- Super Visa insurance is meant for parents and grandparents of Canadian citizens or permanent residents visiting Canada for extended stays. To qualify, applicants must have medical insurance from a Canadian insurer with at least $100,000 in coverage for one year, including emergency medical care, hospitalization, and repatriatio

- Visitors to Canada aren’t covered under public healthcare. A single hospital stay can cost $10,000 or more, and major surgeries can exceed $100,000. Super Visa insurance protects against these out-of-pocket costs

- Super Visa insurance typically costs $100–$200 per month, but premiums increase with age and health conditions. Opting for a higher deductible can significantly reduce premiums—for example, a $5,000 deductible may save hundreds annually compared to a $1,000 deductible

Hospitalization in Canada can cost visitors thousands of dollars, with even a short emergency stay leading to significant medical bills. Since parents and grandparents visiting on a Super Visa are not covered under provincial healthcare plans, having proper medical insurance is mandatory.

Super Visa insurance, in this case, helps protect your parents or grandparents from these high medical costs during their stay. In fact, Super Visa insurance is mandatory medical coverage required by the IRCC for parents and grandparents visiting Canada under the Super Visa program.

Based on our expert advisors’ review, some of the best Super Visa insurance companies in Canada include Allianz, TuGo, Manulife, Secure Travel, Destination Canada, GMS, and 21st Century.

How much does Visitor Insurance cost?

Get instant quotes from Canada's top travel insurance providers and find the perfect coverage for your trip.

Powered by

![]()

What is Super Visa Insurance and why do you need it?

Super Visa insurance is a crucial requirement for parents and grandparents applying for the Canadian Super Visa, a special visa that allows them to visit Canada multiple times.

It’s valid for up to 10 years, and visitors can stay in Canada for up to 5 years each time they visit. Parents and grandparents can even request to extend their stay by 2 years at a time while in Canada. In comparison, a normal visitor to Canada visa only lets visitors stay up to 6 months.

This long-term visa offers an excellent opportunity to reunite families, but to qualify, applicants must show that they are covered by a valid travel medical insurance policy.

This coverage helps protect them from the high cost of emergency medical care in Canada, where a single hospital stay can cost over $10,000 without insurance.

Quick facts about Super Visa insurance

| Minimum coverage amount | $100,000 |

| Coverage duration | At least 1 year |

| Who needs it | Parents and grandparents applying for a Super Visa |

| Covers | Emergency medical care, hospitalization, and repatriation |

| Is it mandatory? | Yes |

Best super visa insurance companies in Canada

| Company name | Best super visa insurance for |

| Allianz | Frequent travellers |

| TuGo | Customizable riders |

| Manulife | Value-added services |

| Secure Travel (RIMI) | Senior travellers |

| Destination Canada | Comprehensive coverage |

| GMS (Group Medical Services) | Competitive pricing |

| 21st Century | Healthy travellers |

Key changes to the Super Visa application in 2026

As of March 31, 2026, IRCC has introduced new income calculation rules for the Super Visa program, making it easier for eligible families to qualify for Super Visa insurance. Here are the updated rules for 2026:

- Hosts can now meet the minimum income requirement using either of the last 2 tax years, rather than only the most recent year. Earlier, only the most recent tax year was taken into consideration

- The income of the visiting parent or grandparent can now be added to help meet eligibility requirements in certain cases

- The Minimum Necessary Income is now set to LICO + 30% to account for the rising living costs

Super Visa Eligibility Requirements

To be eligible for a Super Visa, the person applying must:

- Be the parent or grandparent of a Canadian citizen or Canadian permanent resident

- Have a letter written by their child or grandchild stating that they will provide financial support to the visa holder during their stay

- Provide proof that their child or grandchild meets the minimum income requirement (Low Income Cut off Minimum (LICO))

- Provide a copy of their child or grandchild’s Canadian passport or Permanent Resident Card (PR Card)

- Take a medical exam and show they are healthy enough to enter the country

- Provide proof that they have adequate insurance coverage from a Canadian insurance company (super visa insurance)

Visit the Government of Canada’s website for more details about the requirements for the government’s super visa program.

