- Group life insurance is a master insurance contract designed to cover a group of people at a company or organization.

- Group life insurance provides a death benefit and life insurance to the family of the employee.

- Employer-offered coverage covers you and your dependents until your employment period ends. If you quit or are fired, your coverage ends.

- Life insurance through group benefits is not a guarantee. An individual term life insurance policy offers the most comprehensive benefits

Getting individual or private life insurance to supplement your group life insurance plan is usually recommended to ensure you have adequate coverage. Almost 39% of life insurance policies in Canada are through group term insurance. With such a large number of Canadians covered through their work, many are under the impression that it’s enough coverage for their family too.

However, group life insurance plans have limitations and restrictions, and offer limited coverage. Read on to know more about group and individual life insurance plans, their advantages and disadvantages, and more.

What is life insurance?

Life insurance is an agreement between you and an insurance company that in the event of your demise, they will pay a lump sum, tax-free death benefit to someone you choose (your beneficiaries). In exchange, you agree to pay a premium to the insurance company.

There are two main types of life insurance plans that an individual can choose from:

- Term life insurance that lasts for a specific period of time, generally 10, 20, or 30 years

- Permanent life insurance which covers you for your entire life and generates a cash value component. Some policies also pay dividends depending on your plan type

Life insurance can be bought by an individual (personal life insurance) or offered by an employer as part of a group plan.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What is group life insurance?

A group life insurance is a contract or an agreement that promises to pay an employee’s dependents a tax-free lump sum amount in the event of their demise. It is offered by an employer to a “group” of people—the employees. A group life insurance policy helps soften the financial impact that comes with losing an earning member of a family.

Most group life benefits are offered as term life insurance that is renewed annually by the insurance provider. Unlike whole life insurance which covers an individual for their entire lifespan, term life policies provide coverage for a certain “term” or fixed period of time.

Do I need individual life insurance if I am covered through work?

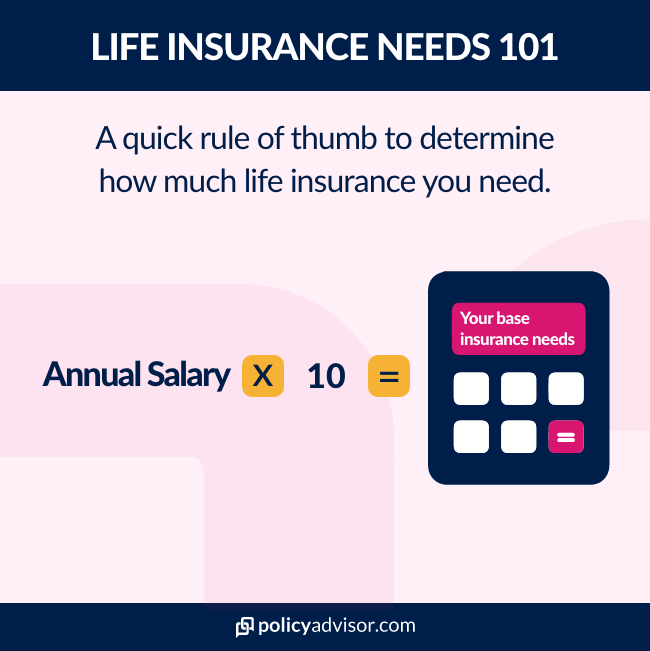

Yes, supplementing your group life insurance with individual life insurance coverage is highly recommended. Group life insurance plans generally payout up to one or two years of your salary. This may not always be enough for your family after you pass away.

To ensure your family’s living expenses, your funeral fee, your children’s education costs, and other expenses, are covered, you need to get individual life insurance. When you buy an individual life insurance plan, you also get the option to get a participating whole life insurance policy. This type of policy gives you a cash value component and dividends, both of which can be accessed while you’re alive or after your demise.

What is the difference between group and individual life insurance?

