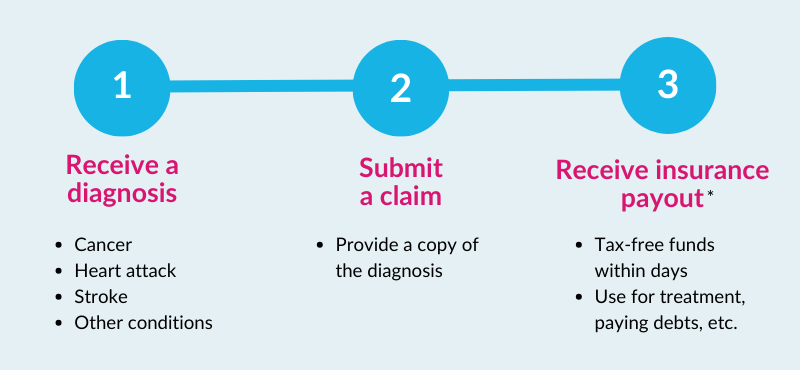

- If you have critical illness insurance and are diagnosed with a covered condition, you will be paid a one-time lump sum benefit

- The tax-free lump sum payment can be used to replace your income, pay mortgage and other loan payments, and support your family

- Critical illness insurance is beneficial if you need financial support beyond hospital treatment, especially for a long-term recovery or specialized treatment outside of Canada

Each year, thousands of Canadians are diagnosed with serious health conditions like cancer, heart attack, and stroke—life-altering events that bring unexpected financial challenges, from higher expenses to lost income to lifestyle adjustments.

Critical illness insurance provides financial protection during these difficult times through a lump sum payment upon diagnosis of a covered condition. In this post, we’ll explore how critical illness insurance works and help you decide if it’s a worthwhile investment for your future.

What is critical illness insurance?

Critical illness insurance is an agreement you make with a life insurance company that they will pay you a tax-free lump-sum of money if you…

- develop a life-threatening illness

- have a serious health event

- or undergo treatment while under their coverage

Unlike life insurance, the payout doesn’t happen after you die. It’s a living benefit you receive while you are alive to help with immediate financial burdens of a critical illness. You get the payout once proof of a specified illness or incident is established (barring any policy waiting period).

How does critical illness insurance work?

Critical illness insurance (also known as CI insurance) works by offering financial support should you or your family member be diagnosed with a serious illness such as cancer, heart attack, or stroke.

Just like with life insurance, you’ll be required to pay monthly premiums over the course of your term length to maintain that protection. Both the amount of the benefit and the monthly payments are decided when you apply for the policy.

During your policy term, if you are diagnosed with a critical illness, you submit a claim that includes your official diagnosis documentation. Then the insurance company pays you the benefit.

*Subject to waiting period

Is critical illness insurance taxable?

No, the lump sum payment received from a critical illness insurance policy is generally tax-free in Canada. This tax-free benefit helps policyholders use the payout for necessary expenses without worrying about deductions. However, exceptions apply if the policy is owned by a business and premiums were deducted as a business expense.

Common uses for critical illness insurance

The payout (or benefit) from a critical illness insurance policy can help replace lost income, support personal and family needs, and pay a mortgage and other loan payments.

Let’s look at the different ways to use a critical illness insurance benefit:

Replacing income

For you or your family to take time off work.

Debts

Mortgages, business loans and other liabilities.

At-home care

Hiring nurses or other home-care practitioners.

Prescription medicine

Out-of-pocket expenses not covered by provincial plans

Enhanced care

Upgraded medical facilities and services

Modifications

Renovations or modifications to your home, car, or other household expenses

Additional treatment

Out-of-country or alternative medical expenses

Savings protection

Eliminate the need to use retirement savings

What illnesses are covered by critical illness insurance?

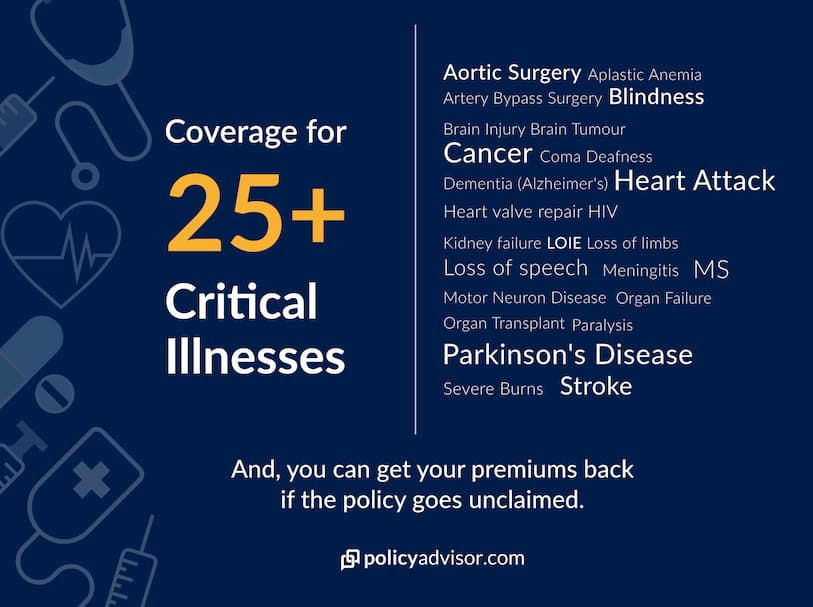

Critical illness insurance in Canada covers over 30 life-threatening conditions, including cancer, heart attack, kidney failure, and stroke. These conditions are selected because they often involve high medical costs and lifestyle changes that impact your ability to work.