Super Visa insurance checklist: What you need to apply

The minimum requirements a Super Visa insurance policy has to meet are:

- Must be valid for at least one year from the date the visa holder arrives in Canada

- Must have at least $100,000 in coverage

- Must cover emergency medical care, possible hospitalization, and repatriation

- Must be active and available for review by an immigration official each time the visa holder enters Canada

- Must have been bought from a Canadian insurance company or an insurer approved by the Office of the Superintendent of Financial Institutions (OSFI)

What is the LICO requirement for a Super Visa?

If you are applying for a Super Visa for your parents or grandparents in 2026, it is essential to meet the Low Income Cut-Off (LICO) requirements set by Immigration, Refugees and Citizenship Canada (IRCC).

These thresholds demonstrate that you have sufficient financial means to support your visiting family members during their stay in Canada.

The required income level depends on the total number of people in your family unit, including yourself, your spouse or common-law partner (if applicable), your dependents, and the parent(s) or grandparent(s) you wish to invite.

As per the new rules, effective July 29, 2026, individuals sponsoring the super visa program must meet the following minimum income requirements:

| No. of family members | Minimum gross income required (Updated 2026) | Old minimum gross income required |

| 1 person | $30,526 | $29,380 |

| 2 persons | $38,002 | $36,576 |

| 3 persons | $46,720 | $44,966 |

| 4 persons | $56,724 | $54,594 |

| 5 persons | $64,336 | $61,920 |

| 6 persons | $72,560 | $69,834 |

| 7 persons | $80,784 | $77,750 |

| Each additional person | $8,224 | $7,916 per member |

Note: Your family size includes yourself, your spouse or partner (if applicable), your dependents, and the parents or grandparents you’re inviting under the Super Visa. These amounts reflect the minimum income you must show through documents such as your Notice of Assessment (NOA), employment letters, or recent pay stubs.

How does medical insurance work for Super Visa?

Super Visa medical insurance works like a private emergency health insurance plan for parents and grandparents visiting Canada under the Super Visa program. Here’s how the process typically works:

- Before submitting a Super Visa application, the applicant must buy a Super Visa insurance policy from an approved insurer

- The insurance policy becomes active on the effective date selected in the policy, usually the day the parent or grandparent arrives in Canada, and it will continue until the full policy term, except when it is cancelled

- The policy covers eligible emergency medical expenses such as emergency hospitalization, doctor and ambulance fees, diagnostic tests and prescription medication, emergency dental treatment, and repatriation expenses

What does medical insurance for Super Visa cover?

A standard medical insurance for Super Visa holders covers a broad range of emergency medical services and hospital-related costs. Here are the typical benefits included in a comprehensive policy:

- Emergency hospitalization and medical care

- Emergency dental treatment

- Ambulance services, including air ambulance if medically necessary

- Follow-up treatment related to the initial emergency

- Medical appliances, such as crutches, braces, or wheelchairs

- Private-duty nursing and home care (if medically required)

- Repatriation of remains in case of death

- Companion accommodation if a family member needs to stay with the patient

- Emergency surgeries or procedures

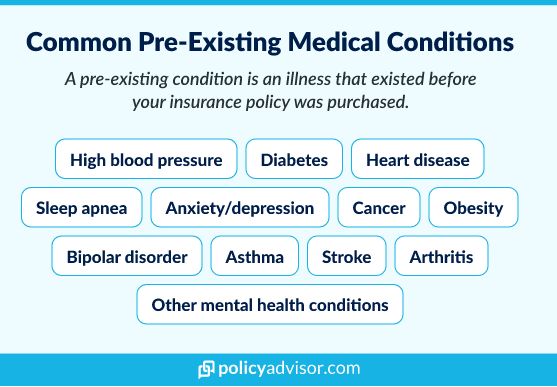

Does Super Visa insurance cover pre-existing medical conditions?

Yes, Super Visa insurance will cover pre-existing conditions or medical conditions that you already had before you applied, if they are stable. Stable means your condition has not:

- Gotten worsened

- Caused new symptoms

- Caused you to need new medication or treatment

- Cause a new diagnosis

Most Canadian providers say that your pre-existing health issue has to meet these conditions for at least 180 days (about 6 months) to be considered stable and included under your health insurance plan for the Canadian Super Visa.

