- There are three main types of mortgage insurance in Canada: mortgage default insurance, mortgage loan insurance, and optional mortgage protection insurance

- Mortgage insurance benefits include financial security for lenders, enabling homeownership with lower down payments, and stabilizing the housing market

- Drawbacks of mortgage insurance include high costs, impact on home equity, and provincial sales tax requirements

- Term life insurance is a cost-effective alternative offering similar protection with flexible beneficiary options and accurately determined premiums

Homeownership can be overwhelming, especially when it comes to understanding the various financial products involved. Among these, mortgage insurance is a critical component that can significantly impact your home-buying experience and financial security.

Whether you are a first-time homebuyer or looking to refinance your existing mortgage, understanding mortgage insurance is essential. So, this comprehensive guide to mortgage insurance in Canada will break down everything you need to know.

We will explore the types of mortgage insurance available, their benefits and drawbacks, the costs involved, and how they can affect your homeownership journey.

What is mortgage insurance?

In Canada, mortgage insurance is a financial protection product otherwise known as creditor insurance. It is typically offered by your mortgage lender. In the unfortunate event of your death, if your mortgage is still outstanding, mortgage insurance pays the debt you owe to your bank for your mortgage loan.

An example of how mortgage insurance works

Let’s say you are purchasing a house for $100,000.

- You pay a 15% down payment ($15,000).

- The amortization period is 25 years.

- Leaving an $85,000 mortgage loan that you need to pay off over the next 25 years.

If you die within this 25-year period, your lender still expects to be paid back. Without this insurance, your family or your estate will need to come up with $85,000 by dipping into their savings or selling the property to settle the mortgage loan.

Mortgage insurance ensures that the mortgage loan is paid off in these circumstances. This kind of insurance is sometimes referred to as mortgage life insurance or private mortgage insurance.

Read our full review of the Best Mortgage Insurance Companies in Canada.

What are the types of mortgage insurance?

There are three main types of mortgage insurance in Canada,

- Mortgage default insurance

- Mortgage loan insurance

- Optional mortgage protection insurance

Mortgage default insurance

Mortgage default insurance is mandatory coverage in Canada for homebuyers with a down payment of less than 20%. This insurance protects lenders in case the borrower defaults on their mortgage.

For example, if you buy a house for $400,000 with a 5% down payment, mortgage default insurance reduces the lender’s risk and lets you secure a mortgage despite the smaller downpayment.

Mortgage loan insurance

Mortgage loan insurance, also known as CMHC insurance, works like mortgage default insurance, protecting lenders against the risk of borrower default. This insurance allows buyers to secure a home loan with a smaller down payment.

For instance, if you put down 10% on a $500,000 home, mortgage loan insurance safeguards the lender, making it easier to obtain mortgage approval in the Canadian housing market.

Optional mortgage protection insurance

Optional mortgage protection insurance is an additional policy that homeowners in Canada can purchase to enhance their financial security. This insurance provides support to cover mortgage payments in case of unforeseen events such as disability, critical illness, or death.

For example, if the primary breadwinner in your family becomes critically ill, this insurance can help cover the mortgage payments, ensuring your family can maintain their home without facing financial hardship.

Benefits of mortgage insurance

Mortgage insurance has several advantages, like:

- Financial security for lenders: Mortgage insurance, whether mandatory or optional, protects lenders. It reduces the risk of borrower default so that lenders can recover their funds even if the borrower is unable to continue making payments

- Enables homeownership with lower down payments: Mortgage insurance makes homeownership accessible to more Canadians by allowing for smaller down payments. Without this insurance, many potential buyers would need to save for a much larger down payment, delaying their ability to purchase a home

- Access to competitive mortgage rates: With mortgage insurance, lenders face reduced risk, which can result in lower interest rates for borrowers. This can lead to significant savings over the life of the mortgage and make homeownership more affordable

- Stability in the housing market: Mortgage insurance contributes to the stability of the Canadian housing market by protecting lenders from widespread defaults. This stability can help prevent housing market crashes and maintain overall economic health

- Stabilizes the housing market during economic downturns: During economic downturns, mortgage insurance plays a crucial role in stabilizing the housing market. By protecting lenders, it helps prevent a surge in foreclosures and supports market stability

- Flexibility for borrowers: Mortgage insurance provides flexibility for borrowers to purchase a home sooner with a lower down payment. This flexibility can be crucial for first-time homebuyers or those looking to upgrade to a larger property

- Enhanced borrower qualifications: With the protection of mortgage insurance, lenders are often more willing to approve borrowers who may not meet traditional lending criteria. This can include individuals with lower credit scores or those with less established credit histories

Drawbacks of mortgage insurance

While mortgage insurance comes with several benefits, it also has a few drawbacks:

- High costs and added interest on premiums: Premiums can be high, and if added to your mortgage balance, you’ll pay interest on them over the life of the loan, raising the total amount paid

