- Top providers of critical illness insurance in Canada for 2026 include Canada Life, Desjardins, iA Financial, Sun Life, and BMO

- Critical Insurance is a living benefit insurance policy. It typically pays a tax-free lump sum if you develop a specified illness, are diagnosed with a covered illness or medical condition, as defined in the policy

- Choosing a plan requires reviewing covered illnesses, coverage amount, payment terms, and riders

A serious illness can disrupt both your health and your finances. Critical illness insurance in Canada pays a tax-free lump sum after a covered diagnosis, helping cover medical costs, household expenses, and lost income without dipping into savings.

The risk is significant. About one in two Canadians will develop cancer in their lifetime. Each year, nearly 70,000 have heart attacks and more than 62,000 experience strokes.

Coverage varies by insurer. Differences in illness definitions, payouts, premiums, and policy flexibility can affect how much support you receive when you need it most. Based on our review of leading critical illness insurance companies in Canada, five providers stand out for 2026 for their strong coverage, clear payouts, competitive pricing, and flexible policy options. The remaining insurers are covered later in our full comparison.

Top 5 critical illness insurance companies in Canada (2026)

- Canada Life: Best for comprehensive and customizable coverage

- Desjardins: Best for extensive coverage

- iA Financial: Best for flexibility

- Sun Life: Best for comprehensive features

- Assumption Life: Best for simple coverage

What is critical illness insurance?

Critical illness insurance is designed to provide financial support if you are diagnosed with a serious illness such as cancer, heart attack, or stroke while you are still living. As a living benefit policy, it pays a one-time, tax-free lump sum directly to you after a covered diagnosis, allowing you to focus on recovery without added financial stress.

You can use the payout in any way you choose. Common uses include replacing lost income, paying for treatment or recovery costs not covered by provincial health plans, reducing debt, or managing everyday household expenses.

Critical illness insurance claims generally fall into two main categories.

- A full claim is paid when you are diagnosed with a major covered illness, such as cancer, heart attack, or stroke, based on the definitions in your policy. Once the claim is approved, the insurer pays the full benefit amount directly to you

- Many policies also offer partial or early-stage claims for less severe or early-detected conditions, such as early-stage cancers or certain medical procedures. These claims provide a portion of the insured amount, while keeping the remaining coverage available for future claims

What does CI insurance cover?

Critical illness insurance typically covers serious medical conditions such as:

- Cancer

- Heart attack

- Stroke

Many policies may also include coverage for additional conditions, subject to strict medical definitions, such as:

- Dementia and Alzheimer’s disease

- Parkinson’s disease

- Kidney failure

- Major organ transplant

- Blindness, coma, and deafness

Some policies may include limited or partial benefits for selecting early-stage or less severe conditions. Coverage for conditions such as HIV, where available, is highly restricted and definition-based, and is not included in all policies.

How much does Critical Illness Insurance cost?

Get instant quotes from Canada's top critical illness insurance providers and find the perfect coverage for your family.

Powered by

![]()

What are the best critical illness insurance companies in Canada?

The best critical illness insurance companies in Canada combine broad coverage, competitive pricing, and reliable payout structures. Coverage limits, payout structures, and policy features vary significantly between insurers.