But note that this can be different for different providers. The amount of time your condition has to be stable, also called a “minimum stability period”, can be anywhere from 90-180 days.

How much do medical expenses cost in Canada without Super Visa insurance?

A single medical emergency in Canada can cost over $10,000 for visitors without Super Visa insurance. Such expenses must be paid out-of-pocket for all medical care, including hospital stays, emergency treatment, diagnostics, and more.

Uninsured medical expenses in Canada for Super Visa applicants

| Medical Service | Estimated Cost (CAD) |

| Emergency Room Visit (basic) | $800 – $1,500 |

| Hospital Stay (per day) | $3,000 – $5,000 |

| Intensive Care Unit (ICU) (per day) | $5,000 – $10,000+ |

| Minor Surgery | $3,000 – $15,000 |

| Major Surgery | $20,000 – $100,000+ |

| MRI or CT Scan | $800 – $2,500 |

| Ambulance Services | $500 – $1,000+ |

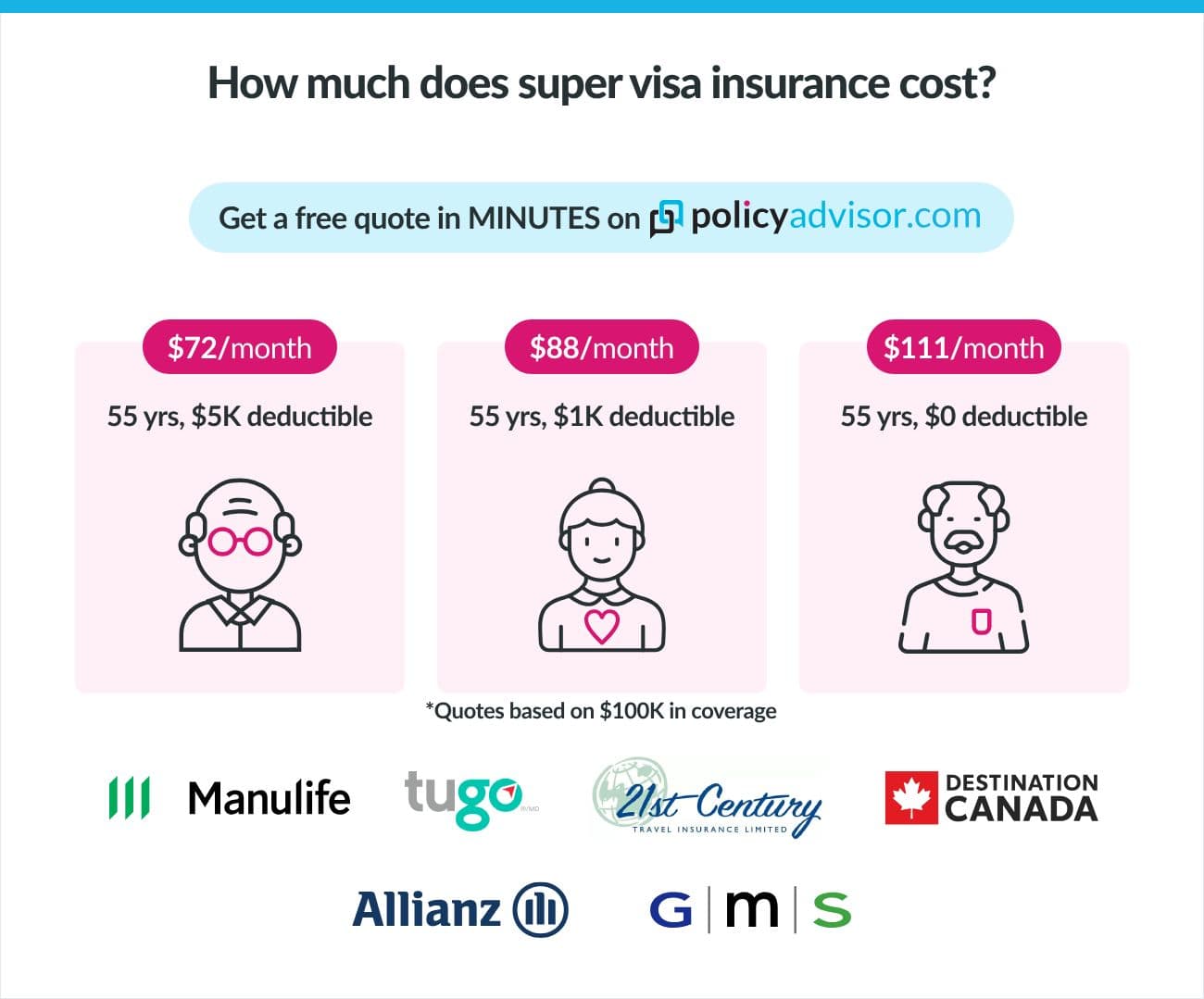

How much does Super Visa insurance cost?

Super Visa insurance can cost between $100 to $200 per month for each parent or grandparent visiting Canada. But the exact cost of Canadian Super Visa insurance fees can vary, depending on factors like:

- Age

- Health & medical history

- Policy length

- Amount of coverage

- Deductible

Originally, Super Visa insurance had to be paid in full at the time of purchase. But as of December 2022, there are options to pay in monthly installments instead. Someone can also sponsor their parents or grandparents and buy the Super Visa insurance on their behalf. Read more about Super Visa insurance payment options.

The below table shows how much Canadian Super Visa insurance might cost at different ages.

Super Visa insurance cost based on age

| Age | Total premium |

|---|---|

| 55 years | $1,110/month |

| 60 years | $1,241/month |

| 65 years | $1,588/month |

| 70 years | $2,187/month |

| 75 years | $2,713/month |

*Quotes based on a 365-day Super Visa insurance policy with $100,000 in coverage and a $1,000 deductible.

