- There are three types of group benefit plans: traditional group health insurance, health spending accounts, and hybrid plans

- Traditional group health insurance plans provide comprehensive coverage, while HSAs offer flexibility, and hybrid plans combine both approaches

- Group health benefits typically include extended health care, dental, vision, disability, and life insurance, helping employers attract talent and support employee well-being

Employee benefits plans, also known as group benefits or employer-sponsored plans, are offered by an organization to its full-time or part-time workers. Not all group health insurance plans in Canada work the same way. Some offer comprehensive, fixed coverage through traditional insurance, while others provide flexible, employer-funded spending accounts. Choosing the right type of plan can directly impact your goals.

In this blog, we’ve explained the different types of group insurance plans that are available. If you’re an employer, looking to attract and retain talent, or an employee who wants to understand group health coverage, this blog is for you!

How much does Group Insurance cost?

Get instant quotes from Canada's top group insurance providers and find the perfect coverage for your business.

Powered by

![]()

What are the different types of group health insurance plans in Canada?

There are three types of group health insurance plans in Canada: Traditional group health insurance plans, Health Spending Accounts (HSAs), and hybrid plans.

Traditional group health insurance plans

In Canada, traditional group health insurance plans are provided by employers to their employees. These plans cover various health-related expenses that may cause financial strain for individuals or their families. The main types of coverage offered under traditional group health insurance plans in Canada include:

1. Extended Health Care (EHC) plans

EHC plans are the most common form of group health insurance plan that employers provide to their team members as an additional perk for their efforts. Most EHC plans cover a comprehensive range of healthcare facilities, such as vision care, physiotherapy, chiropractor visits, prescription drugs, and more.

2. Dental insurance plans

Apart from EHCs, many group health insurance plans also offer dental insurance benefits that protect the individual as well as their dependents from any unforeseen expenses.

Dental plans cover a range of dental care services, including routine check-ups, cleanings, X-rays, fillings, extractions, and more extensive procedures like crowns and orthodontics.

3. Disability insurance

Another form of group health insurance is disability insurance, which may be offered to employees, including both short-term and long-term coverage. Disability insurance protects an individual when their health problem prevents them from working a job and earning a steady income for their family.

Individuals with disability insurance will receive periodic payouts that will help them easily cover basic day-to-day expenses such as groceries, mortgages, children’s education, etc.

4. Employee Assistance Programs (EAPs)

EAPs help with individuals’ overall well-being and can be added as a lucrative perk to a group health insurance plan. They offer support services such as mental health counselling, legal advice, and financial planning for employees dealing with personal issues that might affect their performance at work.

5. Life insurance

This provides a lump-sum death benefit to beneficiaries if the insured employee dies. You can opt for basic life insurance or get dependant life insurance coverage and accidental death and dismemberment.

Find out more about how group health insurance can help small businesses in Canada

Health Spending Accounts (HSAs)

HSAs are unique health accounts that provide a mutually beneficial way for employers as well as employees to work with health insurance. Otherwise known as Health Care Spending Account (HCSA), HSA is more of an out-of-the-pocket payment that the employer bears for their employees.

Employer contributions to an HCSA/PHSP are generally deductible business expenses; employees receive a non‑taxable benefit. Most HSAs have a set amount of annual coverage for each employee and their dependents. Moreover, HSAs do not involve premiums or risk pooling. Instead, employers reimburse employees for eligible expenses up to a fixed annual limit, giving employers full cost control.

Hybrid plans

Hybrid plans combine traditional insurance coverage with an HSA, offering both stability and flexibility. This approach is increasingly popular among growing businesses that want to offer comprehensive group health coverage at affordable costs. These plans typically provide coverage for core benefits like life insurance, disability insurance, emergency travel medical insurance, dental insurance, and more.

The contribution towards the Health Spending Account (HSA) is predetermined by the employer. The HSA lets employers customize the plan and control costs.

Pros and cons of types of group health insurance plans

| Plan type | Pros | Cons |

| Traditional group health insurance | – Comprehensive coverage (health, dental, disability, life)