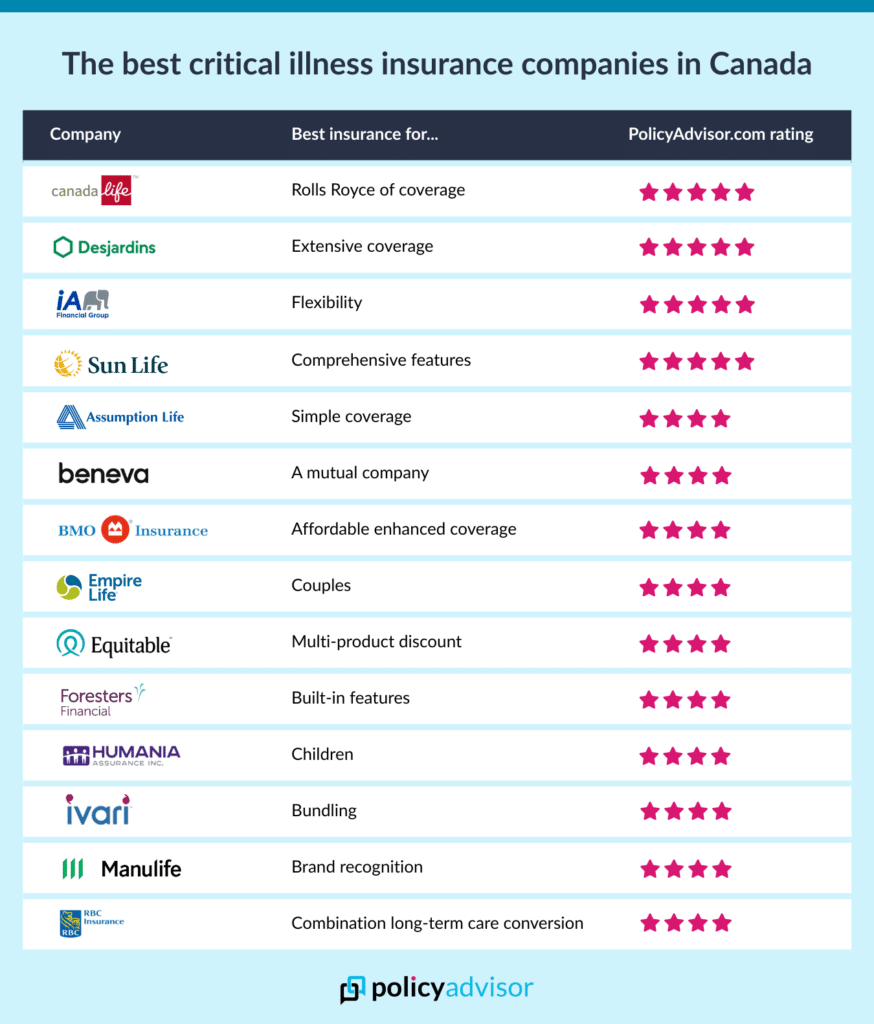

Best 14 critical illness insurance companies in Canada (2026)

- Canada Life: Best for comprehensive and customizable coverage

- Desjardins: Best for extensive coverage

- iA Financial: Best for flexibility

- Sun Life: Best for comprehensive features

- Assumption Life: Best for simple coverage

- Beneva: Best for a mutual company

- BMO Insurance: Most affordable enhanced coverage

- Empire Life: Best for couples

- Equitable Life: Best for multi-product discount

- Foresters Financial: Best for built-in benefits

- Humania: Best for children

- Ivari: Best for bundling

- Manulife: Best for brand recognition

- RBC Insurance: Best for combination long-term care conversion

Let’s take a closer look at each of these top insurers, their unique features, and what makes them stand out in 2026.

1. Canada Life: Best for comprehensive and customizable coverage

8 partial conditions

20-year term

up to age 75

PolicyAdvisor Rating

We give Canada Life a 5/5 because its LifeAdvance critical illness insurance offers one of the most comprehensive and customizable CI product suites in Canada. LifeAdvance covers 25 full payout CI, with partial payouts available for 8 additional conditions. Coverage amounts go up to $3 million, among the highest in the market.

Policyholders can choose flexible payment options, including 10-year term, 20-year term, term to age 75, or permanent coverage with 15-pay, 20-pay, or pay-to-100 structures. Optional riders may include children’s coverage and limited second-event benefits, subject to policy terms and availability at issue. This plan works well for Canadians who want flexible, long‑term protection.

Why choose Canada Life

- High maximum coverage supports estate planning and business protection

- Broad rider availability allows highly customized policy design

- Children’s coverage adds family-focused flexibility

Unique selling point (USP): Canada Life’s LifeAdvance plan delivers highly customizable critical illness protection with high limits, permanent coverage options, and advanced riders.

2. Desjardins: Best for extensive coverage

16 partial conditions

20-year term

up to age 65

up to age 75

PolicyAdvisor Rating

We give Desjardins a 5/5 because its Health Priorities Critical Illness Insurance offers one of the broadest ranges of covered conditions in the Canadian market. The plan covers 26 life-threatening illnesses with full payouts and provides partial payouts for 16 additional conditions, more than most Canadian insurers. Survival periods apply and vary by condition, with longer waiting periods for certain neurological illnesses.

