- Job loss insurance helps cover eligible debt payments such as mortgages, personal loans, and credit cards if you lose your job involuntarily

- Most policies require you to be a permanent, full-time employee

- Most policies provide benefits for 6 to 12 months, although the duration and monthly payment limits vary by insurer

- Job loss insurance does not cover voluntary resignation, dismissal for misconduct, or known layoffs

- What is job loss insurance in Canada?

- Types of job loss insurance in Canada

- Who is eligible for job loss insurance in Canada?

- How does job loss insurance work?

- What does job loss insurance cover?

- How long does job loss insurance provide coverage?

- What do you need to claim job loss insurance?

- Job loss insurance vs. Employment Insurance (EI)

- Job loss insurance vs. disability insurance

- How to buy job loss insurance in Canada

- Frequently Asked Questions

Losing your job can make it difficult to keep up with mortgage, loan, or other financial obligations. Job loss insurance is a type of creditor insurance designed to help cover eligible debt payments if you lose your job through no fault of your own.

Job loss insurance helps you cover the financial gap while you search for a new job or source of income. Unlike regular policies, it is usually offered as an add-on or rider by creditors and lenders.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What is job loss insurance in Canada?

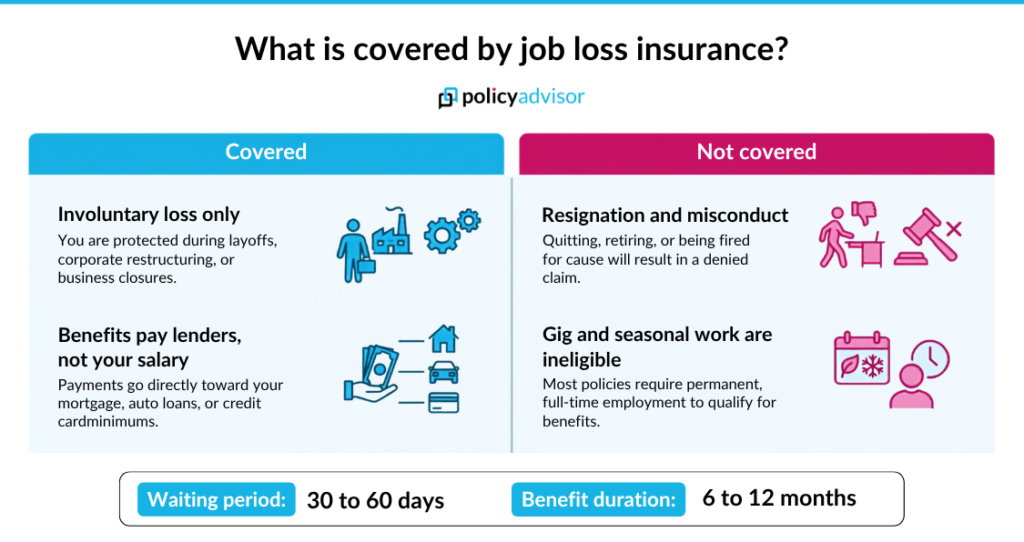

Job loss insurance is an add-on insurance product that helps cover certain debt payments if you lose your job for involuntary reasons, such as layoffs, company restructuring, or business closure. Instead of replacing your salary, it pays some or all of your eligible monthly loan payments and debts for a limited period while you are seeking new employment.

Unlike traditional insurance policies, it is not sold as a standalone product. Job loss insurance is usually sold as an add-on or rider to financial products, and the benefits are typically directly paid to the lender. For example, if you have an outstanding debt on your credit card, the insurer will pay the minimum due directly to the bank.

Job loss insurance in Canada: At a glance

| Feature | Details |

| Purpose | Helps cover eligible debt payments after involuntary job loss |

| Best suited for | Homeowners and borrowers with significant monthly debt obligations |

| Who offers it? | Banks, credit unions, mortgage lenders, and some insurance providers |

| What it covers | Mortgage payments, loan payments, credit cards, and other eligible debts |

| Benefit period | Typically 6–12 months |

| Waiting period | Usually 30–60 days before benefits begin |

| Income replacement? | No. Benefits are paid toward eligible debts directly to the lender, not your salary |

| If you lost your job tomorrow, would your savings cover all of your bills?

According to Statistics Canada, the average savings rate of household income is 5.1%. That means most Canadians are only saving a tiny fraction of their salary. So, chances are, your savings wouldn’t be enough to cover your bills. But even if it could, would you really want to dip into your savings just to make ends meet? |

Types of job loss insurance in Canada

While there is no specific type of job loss insurance, benefits are usually tied to the financial product you purchase that offers this rider. Many institutions also call it Creditor Insurance, payment protection insurance (PPI), or credit protection, allowing beneficiaries to continue paying off their debts for a duration.