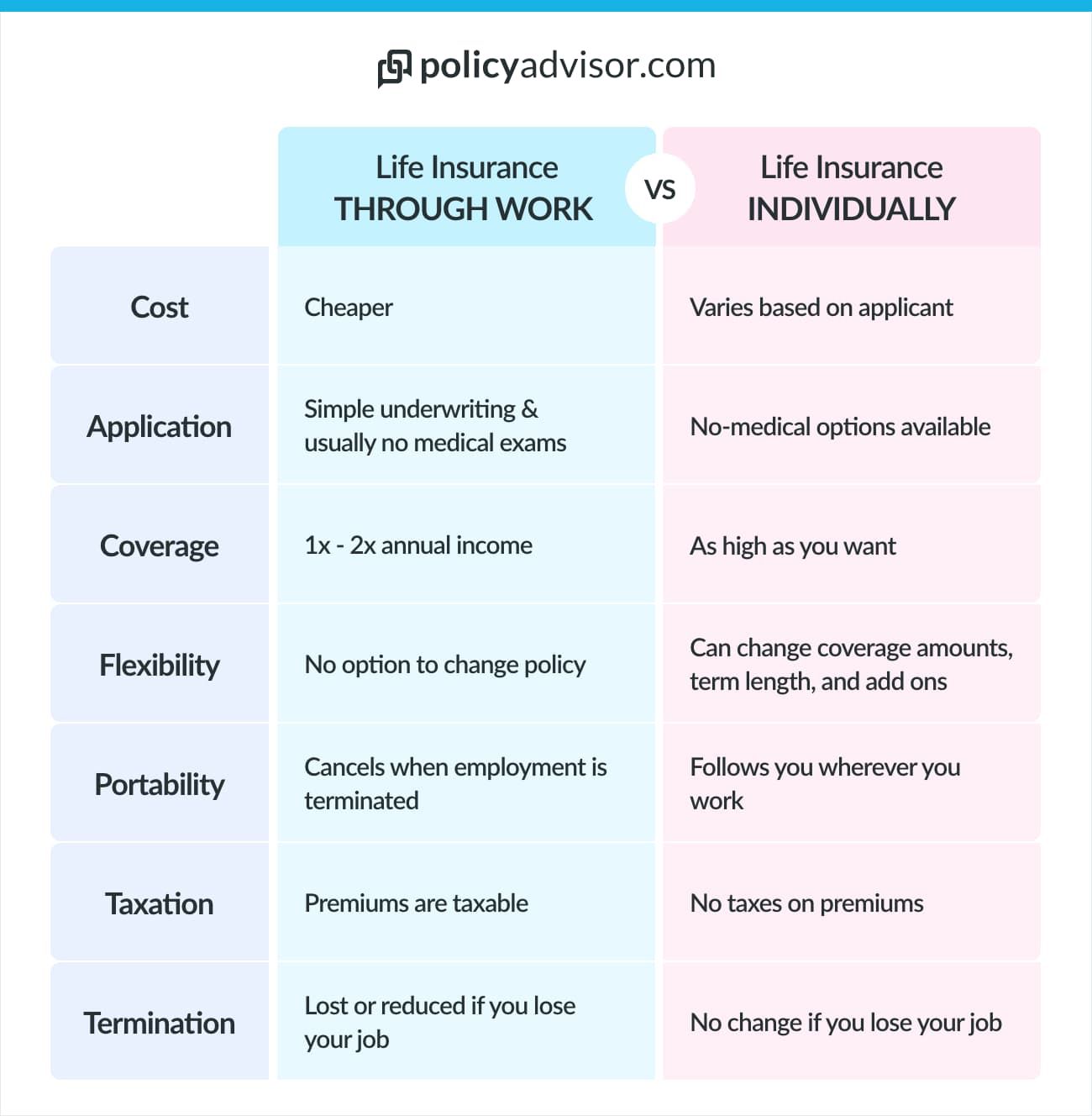

Group life insurance is offered by an employer to a group of people (the employees), while individual life insurance only covers the primary policyholder. Group life insurance plans offer limited coverage and the plan details are designed based on the employer’s budget and recommendations. Individual life insurance policies are customized to fit the needs of the policyholder. It lets policyholders choose their coverage amount, duration, and add additional riders to their core plan.

Difference between group and individual life insurance

| Feature | Group life insurance | Individual life insurance |

| Coverage type | Usually offered as a term life insurance plan to all group members | Individual policyholders can choose between term and permanent life insurance plans depending on their financial requirements |

| Premiums | Lower premiums since the insurer’s risk is spread in a larger pool | Typically more expensive since the policies are customized for an individual |

| Portability | Coverage is tied to employment—if you leave your job, you are likely to lose coverage | Coverage lasts for as long as you pay your premiums or your policy’s duration |

| Flexibility | Limited | Highly flexible |

| Tax implications | Tax benefits are generally limited to premiums paid by the employer, and employees may not receive additional tax deductions | Premiums paid can often be deducted from taxable income under certain conditions, providing potential tax advantages |

What type of life insurance do employers offer as a group benefit?

