- Life insurance protects businesses from financial disruption caused by the death of key owners or partners

- Corporate-owned policies enhance succession planning flexibility by leveraging the Capital Dividend Account (CDA), which allows tax-free distributions of life insurance proceeds to shareholders

- Participating whole life insurance provides guaranteed lifetime coverage, tax-sheltered growth, and dividend potential for corporate liquidity

- Term insurance is suitable for temporary needs or budget-conscious owners, while permanent policies support long-term planning

- Integrating insurance with succession planning, key person coverage, and debt management maximizes strategic value

Running a business in Canada takes vision, discipline, and financial foresight. Yet, life insurance remains one of the most underused tools for entrepreneurs. Beyond personal protection, it serves as a corporate strategy for managing risk, optimizing taxes, and ensuring business continuity.

In the first half of 2025, Canada’s new annualized premium for individual life insurance rose by 9% year over year to $1.04 billion, with permanent life insurance such as whole life and universal life showing the strongest growth (LIMRA). This trend highlights how business owners increasingly view life insurance as a strategic business asset that builds liquidity, supports succession planning, and strengthens long-term corporate wealth.

This guide explains how life insurance for business owners in Canada can protect assets, reduce taxes, and enhance corporate stability through personal, business-owned, or corporate-owned policies.

Do business owners in Canada need life insurance?

Yes, every business owner in Canada faces financial risks that extend beyond daily operations. The death or disability of a key owner, shareholder, or partner can disrupt cash flow, debt repayment, and client relationships almost overnight. Life insurance provides a financial buffer that protects both the company and the people who depend on it.

Without proper life insurance for entrepreneurs and incorporated businesses, several issues can arise:

- Outstanding loans become payable: Lenders may demand immediate repayment of business debts guaranteed by the deceased

- Ownership disputes emerge: Shareholder or partnership agreements may trigger forced buyouts at unfavourable terms

- Client and supplier confidence declines: Uncertainty about leadership continuity can strain critical relationships

- Credit access is restricted: Banks may freeze credit facilities during estate or ownership transitions

- Liquidity pressure intensifies: Surviving partners or family members may struggle with cash flow issues such as to fund ownership transfers or maintain operations

A well-structured business life insurance policy ensures liquidity when it is needed most. It supports succession planning, protects corporate credit, and preserves the value of the business for successors or surviving shareholders.

See how much life insurance would cost for you in Canada

Get instant quotes from Canada's top life insurance providers and find the perfect coverage for your family.

Powered by

![]()

How to choose the right business life insurance policy?

With a clear understanding of ownership, taxation, and policy types, business owners can evaluate options systematically. The best life insurance for small business owners depends on aligning policy features with business objectives.

Choosing between different life insurance policies for business owners

| Policy type | Key features | Best for |

| Term Life |

|

Temporary needs, covering loans or partnership agreements, startups, or budget-conscious owners seeking maximum death benefit coverage |

| Participating (Par) Whole Life |

|

Predictable, stable long-term planning with maximum tax optimization and wealth accumulation |

| Non-Participating Whole Life |

|

Simplicity and cost certainty; suitable for straightforward protection needs |

| Universal Life |

|

Sophisticated investors seeking investment control and premium flexibility; comfortable with market volatility |

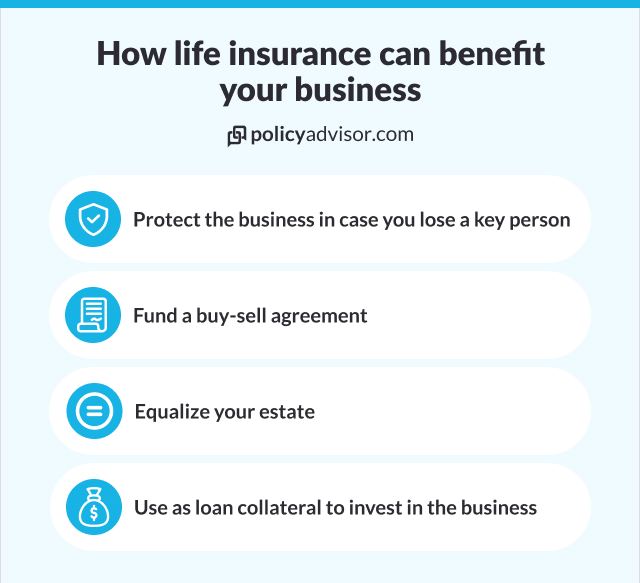

What are the benefits of corporate-owned life insurance for a business owner in Canada?

