1-888-601-9980

1-888-601-9980What are the different types of life insurance in Canada?

In Canada, there are two main kinds of life insurance: one that lasts for a certain period (term life insurance) and one that lasts your whole life (permanent life insurance). Permanent life insurance comes in sub-types, like whole life, universal life, and term-to-100 insurance, which all have different cash growth and investment opportunities. The best type of insurance for you depends on things like your age, how many people rely on you, how much money your family makes, if you’re married, how much debt you have, if you have a mortgage and more.

Many people think there are only two kinds of life insurance in Canada: term life insurance versus whole life insurance. But there are actually many more options!

Read on to find out about the three common types of life insurance available in Canada to help you figure out which policy will fit your needs.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What are the two main types of life insurance?

The two main types of policies are term life insurance and permanent life insurance (which is commonly called whole life insurance). In addition to the main types, there are also no-medical life insurance plans.

Term and whole life insurance are traditionally underwritten, meaning there are a lot of application questions and usually a medical questionnaire or exam. No-medical policies have accelerated underwriting, meaning no medical exam, fewer health questions, and faster approvals.

Here’s a breakdown and detailed description of all the types of life insurance that are commonly offered in Canada.

1. Term life insurance

Term life insurance pays a tax-free, lump-sum payment to your beneficiaries if you die within the policy term.

The most popular coverage lengths for term insurance are:

- 10 years

- 15 years

- 20 years

- 25 years

- 30 years

- up to age 65

Some life insurance companies in Canada (such as RBC Life Insurance or Industrial Alliance Life Insurance) allow you to pick your own term (6, 8, 11 years, etc.).

With term insurance, you can choose your policy lengths to match time-bound debts or liabilities. This could include financial obligations like:

- Your mortgage

- Any outstanding debt you may have

- Coverage for your children’s education

- Living expenses for your loved ones so they maintain the same standard of living

✅ Advantage of term life insurance

- The cheapest form of life insurance

- Your monthly premiums stay the same throughout the term

- It’s flexible—when you buy a term policy, you choose your coverage amount and coverage term

- You can stack your term policies to match each of your financial obligations

❌ Drawback of term life insurance

- Coverage will expire eventually —this means you must find coverage again when the term is up.

✍️ Bottom line

Term life insurance is a cost-effective and flexible way to protect your family, especially during years when you have many financial obligations.

Read more about term life insurance.

| What happens when your term is up?

1️⃣ Renew your policy Most term policies are renewable without a medical exam up to age 75. This means you can do-over the same policy without the hassle of all the paperwork. Some providers offer yearly renewable term policies, which seem like a cheap option for life insurance at first glance. But buyer beware, renewal prices are usually significantly higher than the original term. 2️⃣ Convert your policy Some term policies are convertible to permanent whole-life policies (more on that below). Most term life insurance policies are convertible before age 71 only, though there are exceptions, with some life insurance companies allowing conversion before age 75. 3️⃣ Buy a new policy If you don’t want to renew or convert, you can shop around to find a new policy. However, keep in mind that as you age your life insurance rates will increase compared to your original policy, no matter which company you’re with. |

2. Permanent life insurance

Permanent life insurance (also known as whole life insurance) covers you for your entire life, rather than just a short term. Permanent life insurance is best suited to protect ‘permanent’ or ‘lifelong’ needs such as estate tax liabilities, care for a disabled child or dependent, liquidity for closely-held businesses, and even funeral expenses.

Permanent life insurance also has an investment component. As you pay into your permanent policy over your lifetime the insurance company invests your premiums and your policy starts to accumulate a cash value. Typically, the cash value gains grow year after year and are accessible starting in a specific year of the policy (such as after 10 years).

A policy’s cash value and the cash surrender value may be different.

- Cash value: the sum of money that builds inside the policy. This value can be used to borrow or loan against.

- Cash surrender value: the amount of money paid to a policyholder if they terminate the policy minus any surrender fees.

Some policies also allow you to tap into the investment component of the policy in the form of policy loans, dividends, and more— but it depends on what kind of permanent life policy you have. There are many different sub-types of permanent life insurance policies such as:

- Whole life insurance

- Non-participating

- Participating

- Universal life insurance

- Term-to-100

✅ Advantages of permanent life insurance

- The policy accumulates cash value, which allows for investment or other growth opportunities

- Coverage for life

❌ Disadvantages of permanent life insurance

- Higher premiums

- Premiums can fluctuate, depending on the product

✍️ Bottom line

Permanent life insurance is a more nuanced product that can be beneficial for those specific financial goals beyond covering their debts and providing a lump-sum payment for their loved ones.

Read below about the different subtypes of permanent life insurance policies available, like whole life insurance (non-participating and participating), universal life insurance, variable life insurance, and term-to-100.

What is whole life insurance?