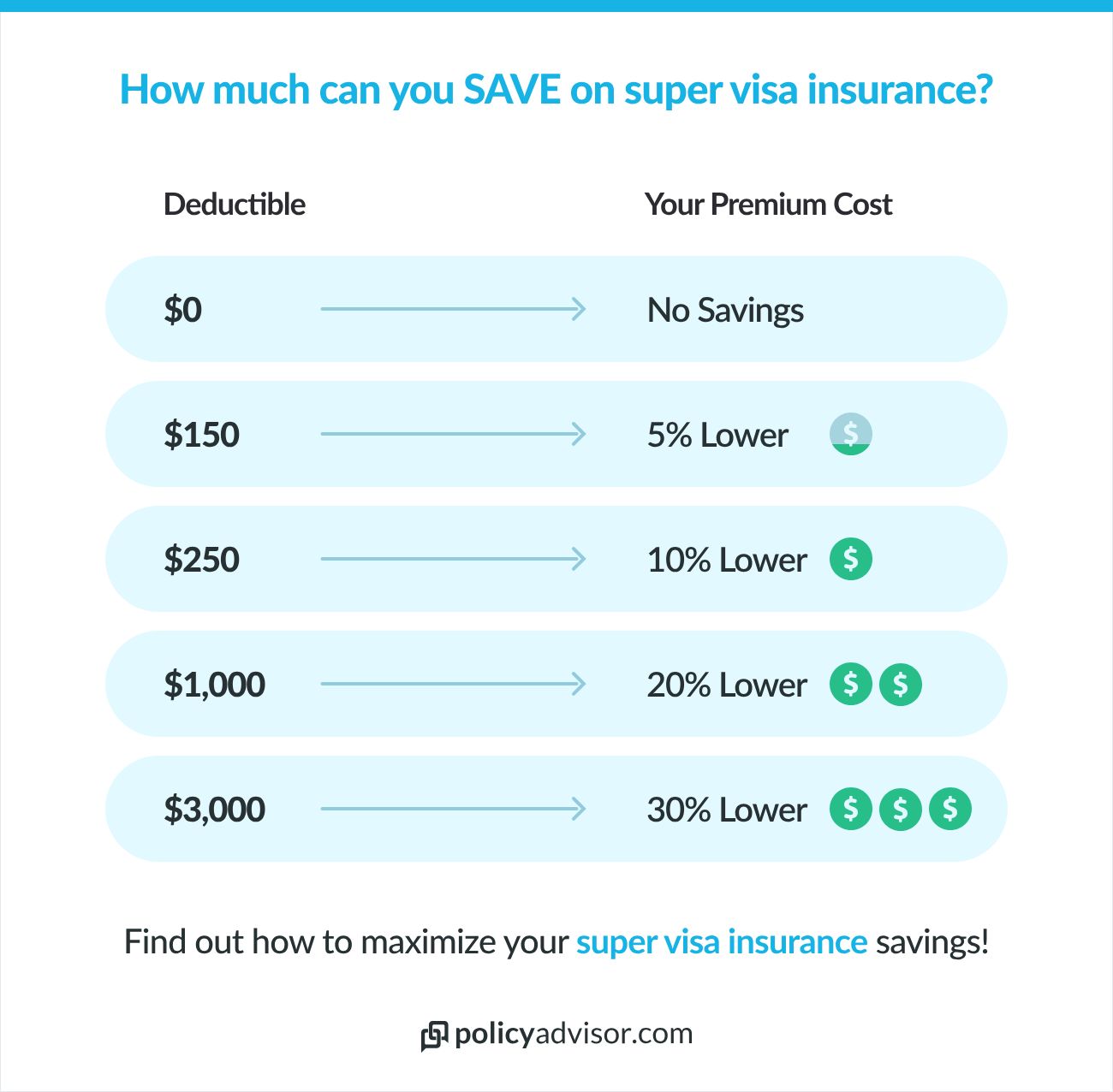

What is the deductible for Super Visa insurance?

The deductible of your Super Visa insurance policy is the amount of money you decide to pay for medical care before your coverage kicks in. Many insurance companies are offering different deductible amounts, which you can choose to lower the premium amount. Some deductibles can be zero, which means you don’t have to pay anything. Others can be thousands of dollars. You can save money on your insurance costs by choosing deductible options.

How much can you save on Super Visa insurance with deductibles?

One of the pros of choosing a higher deductible is that you will pay less monthly or annual costs for your insurance coverage. On the other hand, choosing a lower deductible is the opposite.

When you have a zero-dollar deductible, you don’t have to pay anything upfront for medical expenses. But you’ll have to pay a higher premium each month. Some people decide to pay a deductible, so their premiums are lower. They then pay for smaller medical expenses, like prescription drugs, when they need to.

Which are the best Super Visa Insurance providers in 2026?

In 2026, top Super Visa insurance providers in Canada include Manulife, Travelance, GMS, and Allianz.

- Manulife: One of the most trusted names in Canadian insurance, Manulife offers flexible Super Visa plans with comprehensive coverage. Their plans are widely accepted by immigration authorities and provide 24/7 emergency assistance

- Travelance: Known for its affordable premiums and customizable coverage, Travelance offers two plan tiers (Essential and Premier), making it easier for applicants to choose based on budget and coverage needs. They also allow higher coverage amounts and pre-existing condition protection

- GMS (Group Medical Services): GMS provides competitive rates and excellent pre-existing condition coverage for those who meet stability requirements. Their policies are ideal for seniors and long-term stays, offering coverage periods of up to 365 days

- Allianz: As a global brand, Allianz offers strong international support and robust Super Visa policies. Their plans include emergency medical coverage, repatriation benefits, and optional pre-existing condition coverage

How to apply for Super Visa insurance?

Super Visa insurance is a mandatory requirement for parents and grandparents visiting Canada under the Super Visa program. It must provide at least $100,000 in emergency medical coverage for a minimum of one year. Applying for the right plan ensures compliance with visa requirements and protects against unexpected medical costs.