Life insurance offers far more than personal protection for Canadian entrepreneurs. It functions as a strategic financial tool that safeguards business operations, supports continuity, and enhances long-term corporate planning. Whether held personally or through a corporation, the right policy can strengthen a company’s financial resilience in several ways:

How life insurance supports business continuity, tax planning, and wealth for Canadian companies

| Strategic objective | Key benefits of corporate owned life insurance | Why it matters for Canadian businesses | Who is it ideal for? |

| Business continuity protection |

|

Helps the business survive the sudden loss of a key person without financial strain | Small or mid-sized businesses heavily reliant on specific employees |

| Funding buy-sell agreements |

|

Ensures smooth ownership transitions and avoids forced asset sales or debt | Partnerships or closely held corporations with multiple shareholders |

| Estate equalization for family businesses |

|

Balances family interests while keeping the business operational | Multi-generational family-owned businesses |

| Tax-advantaged corporate wealth accumulation |

|

Creates a corporate asset that grows efficiently while supporting long-term planning | Corporations seeking long-term tax-efficient asset accumulation |

| Key person insurance |

|

Reduces financial risk when the business relies on highly specialized talent and coverage may include owners, executives, or specialised contributors vital to business continuity | Startups, tech firms, or specialized businesses with high-dependency roles |

Should business owners choose corporate or personal life insurance ownership?

Choosing the ownership structure is a foundational decision that shapes the entire insurance strategy. For corporate owners in Canada, it affects tax planning, succession, and the overall value of the policy.

Corporate ownership vs personal life insurance ownership

| Feature | Corporate ownership | Personal ownership |

| Tax efficiency | Death benefit creates Capital Dividend Account (CDA) credits for tax-free shareholder distributions | Death benefit passes directly to beneficiaries; no CDA benefits |

| Balance sheet impact | Cash value counts as a corporate asset, improving financial ratios and lending capacity | Policy does not appear on corporate balance sheet |

| Business continuity | Proceeds fund shareholder buyouts, repay business debts, or maintain operations | Proceeds go to personal beneficiaries; limited direct business impact |

| Creditor protection | May offer protection depending on provincial law and policy structure | Some provinces provide enhanced protection for personally owned policies with family beneficiaries |

| Administrative complexity | Requires corporate compliance and record-keeping | Simple structure, fewer administrative requirements |

| Portability | Policy remains with the corporation; may be affected by business structure changes | Policy stays with the owner regardless of business changes or sales |

| Estate planning | Supports corporate succession and tax planning | Supports personal estate planning and wealth transfer |

What are the tax benefits of corporate-owned life insurance?

Corporate-owned life insurance (COLI) provides significant tax advantages when structured properly under Canadian tax law. Understanding these mechanisms is essential for maximizing the value of life insurance for entrepreneurs and incorporated businesses.

Key tax mechanisms

- Tax-free death benefit: Life insurance proceeds paid to a corporation are received tax-free, providing immediate liquidity without income tax liability. This contrasts with most other corporate assets, which face taxation

- Capital Dividend Account (CDA): The death benefit, minus the policy’s adjusted cost basis (ACB), generates a CDA credit that allows tax-free dividend payments to shareholders. This is the most powerful tax advantage of corporate-owned life insurance

- Tax-deferred growth: Cash value accumulates without annual taxation, allowing compounding on the full pre-tax amount, unlike most corporate investments subject to tax on interest, dividends, or capital gains

- Adjusted cost basis considerations: A lower ACB relative to the death benefit maximizes the CDA credit and tax-free distribution potential. The ACB of a life insurance policy equals total premiums paid minus the NCPI and other adjustments under ITA s.148(9)

For example, a corporation owns a $2 million whole life policy and has paid $400,000 in premiums (adjusted cost basis or ACB). Upon the insured’s death, the Capital Dividend Account (CDA) credit is calculated as:

$2,000,000 (death benefit) − $400,000 (ACB) = $1,600,000 CDA credit

This $1.6 million can be distributed to shareholders as tax-free capital dividends. Without the CDA, the same amount paid as regular dividends could face combined federal and provincial taxes of around 50%, potentially saving shareholders approximately $800,000 in personal taxes.

Non-deductibility of premiums: Life insurance premiums are not tax-deductible for corporations. They are paid with after-tax corporate dollars. However, the tax-free death benefit and CDA credits generally provide far greater value than any potential premium deduction, especially for long-term policies.

Why whole life insurance is ideal for business owners

Whole life insurance offers features that make it the preferred choice for most established Canadian businesses. Each premium contributes to:

- Death benefit protection: Guaranteed lifetime coverage ensures certainty for estate and business planning, with no risk of coverage lapsing

- Cash value accumulation: A tax-sheltered account grows predictably and becomes a corporate asset

When owned by a corporation, this cash value provides strategic flexibility:

- Policy loans: Borrow against cash value for working capital, equipment purchases, or opportunity investments with favorable and flexible terms

- Collateral assignment: Use the policy to secure business credit lines or commercial loans at better rates than unsecured financing

- Retirement funding: Access accumulated value during ownership transitions or corporate reorganizations via policy loans or surrenders

Canadian life insurers maintain strong capital positions, ensuring the reliability of these long-term guarantees (Office of the Superintendent of Financial Institutions, OSFI).