Whole life insurance is a form of permanent life insurance that provides you with coverage from the day you get your policy until the day you die. In other words, it protects you for your entire life. As long as you pay your premiums, your policy never expires — it’s as simple as that. It is the flagship type of “permanent” life insurance, which is why people often interchange the names.

Most whole life policies come with something called a cash value component. As you pay your premiums, part of that money is invested and generates a tax-deferred cash value that grows over time. You can then access it during your lifetime. You can access it in many ways such as:

- Withdrawing your cash value

- Borrowing your cash value

- Using it to loan against

- Cancelling the policy and cashing out the value

Beyond that additional perk, some whole life insurance policies offer additional investment perks called “participating life insurance.” Whole-life policies that just have the cash value and no additional investment perks are known as “non-participating.”

Read more about whole life insurance.

What is non-participating whole life insurance?

Non-participating whole life insurance is permanent insurance in its most basic form. It provides a tax-free death benefit with lifetime coverage that is guaranteed as long as you are paying the premiums. They have a level premium, it can’t increase if your health changes once your coverage is in force.

A non-participating policy has accumulated cash value that you can utilize, but it does not pay additional dividends.

What is participating whole life insurance?

Participating life insurance is a type of whole life insurance policy that—in addition to the guaranteed death benefit—can generate and pay out money over the course of the policy in the form of dividends.

These dividends, which are determined by the insurance company’s performance and profits, are typically issued to the policyholder annually. The policyholder can then choose to:

- Take the dividends as cash

- Premium reductions

- Put into a cash accumulation interest account

- Buy up more life insurance coverage

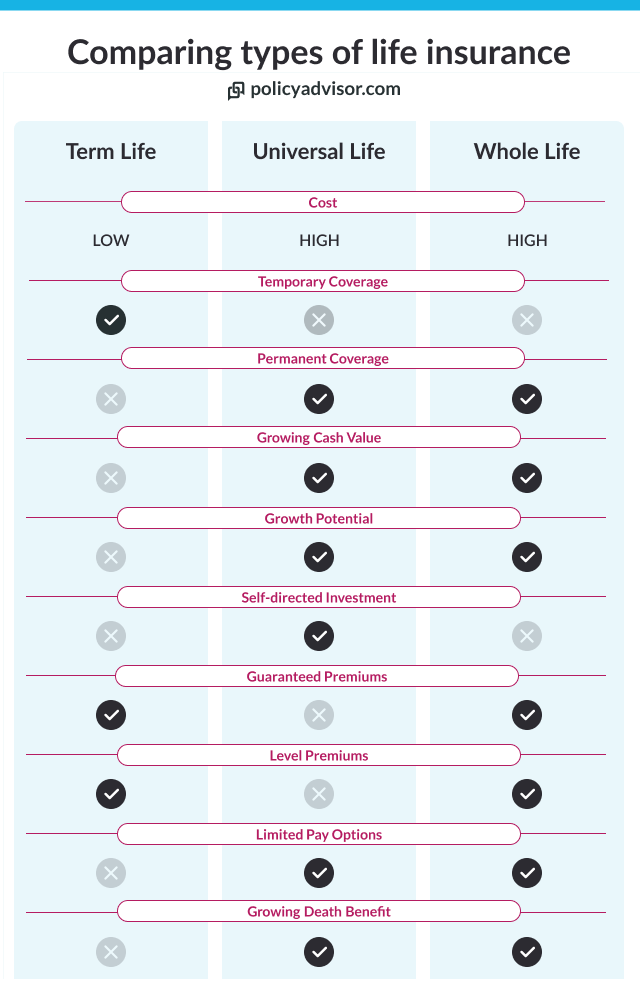

| Term Life Insurance | Whole Life Insurance | |

|---|---|---|

| Cost |

|

|

| Premiums |

|

|

| Death Benefit |

|

|

| Cash Value |

|

|

| Dividends |

|

|

| Investments |

|

|

What is universal life insurance?

Universal life insurance is similar to whole life insurance, except there is a self-directed long-term investment component. Your insurer gives you options for investing the cash value of your policy so it can be considered a way to save for retirement. These options are presented as portfolios that usually generate varying levels of guaranteed returns. If you are a savvy investor or mindful of estate planning, you may find that universal life policies could be an appealing option.

That said, universal life insurance plans require more hands-on activity than other life insurance coverage options, and may not boast the same rate of return as other investment options. Additionally, a universal policy would require more monthly premiums than a simple term life policy would, because there’s more potential for earning.

Read more about the difference between whole life and universal life insurance.

| Whole Life Insurance | Universal Life Insurance | |

|---|---|---|

| Cost |

|

|

| Premiums |

|

|

| Death Benefit |

|

|

| Cash Value |

|

|

| Dividends |

|

|

| Investments |

|

|

What is variable life insurance?