Here’s an overview of the common types of financial offerings that may provide job loss insurance as a creditor protection rider or add-on:

- Mortgages

- Personal loans

- Home equity lines of credit (HELOCs)

- Auto loans

- Credit cards

Who is eligible for job loss insurance in Canada?

Eligibility for job loss insurance varies by insurer and lender, but most policies are designed for Canadian individuals in stable, full-time employment. Additionally, some policies might require you to work the minimum hours or complete additional probationary periods before they come into force.

Here’s a quick overview of the general eligibility requirements for job loss insurance in Canada:

| Requirement | Details |

| Age requirement | Must meet the insurer’s minimum and maximum entry age requirements. |

| Employment status | Must be a permanent, full-time, or eligible part-time employee working for an employer. |

| Involuntary job loss | Must lose your job through no fault of your own, such as a permanent layoff, company closure, or workforce reduction. |

| Minimum employment period | Some insurers require you to have been continuously employed for a minimum period before becoming unemployed. |

| Active employment | You must usually be actively working on the date your coverage begins |

| Waiting period | Your policy must have been in force long enough to satisfy any waiting or qualification period before benefits become payable. |

| Proof of unemployment | Some policies require documentation such as a Record of Employment (ROE), termination letter, or other proof that your job ended involuntarily. |

| Receiving or seeking employment | Some policies require you to register for Employment Insurance (EI) or actively seek new employment while receiving benefits |

Who is not eligible for job loss insurance in Canada?

While job loss insurance applies to employees with ongoing employment, individuals on fixed-term contracts, seasonal workers, or temporary workers may not be eligible for this add-on.

Pros and cons of job loss insurance

How does job loss insurance work?

Job loss insurance in Canada works similarly to most other insurance policies, where it is triggered by certain unforeseen events. Once you purchase the policy after meeting eligibility requirements, benefits are activated if you lose your job involuntarily.

After you lose your job, most insurers will have a waiting period after which your benefit payments begin. Your benefits and payout continue until you return to work or you reach the policy’s maximum period. Additionally, coverage may end if your debts are paid off within the benefit period.

What does job loss insurance cover?

Job loss insurance in Canada offers financial protection if you are out of a job through no fault of your own. Depending on the financial product that offers this add-on, benefits may include some or all of the following:

Here’s an overview of benefits typically offered by job loss insurance in Canada:

| Coverage | What it covers |

| Mortgage payments | Covers some or all of your monthly mortgage payments for a specified period |

| Loan repayments | Covers eligible personal loan, line of credit, or auto loan payments, depending on the policy |

| Credit card payments | Pays the minimum monthly payment on eligible insured credit cards |

What is not covered by job loss insurance in Canada

While job loss insurance in Canada offers financial benefits to individuals who have involuntarily lost their jobs, there are certain restrictions regarding resignation or the grounds for dismissal.

Here’s an overview of common situations not covered by job loss insurance in Canada:

| Exclusion | Reason |

| Voluntary resignation | Coverage generally applies only to involuntary job loss |

| Dismissal for misconduct or cause | Claims are typically denied if employment ends due to misconduct |

| Self-employment or independent contractors | Many policies cover only salaried or permanent employees |

| Seasonal or temporary employment | Coverage is often limited to permanent employment |

| Known or anticipated layoffs | Job losses that were announced before purchasing coverage are generally excluded |

| Unemployment during the waiting period | Most policies have a waiting period before benefits become available |

| Retirement | Voluntary retirement is not considered an insured event |

How long does job loss insurance provide coverage?

Since job loss insurance is intended as temporary financial protection, benefits are limited. Most job loss insurance policies in Canada pay benefits for up to 6 months per claim. However, some insurers may provide longer lifetime maximums for up to 12 months.

However, some insurers may provide longer lifetime maximums of up to 12 months. Also note that many job loss insurance policies in Canada have a waiting period before benefits begin, typically 30 to 60 days, depending on your policy and benefits.

What do you need to claim job loss insurance?

To make a job loss insurance claim, you will need to provide documents proving that you have lost your job involuntarily and meet your policy’s eligibility requirements. While exact documentation varies by insurer, most providers will ask for evidence of your employment status and unemployment benefits before approving a claim.

Here are some documents that you are typically required to submit when applying for job loss insurance:

- Record of Employment (ROE) confirming your employment has ended

- Proof of Employment Insurance (EI) benefits or, if applicable, proof of strike pay (such as a union letter)

- Proof of unemployment benefits or a Service Canada letter detailing your severance package

- Completed claim forms and any additional documentation requested by your insurance provider

Your Record of Employment (ROE) is one of the most important documents for a claim and can typically be accessed through your Service Canada account if your employer has submitted it electronically.

Employment requirements for a job loss insurance claim

In addition to providing the required documents, you will also need to meet your insurer’s employment eligibility criteria. While requirements vary between providers, most job loss insurance policies are designed for individuals with stable, ongoing employment.