Step-by-step process

- Determine coverage needs: Consider the applicant’s age, health status, and length of stay

- Speak to our licensed advisors: Our expert advisors will help you review policies from licensed Canadian insurance providers for coverage, exclusions, and cost

- Confirm eligibility: Ensure the applicant meets any medical or age-related underwriting requirements

- Purchase the policy: Buy a plan with $100,000+ coverage valid for at least 365 days in Canada

- Get proof of insurance: Obtain the official insurance certificate to include in the Super Visa application

Common application mistakes to avoid

- Purchasing insufficient coverage: Anything under $100,000 will not meet Super Visa requirements

- Overlooking exclusions: Failing to review exclusions for pre-existing conditions or age limits can result in denied claims

- Incorrect coverage dates: The policy must start on the date of arrival in Canada and last for one year

- Missing the insurance certificate: You must include proof of insurance with your Super Visa application

Can I buy Super Visa insurance on behalf of my visiting family?

Yes, Canadian citizens and permanent residents can purchase a Super Visa insurance policy on behalf of their parent(s) or grandparent(s). In fact, most do!

With a Super Visa, the person who sponsors their family’s stay in Canada is responsible for their expenses during their visit. This includes any medical expenses that may not be covered by insurance. Since sponsors are already responsible for the costs of their guests, many of them decide to buy their super visa insurance too. This helps them make sure they have the right coverage and get additional coverage if they need to.

Can I get Super Visa insurance with a pre-existing condition?

Yes, you can get Super Visa insurance with a pre-existing condition. Many Canadian insurance providers offer Super Visa insurance plans that include coverage for stable pre-existing conditions, such as diabetes, high blood pressure, or heart disease, as long as the condition has been medically stable for a specific period before the policy start date.

Key things to know about Super Visa pre-existing condition coverage

- Stability periods vary: Some insurers require your condition to be stable for 90 days, while others may require 6 to 12 months

- Premiums may be higher: Plans with pre-existing condition coverage often cost more

- Partial coverage options: Some plans offer limited coverage or higher deductibles

- Medical questionnaires required: You may need to complete a health declaration or screening

- Conditions that may be excluded: Cancer under active treatment, recent heart surgery or stroke, uncontrolled diabetes or hypertension, and conditions with recent hospitalizations

What does “medically stable” mean?

A medically stable condition means that:

- There have been no new symptoms or worsening of the condition

- No new medications or treatments were prescribed or changed

- No hospitalization, test referrals, or specialist consultations occurred for the condition

This stability must be maintained within a defined period, usually 90 to 180 days, depending on the insurance provider.

Can I get a refund on Super Visa insurance if the visa is rejected or unused?

Yes, you may be eligible for a full or partial refund on Super Visa insurance depending on your situation. Insurance providers in Canada offer flexible cancellation and refund options to help protect your investment in case plans change.

Full refund if the Super Visa is not approved

If your parents’ or grandparents’ Super Visa application is rejected by IRCC, most Canadian insurance companies will issue a full refund of the premiums paid. You will need to provide the visa refusal letter from Immigration, Refugees and Citizenship Canada (IRCC) and submit a refund request before the insurance policy start date.

Partial refund for early departure from Canada

If your parents or grandparents leave Canada before the one-year coverage period ends, you may be entitled to a partial refund for the unused portion of the Super Visa insurance. To qualify:

- The visitor must have left Canada permanently

- No claims should have been made on the policy

- You must provide proof of departure, such as boarding passes or a stamped passport

Refund amounts vary by provider and are calculated based on the number of unused months, minus any cancellation fees (if applicable).

Are there alternatives to Super Visa insurance?

No, there are no alternatives to Super Visa insurance. A hard rule for the visa to be approved is having proof of medical insurance coverage. A Super Visa medical insurance policy is the only option to meet this requirement.

But there are other visitor’s visas and immigration programs that do not need super visa insurance. They include:

- The 6-month standard visitor visa

- The electronic travel authorization (eTA) for travellers from eligible countries

- A passport for travellers from visa-exempt countries

- The Parents and Grandparents Sponsorship Program (PGP). This program lets Canadian citizens and permanent residents sponsor their parents and/or grandparents to become permanent residents of Canada.

Canadians can also consider regular travel insurance for parents or grandparents if they plan on visiting for a shorter period of time. They may not need as much coverage as insurance for a Super Visa, so they can save on costs by getting a regular plan instead.