Variable life insurance is similar to universal life insurance in that it has a self-directed investment component—however, the portfolios available are more volatile (or variable) than what is usually offered with universal life. The returns are not guaranteed.

Variable life insurance usually isn’t offered in Canada. Instead, whole life with an investment component is almost always referred to as universal life insurance in Canada.

What is term-to-100 insurance or term life insurance to age 100?

Term-to-100 insurance plans are the bridge between term and whole-life insurance. Coverage lasts your entire life, but you only pay premiums for a fixed term (until you turn 100 years old). While this type of policy is permanent, it doesn’t have the cash value or investment component that other permanent policies have—but that does make term-to-100 cheaper than most permanent policies. Many choose a term-to-100 policy with a lower death benefit amount to cover funeral costs (or as a de facto final expense insurance).

Read more about term to 100 life insurance.

3. No medical life insurance

No medical life policies have very few medical questions and do not require a medical exam. Options include simplified and guaranteed issue life insurance. Both types of policies insurance have lower coverage amount options than traditionally underwritten policies. These policies are best for those who:

- Have underlying health conditions or medical issues

- Have hobbies or pastimes that are considered dangerous (like sky-diving)

- Need to get coverage quickly

✅ Advantages of no-medical life insurance

- The application process is quick

- No medical exams

- Few or no medical questions

❌ Disadvantages of no-medical life insurance

- Usually less coverage offered

- Higher premiums

✍️ Bottom line

No-medical life insurance is a great option for those in poor health or who need coverage fast.

Read more about life insurance without medical exams.

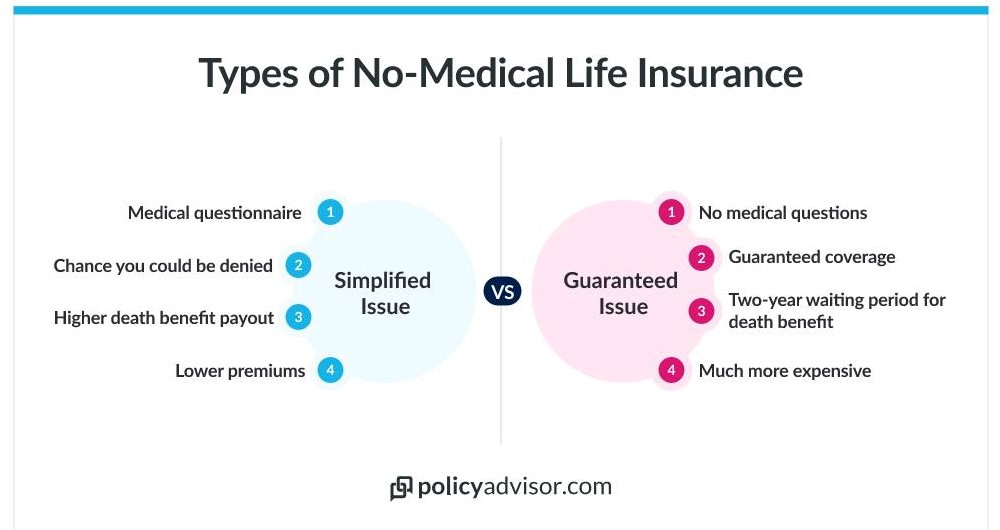

Simplified life insurance

Simplified issue life insurance requires you to answer a FEW questions about your medical history on the life insurance application, rather than undergoing a full physical medical exam and interview process. Simplified issue life insurance policies usually carry additional limitations such as an exclusion period (sometimes 1-2 years) during which no claims are accepted. They may also have lower death benefit coverage than traditional policies.

Read more about simplified issue life insurance.

Guaranteed life insurance

Guaranteed life insurance has NO health questions and is essentially a pay-to-play product. It is a last-resort life insurance option. It’s there for those who don’t qualify for any traditional life insurance policies or simplified life policies. A guaranteed issue policy has a 2-year waiting period as well as a lower life insurance payout amount—the death benefit is usually limited to $50,000.

Find out more about the difference between simplified vs guaranteed life insurance.

Compare the different types of life insurance

While all life insurance pays out a death benefit, not every policy is built the same. So how do they compare? The chart below shows how some of the most popular types of life insurance compare.

What is the best type of life insurance for me?

Finding the perfect life insurance plan can be a challenge and the answer isn’t always straightforward. Check out our life insurance needs calculator to see what sort of coverage you need to protect your family and loved ones.

Once you figure out your coverage needs, you can start comparing life insurance quotes online and choose your preferred life insurance company and life insurance plan.

How do I get life insurance?

You can get an individual life insurance policy by clicking on any of our tools mentioned above or booking some time with our life insurance experts.

They can help you determine how much life insurance you need to protect your family or other financial interests. Reach out and get a quote!