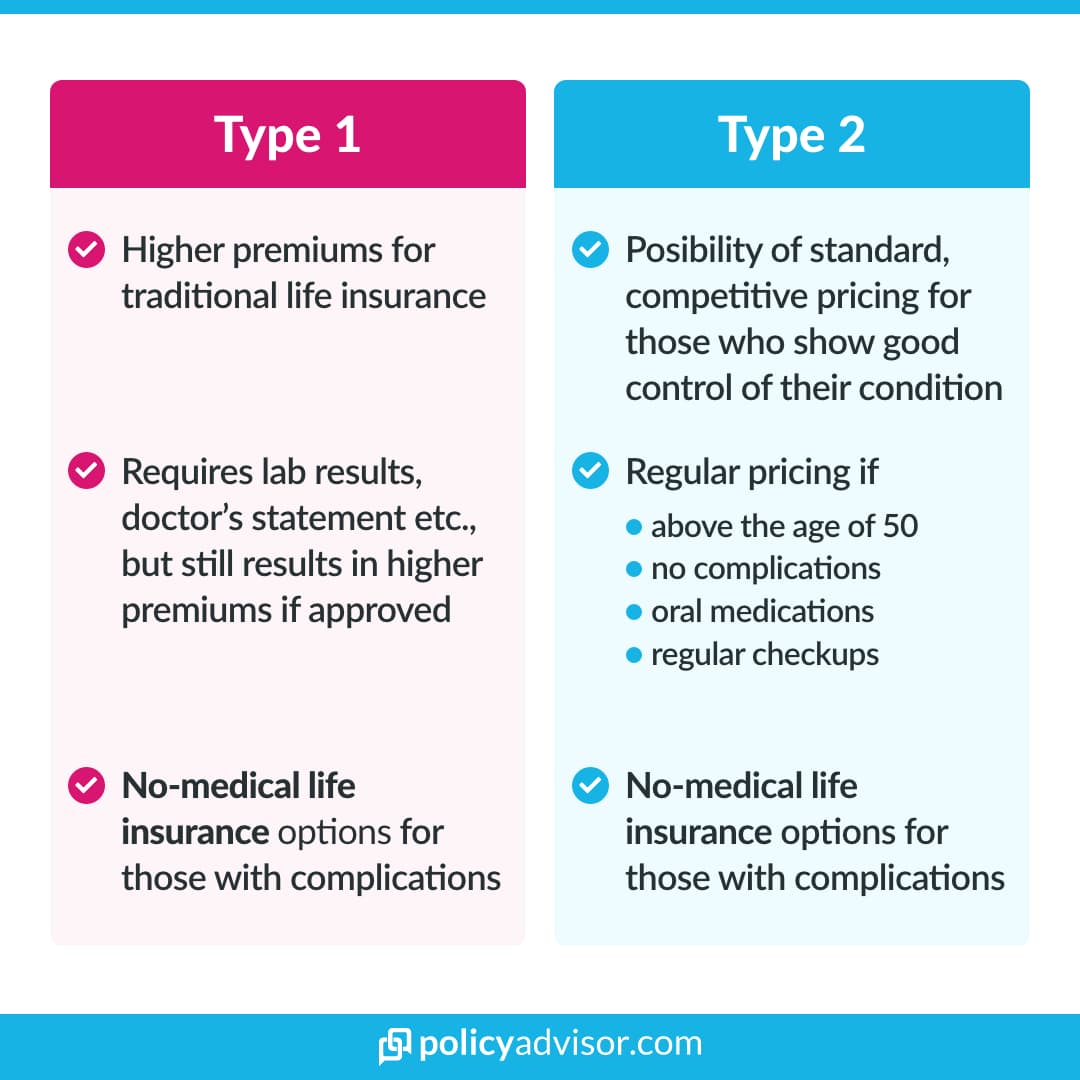

There are life insurance options for people with type 1 diabetes who are insulin-dependent. The availability of a life insurance policy depends on the age of the applicant, duration of the disease, and degree of control. Traditional life Insurance companies that require lab results will also seek a doctor’s statement to establish the stability of the treatment and the condition. In most cases, a life insurance company may apply a rating (higher premium) when approving life insurance for those with type 1 diabetes.