Coverage amounts go up to $3 million. Payment options include 10‑year term, 20‑year term, term to age 65, and term to age 75. The plan also includes children’s coverage. Partial payouts count against the total benefit. This plan is ideal for Canadians who want the broadest condition coverage.

Why choose Desjardins

- Widest range of covered conditions in Canada

- Digital delivery simplifies claims setup

- Ideal for clients seeking maximum illness coverage breadth

Unique selling point (USP): Desjardins’ Health Priorities plan offers the widest range of covered critical and partial conditions in Canada, making it ideal for Canadians who want maximum illness coverage breadth.

3. iA (Industrial Alliance): Best for flexibility

5 childhood illnesses

7 partial payouts for non-life-threatening conditions

12-year term

25-year term

up to age 75

up to age 100

PolicyAdvisor Rating

We give iA (Industrial Alliance) a 5/5 because its Transition plan provides broad coverage with unmatched flexibility. The plan covers 25 major critical illnesses and 5 childhood illnesses. It also offers partial payouts for 7 conditions. Coverage amounts go up to $2.5 million. Payment options include 10‑year term, 12‑year term, 25‑year term, term to age 75, and term to age 100. Optional riders include guaranteed insurability and mortgage‑reducing benefits. The reducing option gradually decreases the benefit payment in the early years (down to 50%), by design, making it suitable for mortgage or short-term protection needs. This plan fits clients who want flexible and tailored coverage.

Why choose iA

- Mortgage-reducing and guaranteed insurability riders enhance practical value

- Multiple lives can be covered under one policy

- Online management provides fast, convenient access

Unique selling point (USP): iA stands out for its highly flexible critical illness coverage, with the widest range of term options, customizable riders, and mortgage-reducing benefits for tailored protection.

4. Sun Life: Best for comprehensive features

8 partial conditions

up to age 75

permanent coverage

PolicyAdvisor Rating

We give Sun Life a 4/5 because it offers some of the most comprehensive critical illness coverage in Canada, backed by a long-established insurer with strong claims-paying ability.

The plan covers 26 full payout conditions and partial payouts for 8 conditions. Coverage amounts go up to $2.5 million. Payment options include 10‑year term, term to age 75, and permanent coverage. The plan allows up to four partial claims, one per eligible condition, subject to policy definitions. The application process remains largely paper-based and advisor-assisted, which may be slower than fully digital competitors.

Why choose Sun Life

- Allows multiple partial claims for increased usability

- Long-term care conversion adds future planning flexibility

- Children’s illnesses included for family protection

Unique selling point (USP): Sun Life stands out for its extensive condition coverage and long-term flexibility, including permanent CI and long-term care conversion options.

5. Assumption Life: Best for simple coverage

20-year term

PolicyAdvisor Rating

We give Assumption Life a 4/5 because its Critical Protection plan focuses on straightforward, essential critical illness coverage. With 16 covered conditions, it is designed for Canadians who want basic protection without the complexity or cost of more feature-rich plans.

The plan offers value through simplified underwriting, optional return-of-premium riders, and a fully digital application experience. Medical exams are not automatically required for all coverage amounts, making approval faster and more accessible for many applicants.

Why choose Assumption Life

- Simple, straightforward coverage with fast electronic approval

- Optional return-of-premium riders add flexibility

- Minimal medical exam requirements for easier access

Unique selling point (USP): Assumption Life offers straightforward critical illness coverage with fast digital approval, making it ideal for Canadians seeking basic protection without complexity.

6. Beneva: Best for a mutual company

4 partial conditions

20-year term

up to age 75

up to age 100

PolicyAdvisor Rating

We give Beneva a 4/5 because it combines comprehensive critical illness coverage with a mutual company structure. Policyholders become members of a mutualist organization, giving them a voice in how the company is run; an appealing feature for Canadians who value community involvement and corporate responsibility.

Beneva offers coverage for up to 25 critical conditions with maximum benefits of $2 million. Partial payouts are available for 4 non-life-threatening conditions, typically paid at 10% of the policy amount up to $50,000, generally payable once per policy. While partial coverage is more limited than some competitors, the plan includes children’s coverage and permanent policy options.