Most employee life insurance is term life insurance. Although other types of permanent life insurance are also sometimes offered.

With group term life insurance plans, the death benefit is offered as a flat dollar amount, as a multiple of an employee’s annual salary (such as one or two times your annual salary), or a mix of both.

Do employers pay for group term life insurance?

Most private employers will pay for a substantial, if not the entire, portion of the premiums for group life insurance. The only thing to note: the coverage offered is typically basic. This means there is no customization or riders built in. The cost of additional supplementary coverage is usually paid for by the employee.

What are the benefits of group life insurance?

There are a number of benefits of group life insurance that make it an attractive option for those who are offered it through work or a professional association.

Affordability: An employer often pays for most – if not all – of the life insurance premium so there is very little or no cost to the member of the plan. If you do need to pay a portion of the premiums, they are usually less expensive. This is because the insurance company prices it on the basis of the underlying risk profile of the entire group as a whole rather than as an individual insurance applicant.

Convenience: It’s easy and convenient to sign up with only a small amount of paperwork and no individual underwriting. The payments are usually through payroll deduction, so no worries about policy lapsing because you missed your premium payments.

Limited underwriting: Most group term life contracts do not require any medical exam to be administered to the individual plan members. Members may be automatically or voluntarily enrolled in the overall group life insurance plan. However, an eligible employee may be required to go through medical underwriting, to establish good health in special circumstances such as when seeking an amount higher than the group coverage or when trying to rejoin the plan, after initially declining coverage.

What is the main disadvantage of group life insurance?

The main disadvantage of group life insurance is the one-size-fits all approach that assumes that every member of the group is likely to need the same amount of coverage. This is not always the case and life insurance coverage should be customized to individual needs.

Other disadvantages of a group life insurance policy are:

Lack of control: Another disadvantage is that the plan sponsors (i.e. the employer or the organization) or even the insurance company can change the plan anytime they choose or even discontinue it altogether. Because you are sharing a plan among others in a group, it cannot be tailored to meet your own unique needs. There may be exclusions for medical conditions that you may have.

Limited portability: Group life insurance is dependent on an individual’s affiliation with the group. Just because one particular job includes insurance, there’s no guarantee that the next one will. If you find yourself in a position where you need to purchase life insurance once you make a career change, your premiums are likely to be much higher by then as you are a little older and more expensive to insure from an underwriting perspective.

Taxation: Lastly, depending on how your employer structured the benefit fees, you might need to pay taxes on the payout.

What happens to my group life insurance coverage if I leave my employer?

Employer-offered life coverage is linked to your employment. This means it covers you and your dependents until your employment period ends—whether you quit or you’re fired by the employer.

Many employer-offered plans include an option to convert the group coverage to an individual policy, upon leaving the employer. However, the cost of conversion from group to individual coverage is significantly higher and most people tend to get new individual coverage at that time.

Typically, only those individuals who may have pre-existing health conditions, and may find it hard to get individual coverage based on a medical exam, will take advantage of this conversion option.

Frequently asked questions

Does life insurance cover job loss?

No, life insurance does not cover job loss. It pays your beneficiaries a lump sum of money in the event that you, the employee, pass away. Job loss insurance is a separate insurance product. Disability insurance provides income replacement (usually 60-80%) in the event that you are injured or ill and can no longer work.

Does group life insurance end at retirement?

Yes. Group life insurance is dependent on your continued employment; therefore, at retirement, your group life insurance also expires. However, as mentioned above, you will typically have the ability to convert the group plan into individual coverage, without providing any evidence of good health. The conversion has to be requested within a limited period of time, usually 31 days. The conversion option is much more expensive since no evidence of good health is provided.

Are my dependents covered through employer life insurance?

Sometimes. Most employer-offered life insurance plans will allow an employee to extend coverage to also include their dependents, such as married or common-law spouse and dependent children up to a certain age, such as 21 years. But that’s not always the case, so check your policy documents!

Is group life insurance a taxable benefit?

Yes, employer-paid life insurance is considered a taxable benefit. With group term life insurance paid by the employer in Canada, the premiums appear on your T4 slip and are reported on your tax return as a taxable benefit.

Many people have life insurance coverage through their work and don’t look into individual life insurance coverage. But the fact is, group coverage often fails to meet your coverage needs when you need it most. The benefits of group life insurance include its affordability, convenience, and limited underwriting. The disadvantages include its limited coverage, the lack of control of the policy, limited portability, and taxation. An alternative that we suggest is an individual term life insurance policy.