No-medical, questionnaire-based options make for an easier and faster process in such cases, albeit they offer life insurance for diabetics at higher premiums. For no-medical questionnaires, the focus is primarily on the age of the insured, the stability of the medication, and the risk of complications. If you are older, with no change in your insulin dependence in the last 12 months and no associated complications, you can easily get life insurance with no medical exam or obligation to provide medical records.

Best life insurance for type 2 diabetics

Yes, people with type-2 diabetes can get life insurance in Canada with the possibility of standard, competitive pricing. Life insurance companies are usually more accommodating when offering life insurance to people with diabetes who do not require insulin injections. Traditional insurance companies may even consider granting standard regular-health pricing (even more affordable life insurance) to someone who is:

- Above the age of 50

- Controlling their blood glucose levels and providing lab results with A1C levels

- Undergoes regular medical check-ups with a physician or specialist

- Is treated with oral medications that have not been increased in the past 12 months

- Follows a diet

- And has no diabetes diagnosis associated complications

There are also several options with no medical exam for people with diabetes that may not be able to get standard pricing or those that may want easier and faster access to life insurance. Most no-medical life insurance questionnaires contain a few questions that seek to assess how long you have had type 2 diabetes, whether your medications have changed recently, and whether you have any complications associated with this type of diabetes. Based on simple binary questionnaires, the eligibility of life insurance for diabetics can be established fairly quickly.

How can diabetics get a lower insurance premium?