- Impact on home equity: Premiums added to your loan balance can slow the rate at which you build equity in your home

- Provincial sales tax requirements: In some Canadian provinces, mortgage insurance premiums are subject to provincial sales tax, increasing the overall cost

- Long-term cost: While enabling homeownership sooner, the long-term cost of paying premiums over several years can be substantial

Key differences in insurance types

Mortgage Default Insurance vs. Mortgage Protection Insurance

Here’s how mortgage default insurance and mortgage protection insurance differ:

| Feature | Mortgage Default Insurance | Mortgage Protection Insurance |

| Purpose | Protects the lender in case the borrower defaults on the mortgage | Protects the borrower by covering mortgage payments during unforeseen events like illness, disability, or death |

| Mandatory/optional | Mandatory for down payments less than 20% | Optional |

| Who it protects | Lender | Borrower and their family |

| When it’s required | Required by lenders for high-ratio mortgages | Can be purchased at any time by the homeowner |

| Cost | Added to the mortgage and can increase monthly payments | Separate premium paid by the homeowner |

| Coverage | Covers the lender’s loss in case of default | Covers mortgage payments or remaining balance upon certain conditions |

| Benefit payout | Paid to the lender | Paid to the borrower or their family |

| Eligibility | Based on the down payment amount | Based on the borrower’s health and risk factors |

| Tax treatment | Premiums are not tax-deductible | Premiums may be tax-deductible under certain conditions |

To learn more about how mortgage default insurance works and how much it costs, head to our CMHC Mortgage Default Insurance Calculator.

Is mortgage loan insurance the same as mortgage protection insurance?

No, mortgage loan insurance and mortgage protection insurance are not the same. Mortgage loan insurance is mandatory for homebuyers who make a down payment of less than 20%. Mortgage protection insurance is optional. Here are some of the key differences between the two:

Mortgage Loan Insurance

- Often referred to as CMHC insurance, mortgage loan insurance is mandatory for homebuyers who make a down payment of less than 20% of the home’s purchase price

- This insurance protects the lender against the risk of borrower default. It ensures that the lender can recover their funds even if the borrower is unable to continue making mortgage payments

- The cost of mortgage loan insurance is typically added to the mortgage amount, which can affect monthly payments and the overall cost of homeownership

Mortgage Protection Insurance

- It is an optional policy that homeowners can purchase to protect themselves and their families

- This insurance provides coverage in case the homeowner experiences a critical illness, disability, or death

- The benefits of mortgage protection insurance are paid directly to the borrower or their family, helping to cover mortgage payments or pay off the remaining balance

- Unlike mortgage loan insurance, mortgage protection insurance is not required by lenders and serves to offer additional peace of mind and financial security to the homeowner

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

Do I need to buy mortgage insurance?

No, mortgage insurance is not mandatory to qualify for your mortgage. But your lender making it seem like it is. That’s because it protects them—not you.

However, it is smart to consider protecting the outstanding balance of your mortgage. A term life insurance policy that matches your mortgage term is a cost-effective way to protect your mortgage debt.

Read more about if life insurance is mandatory to qualify for a mortgage.

Mortgage insurance alternatives

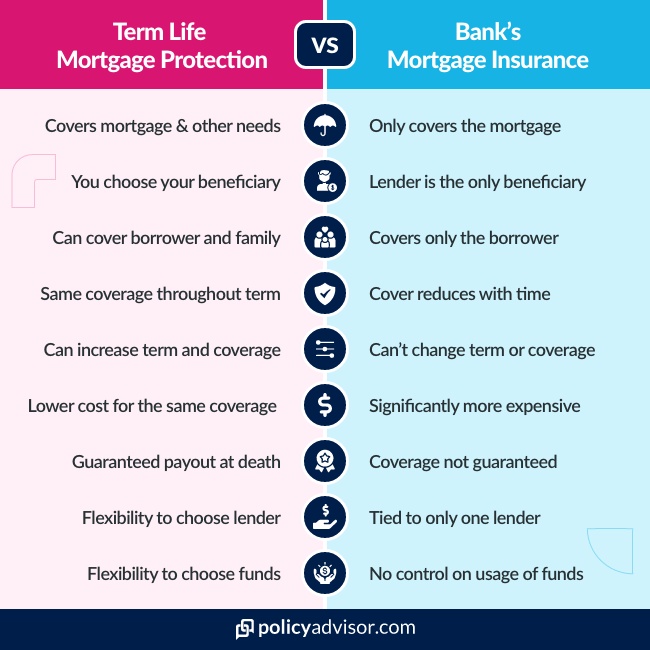

Term life insurance can provide the same security as traditional mortgage insurance. This alternative is referred to as mortgage protection insurance. It is usually a more affordable option and provides more flexible coverage.

How to cover a mortgage debt with life insurance

Protecting a mortgage with life insurance works by getting term life insurance that is in force during the amortization period of your mortgage.