Our advisor’s take on super visitor insurance quotes in Canada

Choosing the best Super Visa insurance policy is not just about finding the lowest premium. The right plan depends on several factors, including the traveller’s age, medical history, deductible preference, stability period requirements, and whether coverage for pre-existing conditions is needed.

For travellers with pre-existing medical conditions, TuGo often offer competitive pricing and shorter stability periods. For monthly payment options, Travelance may provide such options along with broader medical coverage.

If you want to get the best super visa insurance quotes, speaking with a licensed advisor can help families compare plans based on both price and coverage quality, ensuring the policy meets IRCC requirements while also providing suitable protection during the visitor’s stay in Canada. Schedule a call now!

Do you need to purchase a Super Visa insurance policy in Canada?

No, you do not have to physically be in Canada to buy Super Visa insurance. You just have to buy it from a Canadian insurance provider or any other insurer authorized by OFSI. But you can buy the policy whether you are in Canada or elsewhere. You can only apply for the visa itself from outside of Canada, though.

Can you get a discount if you buy several Super Visa insurance policies?

Yes, most insurance companies will give you a discount if you buy more than one Super Visa insurance policy at once. Each company has its own special offers and deals. Ask about the multi-policy discount to find out how you can save!

Do you need to take a medical test for Super Visa insurance?

No, you don’t need to go through a medical exam or do labwork to get Super Visa insurance. You will only be asked some questions about your health when you apply.

Be sure to only give honest and accurate answers to each question during the application process. If you give false information, your policy could be cancelled. And if that happens, you risk losing your visa altogether.

Can you get a refund for Super Visa insurance?

Yes, you can get a refund for Super Visa insurance. But only in some circumstances. For example, if you apply for a policy and get approved but your Super Visa application is denied. In this case, you can get a full refund for your Super Visa insurance policy.

Can you cancel Super Visa insurance?

Yes, you are allowed to cancel Super Visa insurance. But it doesn’t happen often because this kind of insurance is mandatory for the visa itself.

Let’s say your Super Visa application was accepted and you’re now using that visa to stay in Canada. You wouldn’t be able to cancel the insurance because that would also cancel your visa.

But let’s say you have to leave Canada earlier than expected, and you haven’t used your insurance plan. In that case, you can cancel your insurance policy and get some money back. But you might have to pay a cancellation fee.

Can foreign workers in Canada get Super Visa insurance for their families?

No, the parents and grandparents of foreign workers in Canada cannot get a Super Visa or insurance for a Super Visa. It’s only available to the relatives of Canadian citizens and permanent residents. Foreign workers, like international students, are considered temporary residents in Canada. But their visiting relatives can still get standard travel insurance.

Does Super Visa insurance cover dental treatment or dental emergencies?

Yes, Super Visa insurance covers emergency dental expenses. Depending on your policy, Super Visa insurance can provide thousands of dollars in coverage for dental emergencies and expenses. Note that it does not cover planned dental treatment, like cosmetic surgery.

How long does Super Visa insurance coverage last?

Super Visa insurance coverage lasts for up to 1 year at a time. It’s bought in 1-year increments, so the Super Visa holder needs to get a new policy every year they remain in Canada.

Also, keep in mind that if the visitor leaves Canada and comes back again, they will need to have new, valid Super Visa insurance coverage.

Does Super Visa insurance cover doctor visits?

No. Super Visa insurance is primarily designed to cover emergency medical expenses, such as treatment for illnesses or injuries, prescription medications, diagnostic procedures like X-rays, ambulance services (ground, air, and sea), and essential medical equipment (e.g., crutches, slings, and wheelchairs).

However, it does not cover routine doctor visits or preventive care, including planned vision and dental care.

Which providers offer Super Visa insurance?

You can get a parent/grandparent Super Visa insurance policy from some of the best visitor insurance companies in Canada, like:

- Manulife

- TuGo

- Group Medical Services (GMS)

- Allianz

- 21st Century Travel Insurance Limited

- Destination Canada

Super Visa insurance is mandatory medical coverage for parents and grandparents visiting Canada under the Super Visa program. This guide explains eligibility, IRCC requirements, coverage, super visa insurance costs, pre-existing condition coverage, deductibles, refunds, and the best insurance providers in Canada for 2026.