– Defined structure |

– Less flexibility |

| Health spending account | – High flexibility for employees

– No risk pooling or premium increases |

– Employees must manage spending |

| Hybrid plan | – Customizable benefits structure

– Better cost optimization |

– More complex to manage |

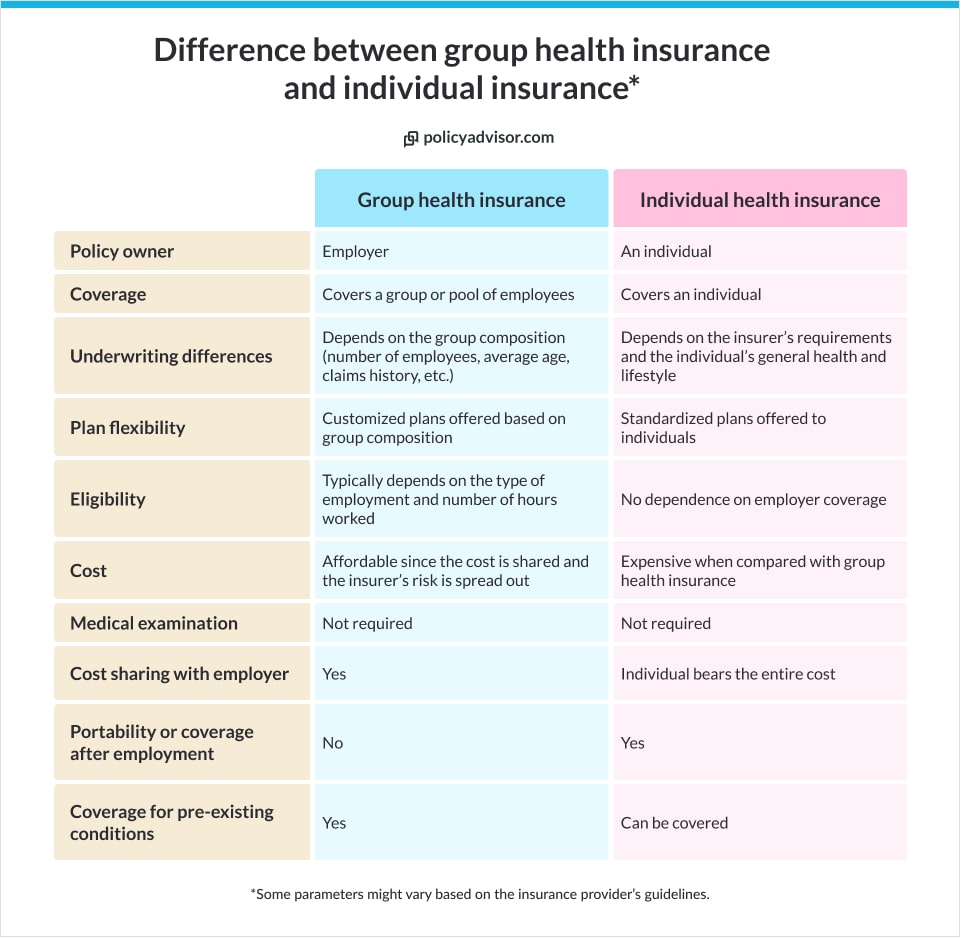

Group health insurance vs individual health insurance

The main difference between a group health plan and an individual health plan is reflected in their respective names; the former covers a “group” of employees in an organization while the latter is purchased by an individual for personal health coverage.

How can you access group benefits in Canada?

In Canada, you can access group health benefits in three ways: through employer-sponsored plans, through professional associations, and through government-sponsored benefits.

Employer-sponsored benefits

Employer-sponsored benefits are offered by an employer to the employees of an organization, forming a key part of an organization’s compensation package. Employers work with licensed experts, such as those at PolicyAdvisor or with the insurance companies directly, to obtain a group health plan that is tailored to meet the needs of the employee pool at the organization.

Employer-sponsored benefits are typically part of an employee’s compensation package and are offered as a perk. This means that the employer pays most or all of the premiums for the group health benefits being offered to their employees. Since these benefits are offered to a group of people, the premiums are lower compared to individual plans since the insurer’s risk is distributed amongst the pool of employees.

In some cases, the cost might be split between the employer and employees, especially if the latter chooses to add family members to their group health benefits plan.

Key features of employer-sponsored plans

- Some of the key features of employer-sponsored group benefits plans are:

- They can be paid for largely or in entirety by an employer

- Smaller organizations usually need 100% participation while larger ones will need 70%

- Employees can add family members to their group benefits for an additional cost

- Employer-sponsored plans are typically not portable and only last for the term of employment

- Employer-sponsored plans have limited customization

- Some organizations might exclude part-time workers or employees on unpaid leave from these plans

Learn more about how group health insurance works

Did you know?

Professional association benefits

Professional associations are organizations that offer networking opportunities to a group of people from a certain industry or profession. These associations include financial institutions, retiree organizations, college and university alumni groups, and clubs.

Professional associations offer standardized group benefits to their members and their families. Similar to employee benefits, every member can choose to get coverage for health & dental, vision, prescription medication, and paramedical services. The premiums can either be paid directly by the members or deducted from their membership fees.

Depending on the preference of the association, it might also offer life insurance, disability insurance, and accidental death and dismemberment (AD&D) insurance. For example, an armed forces or army veterans association might choose to offer life, disability, and AD&D insurance to its members while an advocacy group for a trade association might not.

Since a group of people is insured under professional association benefits, premiums will be lower, and the plans will be customizable. It is beneficial to work with licensed experts when figuring out the best group benefits for a professional association.