Your beneficiaries are entitled to a tax-free death benefit that never reduces and can be applied to whatever they choose through mortgage protection insurance.

Private mortgage insurance, as it is sometimes called, offers the same security throughout the riskiest years of your mortgage loan, with several additional benefits not offered by conventional loan insurance:

- You can get coverage well beyond the amount of your mortgage balance

- You get to pick your own beneficiary, instead of paying for insurance to protect the lender

Learn more about mortgage protection through term life insurance.

Mortgage insurance vs term life insurance – which is better?

While mortgage insurance pays off one’s mortgage in the event the borrower dies, other products can do a better job at protecting a mortgage debt.

A term life insurance policy can offer you better mortgage protection in a number of ways:

- The policyholder chooses the beneficiary

- In turn, the beneficiary can choose exactly how the benefit is used

- The benefit can go towards paying off the mortgage and/or other uses, like servicing other debts or handling final expenses

Learn more about mortgage insurance versus life insurance.

How much mortgage insurance do I need?

How much mortgage coverage you need depends on the value and cost of your home and several other facts. Unfortunately, you don’t get much of a choice if you go through your lender – the coverage amount is tied to the value and term of your mortgage loan.

However, life insurance allows you to cover your mortgage loan balance and many other financial needs, including:

- child care

- education costs

- your family’s future living expenses

- funeral expenses

- anything your beneficiaries wish

Our insurance calculator can help you find out exactly how much coverage you need.

Learn more about how much life insurance you need.

How much does mortgage insurance cost?

The cost of mortgage insurance can be 2-4 times as much as a term life insurance policy. In the below table, you can see just how affordable term insurance can be.

| Coverage | 10-Year Term | 20-Year Term |

|---|---|---|

| $250,000 | $11/month | $14/month |

| $500,000 | $15/month | $22/month |

| $1,000,000 | $24/month | $35/month |

*Premium payments for female, non-smoker, 30-years old

Why is mortgage insurance expensive?

Lender-provided mortgage insurance is expensive because there is no underwriting. Underwriting is the process an insurance company goes through to determine the appropriate fees for taking on the financial risk of your death.

Without this stringent evaluation process, they are more blindly taking on the financial risk of your policy paying out.

Read more about why mortgage insurance is so expensive.

Where do I get mortgage insurance?

You can only get mortgage insurance from the lender who provided your mortgage loan.

However, term insurance is available from several companies nationwide and the expert advisors at PolicyAdvisor have reviewed them all. We can help you find the best provider to protect your mortgage and make insurance part of your financial plan. Contact us below for advice on protecting your foray into the real estate market, or other needs like critical illness insurance or disability coverage.

Frequently asked questions

How long does it take to get an insured mortgage?

It generally takes anywhere from a few days to a couple of weeks to get an insured mortgage in Canada. However, the duration can vary depending on several factors, such as the lender, the complexity of your financial situation, and the completeness of your application.

Why is mortgage insurance often considered expensive?

Mortgage insurance is often considered expensive because it adds a significant cost to your mortgage payments. The premiums for mortgage loan insurance are typically added to your mortgage balance, which means you pay interest on them over the life of the loan. Additionally, if you choose to pay the premiums upfront, it can be a substantial amount that makes homeownership more expensive.

Can I cancel my mortgage insurance?

In most cases, you can cancel your mortgage loan insurance once you have paid down your mortgage to less than 80% of the home’s value, meaning your loan-to-value ratio is less than 80%. However, if you have opted for optional mortgage protection insurance, you can typically cancel it at any time, but this will depend on the terms of your policy.

How are mortgage insurance premiums calculated?

Mortgage insurance premiums are typically calculated as a percentage of your loan amount. For mortgage loan insurance, the premium rate varies based on the size of your down payment and the loan-to-value ratio.

For example, the premium might be higher for a smaller down payment. Optional mortgage protection insurance premiums are based on factors such as your age, health, and the amount of coverage you choose.

Is mortgage insurance a one-time payment?

No, mortgage insurance, typically offered by your lender, is not a one-time payment. It is generally included in your monthly mortgage payment and can only be canceled once you reach 20% equity in your home.

Do you have to pay mortgage insurance up front?

Yes, you can pay your entire mortgage insurance premium upfront, especially if you have sufficient funds to cover the downpayment, premium expenses, and other initial costs. Paying your mortgage insurance premium upfront can help lower your monthly mortgage payments.

What age does mortgage insurance end?

In Canada, mortgage insurance, also known as mortgage life insurance or private mortgage insurance (PMI), automatically ends when you reach the age of 70.

Mortgage insurance is typically offered by a mortgage lender. The coverage pays off your mortgage debt if something happens to you if your mortgage is still outstanding. Your home is often your most valuable asset, both financially and emotionally, and it’s important it is protected should something unfortunate happen to you. Term life insurance is often a more flexible and cost-effective way to cover your mortgage debt.