Common employment requirements include:

- Working at least 20 hours per week in a permanent position

- Having been employed for at least nine months before making a claim

- Maintaining continuous employment with the same employer for at least one year

- Losing your job involuntarily, such as through a layoff, business closure, or company restructuring

Eligibility requirements vary by insurer. It is recommended to check your policy wording to confirm the exact list.

Job loss insurance vs. Employment Insurance (EI)

Many Canadians wonder if they need job loss insurance if they are covered under Employment Insurance (EI), which is a federal government program funded through payroll contributions.

While EI is a government-run income replacement program, job loss insurance is a private insurance product designed to help cover specific financial obligations, such as mortgage or loan payments.

Here is a comparison of the key differences and benefits of job loss insurance and Employment Insurance (EI) in Canada:

| Feature | Job loss insurance | Employment Insurance (EI) |

| Provider | Private insurance company or lender | Government of Canada |

| Purpose | Helps cover insured financial obligations, such as mortgage, loan, or credit card payments | Replaces part of your employment income while you are unemployed |

| Eligibility | Depends on the insurance policy and underwriting requirements | Must meet EI eligibility criteria, including sufficient insurable hours and involuntary job loss |

| Benefits | Monthly payments toward eligible insured debts or a fixed monthly benefit | Up to 55% of average weekly insurable earnings, up to the annual maximum benefit |

| Benefit period | Typically up to 6 months per claim (varies by insurer) | Usually 14–45 weeks, depending on your insurable hours and regional unemployment rate |

| Waiting period | Varies by policy (commonly 30–60 days before benefits begin) | One-week waiting period before benefits are paid |

| Premiums | Paid by the policyholder | Premiums are deducted from employees’ paycheques and paid by employers |

Should you choose Employment Insurance or job loss insurance in Canada?

While Employment Insurance (EI) is the primary source of income support for eligible Canadians who lose their jobs through no fault of their own, it may not fully replace your income or cover all of your financial obligations.

Meanwhile, job loss insurance can help you continue making mortgage, loan, or credit card payments while you are unemployed. It is also worth noting that many employers have a mandatory enrollment in the EI program, making job loss insurance an optional add-on.

Can you receive both Employment Insurance and job loss insurance in Canada?

Yes, in many cases, you may qualify for Employment Insurance while also receiving benefits under a private job loss insurance policy, provided you meet the eligibility requirements of both programs. Since they serve different purposes, receiving one does not disqualify you from the other.

Job loss insurance vs. disability insurance

Canadian employees often confuse unemployment protection with disability insurance, but they protect against very different risks. While job loss insurance deals with debts and mortgages, disability insurance provides income replacement if an illness or injury prevents you from working.

Similar to Employment Insurance, you can have disability insurance and job loss insurance at the same time. This combination is effective for protecting your financial liabilities while providing supplemental income to manage living expenses.

How to buy job loss insurance in Canada

Job loss insurance is usually offered when you apply for a mortgage, personal loan, line of credit, auto loan, or credit card. Since it is often sold as creditor insurance, the add-on is designed to protect a specific debt rather than provide general income replacement.

It is usually offered by creditors such as banks or insurers when you purchase a product. It is recommended to discuss premiums, benefit limits, waiting periods, and exclusions with your lender.

Is job loss insurance worth it in Canada?

The need for job loss insurance in Canada depends solely on your financial situation and existing insurance policies or alternative methods of funding. If you have 3–6 months of living expenses saved or your Employment Insurance payout is enough to sustain your daily costs, it may be advisable to skip this add-on.

However, if you have incurred significant debt through the purchase of property or other assets and do not have substantial emergency savings, it may be advisable to keep job loss insurance as a safety net to prevent defaulting on repayments or hurting your credit score.

Frequently Asked Questions

What does job loss insurance cover?

Job loss insurance generally covers eligible debt payments after involuntary unemployment, including mortgages, personal loans, auto loans, and some credit card or line of credit payments.

Does job loss insurance cover layoffs?

Yes, most policies cover involuntary job loss due to layoffs, company restructuring, employer bankruptcy, or business closures as long as you meet the eligibility requirements.

Does job loss insurance cover voluntary resignation?

No. If you resign from your job voluntarily, job loss insurance typically will not pay benefits since the unemployment was the result of your actions.

How long do job loss insurance benefits last?

Most policies provide benefits for six to twelve months. However, the exact duration depends on your insurer, lender, and policy terms.

Does job loss insurance affect my credit score?

No, purchasing job loss insurance does not affect your credit score. In fact, it protects your credit score by ensuring you can pay the minimum due without defaulting.

Job loss insurance is an optional type of creditor insurance that helps cover eligible debt payments, such as mortgages, personal loans, and credit cards, if you lose your job involuntarily. This guide explains how job loss insurance works in Canada, what it covers, common exclusions, costs, eligibility requirements, alternatives, and how to decide if it is the right financial protection for you.