Key features of professional association benefits

Professional association benefits are a great way to increase and retain members of an organization. Some of the key features of these benefits include:

- Highly customizable plans, tailored based on the association’s member composition

- Lower premiums since the insurer’s risk is spread

- Group benefits are extended to family members and loved ones

- There is no portability; coverage ends when membership expires or is cancelled

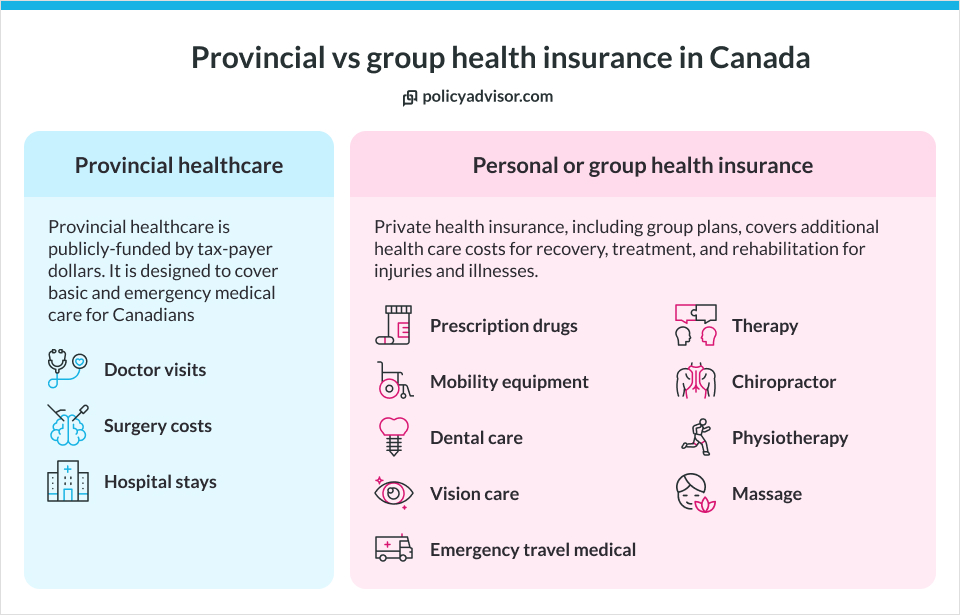

Provincial health care plans vs employee benefits plans

The Canadian government provides healthcare to all its citizens. So the question that arises is: why are group benefits plans even necessary? It’s because provincial health care plans typically cover essential medical needs such as emergency healthcare and other basic medical care that includes surgeries and doctor visits. Employee insurance plans, on the other hand, provide wider, more extensive supplementary medical coverage.

Estimating costs of traditional group health insurance

Traditional group health plans may come in several different formats with limitless customization options. Hence, it’s safe to say that the cost of this insurance plan will also vary. Although prices may fluctuate across companies depending on employee demographics, here is an estimate:

- Small businesses (up to 50 employees): The cost per employee can range from $1,500 to $4,000 per year

- Medium-sized businesses (50-250 employees): The cost per employee can range from $1,200 to $3,500 per year

- Large businesses (250+ employees): The cost per employee can range from $1,000 to $3,000 per year

Cost-sharing options for employee health benefits

Group health insurance may also be categorized based on how the insurance premium is being paid and who pays for it. Taking a look at the plethora of cost-sharing options, employee health benefits may be as follows:

- Employer pays: In this category, the employer bears the entire cost of the premium on behalf of the employee. The employer usually provides this benefit as an added perk to their dedicated workforce

- Employee pays: In this arrangement, the employee bears the entire cost of the premium. However, the employer may provide assistance with the insurance paperwork for a streamlined procedure

- Employer and employee split: This procedure allows the employer as well as the employee to split the cost of the premium. In this way, both parties may receive tax benefits and other mutual perks

- Coverage-based split: In this method, there can be different cost-sharing arrangements for different types of coverage. The cost-sharing procedure can be customized based on the agreement between the employer and the employee

Explore more about employee benefits through our detailed guide

How to choose the best group health insurance companies in Canada?

There are several insurance companies in Canada that can help build a group benefits plan for your organization. At PolicyAdvisor, we work with 30 of Canada’s top life insurance companies to get you the best rates on the benefits plans you need for your business. While all insurers offer different kinds of coverage, the best health insurance company is the one that understands your unique requirements and builds a customized plan with you.

Frequently asked questions

Is group health insurance taxable for employees?

Apart from Quebec, employer-sponsored benefits like prescription drugs, vision and dental are not taxable.

What are the different types of group health insurance in Canada?

The three types of group health insurance plans in Canada that you can choose from include traditional group plans, health spending accounts, and hybrid plans.

Which are the best group health insurance companies in Canada?

There are several health insurance companies in Canada from which to choose. Some prominent companies working with group health insurance include Manulife, Sun Life, Desjardins, Canada Life, etc. You may connect with expert insurance brokers (such as licensed experts at PolicyAdvisor) to help you understand the process.

What does a typical group health insurance plan cover?

Most group health insurance plans in Canada cover extended health care, dental care, vision care, disability insurance, and life insurance. Coverage may vary depending on the plan type and level chosen by the employer.

Group insurance plans are offered by organizations to their members or employees. There are three types of group benefits plans: traditional group health insurance, health spending accounts, and hybrid plans. They cater to employees of an organization and help in employee retention.