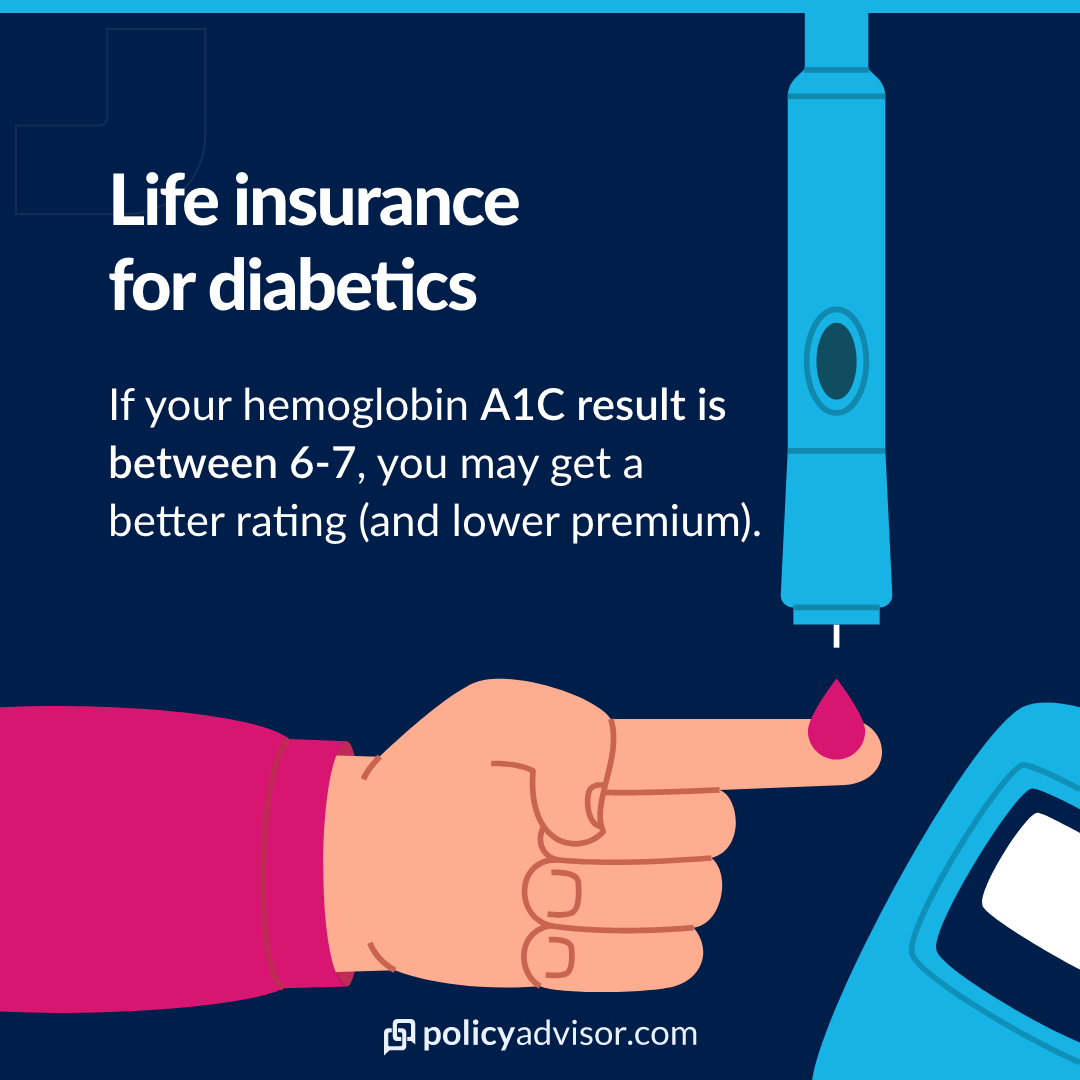

As hinted at above, those with diabetes can get a better insurance rating if they keep their blood sugar levels under tight control. Typically, that would mean a hemoglobin A1C result between 6-7. Once your blood sugar levels surpass those numbers, you may be looking at a higher rating, which will increase the cost of your premium.

Other factors like high blood pressure, diabetic retinopathy, diabetic neuropathy, kidney disease, and proteinuria can also affect your rating. While one of these issues may affect any diabetic as they age, if you have tight control and show no symptoms of them at the moment, it may be an opportune time to apply for life insurance as a diabetic.

What sort of questions do insurance companies ask diabetics?

Just like any other applicant, an insurance provider will ask you questions about your health and medical history to evaluate your risk when you apply for life insurance. When you disclose to your insurance broker that you are diabetic, they will have specific questions about the disease when calculating how to price your coverage. These questions are aimed at assessing the duration and stability of diabetes and the risks of any complications.

They will include:

- Details about your family doctor or endocrinologist

- When you were first diagnosed with diabetes

- What medications or treatment your diabetes requires (Whether you are insulin-dependent, or control your blood sugar levels through oral medication or diet)

- How often you check your blood sugar levels and the results of your most recent hemoglobin a1c blood test

- Any other health conditions you have that are or may be diabetes-related complications (like heart disease or high blood pressure, elevated cholesterol, kidney function, neurological problems, diabetic comas, or diabetic retinopathy)

- Your family doctor may be asked to provide an Attending Physician’s Report with details about the state of your health

Can diabetics get a life insurance policy if they have been turned down before?

Yes, diabetics can get life insurance if they have been turned down before or denied coverage. Read more about your life insurance options when your application has been declined.

Getting life insurance with diabetes

As experienced, licensed insurance brokers, the PolicyAdvisor team has helped many diabetics in Canada get either a no medical or medically underwritten policy. We work with the best life insurance companies in Canada to shop for the best provider for your needs. Whether it is term policy or permanent life insurance policies you seek, our advisors have experience placing every different type of life insurance and matching our clients with affordable coverage.

If you have any questions at all about life insurance for diabetics or want to chat about what you can do to make sure you apply for the right kind of coverage, schedule a free consultation with one of our experts and we’ll make sure you have all the facts about term life insurance for diabetics.

- Individuals with diabetes have several options for life insurance in Canada

- Availability of life insurance for diabetics depends on age, duration, stability of treatment and absence of complications

- If you are older and your diabetes is well-maintained, then several fully underwritten products will be available

- No medical life insurance options are easier, faster and more flexible, albeit at higher premiums