Here’s a list of conditions usually covered by critical illness insurance:

Basic critical illness coverage

- Cancer

- Heart attack

- Stroke

Enhanced critical illness policy coverage

- Acquired Brain Injury

- Aortic Surgery

- Aplastic Anemia

- Blindness

- Bacterial Meningitis

- Cancer

- Coma

- Coronary Artery Bypass Surgery

- Dementia, including Alzheimer’s Disease

- Deafness

- Heart Attack

- Heart Valve Replacement or Repair

- Kidney Failure

- Loss of Independent Existence

- Loss of Limbs

- Loss of Speech

- Major Organ Failure on Waiting List

- Major Organ Transplant

- Motor Neuron Disease

- Multiple Sclerosis

- Occupational HIV Infection

- Paralysis

- Parkinson’s Disease

- Severe Burns

- Stroke (Cerebrovascular accident)

What is partial payout in critical illness insurance policies?

A partial payout allows you to receive a portion of your critical illness insurance benefit if you’re diagnosed with an early-stage or less severe covered condition.

Partial payment details:

- The specified illnesses will be made clear to you before your coverage begins

- Often non-life-threatening cancers fall into this category

- This clause allows you to receive some money (typically between 10-25 percent of your coverage amount and is subject to dollar value limits) during your recovery

- You can maintain your protection should you contract a terminal condition down the road

The conditions eligible for partial payment vary from company to company.

Some conditions eligible for partial payout are:

- Early thyroid cancer

- Early prostate cancer

- Stomach tumours

- Superficial skin cancers

- Ductal breast cancers

- Coronary angioplasty

Can I receive multiple critical illness insurance payouts if I am diagnosed with multiple conditions?

Yes. It is possible to receive multiple payouts on a critical illness insurance policy for partially critical conditions. However, coverage only pays out once in its entirety for fully critical conditions. The amount of times you can claim partial conditions depends on your policy wording.

How much does Critical Illness Insurance cost?

Get instant quotes from Canada's top critical illness insurance providers and find the perfect coverage for your family.

Powered by

![]()

How much does critical illness insurance cost?

In general, you can expect to pay anywhere from $21-70 per month for critical illness insurance. On average, it’s more expensive than term life insurance but not so expensive that you can’t afford it. Just like life insurance, the younger and healthier you are, the less expensive your critical illness insurance premium is.

Coverage amounts are smaller than what you’d see for a life insurance death benefit, so that also helps keep premiums low. Canadians typically elect for an average critical illness coverage of $77,000 according to the Canadian Society of Actuaries.

Other factors that can affect the cost of premiums include:

- your term length

- the number of conditions covered by your policy

- any riders or clauses you opt for

- smoking status

Critical illness insurance riders

Some companies allow you to add riders to a critical illness insurance policy that can add coverage or return your premiums. With some policies, you may be able to choose the number of illnesses covered as well as the amount of coverage and the term length of the rider. Critical illness riders typically have a 30 day survival period that needs to be completed, before the policy can pay out the proposed benefit of the rider.

Child critical illness rider

A Child Critical Illness rider provides coverage for the insured’s children if they are diagnosed with a childhood illness. The exact list and number of illnesses covered vary across insurers.

Return of Premium on Death rider or Expiry rider

A Return of Premium on Death or Expiry rider returns all or a part of the premiums one has paid over the course of their policy when the policy term ends or when the individual passes away.

Is critical illness insurance worth it?

Yes, critical illness insurance is worth the money. Critical illness insurance is protection you buy to protect you and your family from the financial fallout that happens if you get critically sick. If you want the financial freedom to recover from a serious illness on your own terms, then you need this type of insurance.

Because critical illness insurance pays a living benefit, getting coverage is even more of a personal decision than life insurance. Life insurance is really about your family’s needs. Critical illness insurance is about your financial needs while you recover.

Look at the stats:

- 1/2 of Canadians will be diagnosed with cancer in their lifetime

- The average out-of-pocket expenses for cancer in Canada is around $400 a month. This excludes treatment covered by public or private health care and can be more depending on the type of cancer

- When you’re diagnosed with cancer, you’ll likely have to take time off work to recover

So, can you afford to take time off work, cover your usual bills, plus at least $400 a month to pay for your treatment/recovery? If you can’t, critical insurance is worth it.

Buying this insurance can give you the peace of mind to know, that if you’re facing a critical diagnosis, you’ll be able to focus completely on recovery.