How do participating whole life policies work for business owners?

Participating (par) whole life insurance adds value beyond lifetime coverage through annual dividend distributions. While dividends are not guaranteed, Canadian mutual insurers have historically paid them consistently for decades, providing both growth and flexibility for business owners.

How policy dividends work: Participating policies allow policyholders to share in the insurer’s favorable operating experience. Surplus arises when:

- Investments outperform expectations

- Mortality experience is better than projected

- Expenses are lower than anticipated

This surplus is distributed as dividends to participating policyholders, creating a source of cash value growth over time.

Strategic dividend options for business owners: Dividends from participating policies can be used in three main ways:

- Purchase paid-up additions (PUAs): Increases both death benefit and cash value on a compounding basis, accelerating policy growth and maximizing CDA credits

- Premium reduction: Offsets ongoing premiums, improving corporate cash flow while maintaining coverage making it useful in years of constrained cash flow

- Cash payments: Provides flexible annual income to support operations or build retained earnings

The compounding advantage: When dividends purchase PUAs, growth accelerates exponentially. Each PUA acts as a small participating policy, earning its own dividends in future years.

For example, a corporate-owned policy earning $10,000 in dividends that purchases PUAs increases death benefit and cash value. The following year, those PUAs also earn dividends, compounding growth over decades.

This compounding effect:

- Enhances the asset value on the corporate balance sheet

- Increases Capital Dividend Account credits available at death

- Makes participating whole life highly effective for long-term wealth accumulation, business succession, and estate planning

The Canada Revenue Agency recognizes this structure, providing favorable tax treatment that enhances its value for incorporated business owners.

How the 2025 economic environment affects business life insurance

The Canadian economy directly influences the cost, growth, and strategic value of life insurance for entrepreneurs. Interest rates, inflation, and corporate taxation all shape policy performance, dividends, and tax advantages.

Understanding these factors helps business owners choose between term, permanent, or participating whole life policies to best support business continuity, succession planning, and wealth accumulation.

| Factor | Impact on business life insurance |

| Interest rates & dividends | Higher rates improve participating whole life dividends; low rates can pressure returns, but major Canadian insurers maintain consistency. |

| Inflation | Increases the value of tax-deferred cash value growth in permanent policies; term insurance provides fixed protection but no accumulation. |

| Corporate taxation | CDA credits from corporate-owned policies offer tax-free shareholder distributions; provincial variations affect strategy value. |

| Economic stability | Stable rates and insurer performance in 2025 favor permanent life insurance for long-term planning; term insurance remains cost-effective for short-term needs. |

Frequently asked questions

How much life insurance does a business owner need?

Coverage depends on business debts, partner buyout requirements, revenue replacement, and succession plans. Most advisors recommend totaling all business loans plus 3–5× the owner’s annual contribution to revenue, then adjusting for buyout agreements and key person value.

Can a corporation deduct life insurance premiums as a business expense?

A corporation generally cannot deduct life insurance premiums as a business expense because they are paid with after-tax dollars, except when the policy is required as collateral for a loan from a restricted financial institution.

What is the Capital Dividend Account and how does it work?

The CDA is a notional corporate account that tracks certain tax-free surpluses. Corporate-owned life insurance death benefits exceeding the adjusted cost basis create CDA credits, which can be distributed to shareholders as tax-free capital dividends under a formal election.

Should the business or individual own the life insurance policy?

It depends on objectives. Corporate ownership provides CDA benefits, balance sheet value, and business liquidity. Personal ownership offers simplicity and direct estate planning. Corporations with retained earnings usually benefit from corporate ownership, while sole proprietors or those focused on personal estates may prefer personal ownership.

How does cash value in a life insurance policy work?

Cash value is the tax-deferred accumulation component of permanent life insurance. A portion of premiums grows predictably, with potential dividends in participating policies. Owners can borrow against it, use it as collateral, or access it for business needs, while whole life guarantees both growth and death benefit protection.

Life insurance helps Canadian business owners manage risks such as loan acceleration, forced buyouts, and liquidity gaps when key stakeholders die unexpectedly. Corporate ownership maximizes tax efficiency through the Capital Dividend Account, while participating whole life policies provide guaranteed growth, dividend potential, and cash value that supports business needs. Integrating coverage with succession plans, key person protection, and debt management multiplies its value, making permanent life insurance a strategic tool for long-term business planning in 2025.

LIMRA. “Canadian Life Insurance Sales Post Fifth Consecutive Quarter of Growth.” LIMRA, September 9, 2025.