Learn more about whether critical illness insurance is worth it.

| Advantages | Disadvantages |

| Financial protection for your family | More expensive than life insurance |

| Flexibility in how benefit is used | Some companies only offer basic policies |

| Premiums can be returned if there are no claims | |

| Ability to get coverage as a rider or separate policy |

Can I get life insurance and critical illness insurance together?

Yes, many Canadian insurance companies offer life insurance and critical illness coverage together. You can add critical illness coverage as a rider to your life insurance policy. This can help you apply for both life insurance and critical illness coverage at the same time without having to go through underwriting again.

Learn more about critical illness insurance versus critical illness riders.

How much critical illness insurance coverage do I need?

In general, Canadians commonly purchased between $50,000 and $100,000 in coverage or more.

Because the coverage pays a living benefit, it’s intended to cover a shorter period of time, specifically while you are treating and recovering from an illness. Hopefully, your recovery will be swift, and you wouldn’t be reliant on the money paid out by your policy for the remainder of your life.

If you’re unsure how much coverage you want, an insurance calculator can suggest a coverage amount based on your estimated needs and give you an estimate of the monthly expenses associated with the policy.

Learn your coverage needs with our critical illness insurance calculator.

Which are the best critical illness insurance companies in Canada?

We reviewed the top companies offering such policies so you can make an informed decision on your critical illness insurance provider. Companies like Canada Protection Plan (which allows credit card payments), Sun Life, Canada Life, BMO Insurance, and more offer critical illness benefits in Canada.

Read more about the best critical illness insurance companies in Canada.

How can I get my critical illness insurance quotes?

Still have questions? Schedule a chat with a licensed insurance agent from PolicyAdvisor. They’re happy to go over anything you’re curious about and provide you with many quotes from the best insurance companies in Canada. Save time and money when you speak to our brokers, form your life insurance plan, and compare quotes online.

Frequently asked questions

How often do critical illness insurance payout?

On average, about 80 percent of critical illness insurance claims are approved, and this percentage continues to rise. Approval rates vary by provider, which is why you should research different companies and understand their coverage definitions and waiting periods before purchasing a policy.

Which three illnesses are covered under most critical illness policies?

Cancer, heart attack, and stroke are covered under most basic critical illness insurance policies. Enhanced policies may include up to 26 conditions or more.

How much is the maximum coverage for critical illness?

The maximum amount of coverage offered by Canadian critical illness insurance providers is $3 million. Usually, Canadians get $50,000 – $100,000 in critical illness coverage.

Do you need critical illness or disability insurance?

You need both critical illness insurance and disability insurance to fully financially protect yourself from injury or illness. They are two different insurance products. Critical illness insurance will pay you a lump sum payment if you are diagnosed with a critical illness.

Disability insurance will replace a portion of your income if you are sick or injured and cannot work. Both products will help ensure your family is financially taken care of if you become very sick.

Can I be refused critical illness coverage?

The average Canadian resident should have their application accepted depending on their history. However, you can be refused or denied coverage by the insurance carrier you applied to.

You and your family’s medical history will factor heavily into the underwriting process. If you have already been diagnosed with an illness, or have pre-existing conditions your likelihood of being insured or availability of coverage options may be reduced.

Will I get my money back if I do not claim on my critical illness policy?

Yes, some critical illness policies allow for a return of premium. Some insurers will return all of the premiums you’ve paid if you haven’t made a successful claim at the end of your term, hit certain age milestones, or surrender your policy.

This is an optional clause and it will increase the cost of premiums.

There’s also a return of premium on death clause, which means your premiums will be paid back to your chosen beneficiary should you pass away unexpectedly, without receiving a full benefit payment under your critical illness policy.

Do you have to spend a critical illness insurance payout on treating your illness?

No. You only need to be diagnosed with a covered condition to receive your critical illness insurance benefit. The tax-free payment can be used however you choose—whether for medical expenses, replacing lost income, supporting family needs, hiring care providers, or seeking treatment abroad.

What is the survival period in critical illness insurance?

In order to get your payout, you must pass the 30-day survival period after your diagnosis. This waiting period is consistent across most insurance companies and covers most types of diseases. Some companies now permit a zero-day survival period for certain conditions.

If I get better, do I have to return the benefit?

You do not have to give back your critical illness payout if you recover from the covered medical condition. Critical illness plans are not defined by recovery, treatment, or death. It is a one-time payment that is triggered by the diagnosis of specific diseases or conditions.

Critical illness insurance coverage differs from other types of insurance in that it is a living benefit that pays out a one-time lump sum.

- Term life insurance – pays out after your death

- Long-term care insurance – pays for assistance for those who can no longer take care of themselves

- Disability insurance – pays out monthly if you cannot work due to an illness or disability

- Critical illness insurance – pays out a one-time lump sum when you are diagnosed with a life-threatening illness or disease

Critical illness insurance is an agreement with an insurance company where they pay you a tax-free amount of money if you are diagnosed with a life-threatening condition or illness. You can spend this money how ever you choose, but it usually goes toward treatment plans, travel, covering bills, and other financial needs you family may have while you recover. This coverage can be purchased as an independent policy or in combination with life insurance products.