Why choose Beneva

- Mutual company structure gives policyholders a voice

- Children’s coverage is included for family protection

- Digital delivery improves accessibility

Unique selling point (USP): Beneva stands out as a mutual insurer, offering solid critical illness coverage while allowing policyholders to participate in a member-owned organization.

7. BMO: Best for affordable enhanced coverage

7 early-stage conditions

20-year term

up to age 75

up to age 100

PolicyAdvisor Rating

We give BMO a 4/5 because its Living Benefit Critical Illness Insurance covers 25 life-threatening illnesses plus partial payouts for 7 early-stage conditions. Coverage ranges from $25,000 to $2 million, with flexible terms of 10 years, 20 years, or to age 75 or 100.

Unlike standard critical illness plans, BMO’s Early Discovery Benefit provides a portion of the benefit for early-stage diagnoses. This helps clients manage treatment costs right away, rather than waiting for a major claim. It’s ideal for families with mortgages, young children, or business owners who can’t afford income interruptions.

Why choose BMO

- Early-stage payouts reduce financial stress and improve usability

- Flexible terms accommodate different life stages

- Affordable enhanced coverage backed by a major Canadian insurer

Unique selling point (USP): Early-stage partial payouts plus broad coverage ensure Canadians receive meaningful financial support when a serious illness strikes, not just at its most severe stage.

8. Empire Life: Best for couples

6 partial conditions

20-year term

up to age 75

up to age 100

PolicyAdvisor Rating

We give Empire Life a 4/5 because it offers a well-rounded critical illness insurance plan with strong coverage and a unique multi-life option. Coverage amounts go up to $2 million, with full payouts for 25 critical illnesses and partial payouts for 6 additional conditions, each up to $50,000.

Empire Life stands out for couples by allowing two lives to be insured under a single policy at a discounted rate. While children’s coverage and limited-pay options are not available, the plan remains a solid choice for adults seeking comprehensive protection with cost savings for partners.

Why choose Empire Life

- Multi-life option provides discounted coverage for couples

- Partial payouts enhance usability for less severe conditions

- Digital policy delivery improves convenience

Unique selling point (USP): Empire Life’s multi-life critical illness policy offers couples discounted coverage under one plan, combining affordability with comprehensive protection.

9. Equitable Life: Best for multi-product discounts

20-year-term

payup to age 75

up to age 100

PolicyAdvisor Rating

We give Equitable Life a 4/5 because its critical illness insurance offers solid coverage paired with valuable multi-product discounts. When bundled with other Equitable policies, such as life insurance, policyholders can reduce overall premiums while maintaining comprehensive protection.

The plan covers 26 critical illnesses, includes protection for 5 childhood illnesses, and offers coverage for loss of independent existence. Coverage amounts go up to $2 million, with flexible term options including Term-to-100 and a limited-pay structure. While partial benefits are limited to a single payout, and second event coverage is not available, the discount potential makes this plan attractive for bundled insurance buyers.

Why choose Equitable Life

- Multi-product discounts reduce overall insurance costs

- Built-in children’s coverage adds family protection

- Term-to-100 and limited-pay options allow flexible planning

Unique selling point (USP): Equitable Life stands out for its multi-product discounts, making it a strong choice for Canadians bundling critical illness coverage with other insurance needs.

10. Foresters Financial: Best for built-in benefits

Live Well Plus

8 partial conditions

20-year term

up to age 80

PolicyAdvisor Rating

We give Foresters a 4/5 because its refreshed Live Well and Live Well Plus critical illness plans include several built-in features that add value without requiring extra riders. Return-of-premium is included as standard, and policyholders also gain access to Foresters’ community benefits.

Coverage amounts go up to $2 million for enhanced plans, with partial payouts available for 8 conditions. Partial claims typically pay 15% of the policy amount, up to $50,000, and can be claimed twice, though they reduce the final benefit. The plan also offers a unique Term-to-80 option, which is uncommon in the Canadian market.

Why choose Foresters

- Built-in return-of-premium feature adds value without extra riders

- Unique term-to-80 option extends coverage into later life

- Community and member benefits included

Unique selling point (USP): Foresters stands out for its built-in benefits, combining return-of-premium features, community perks, and partial payouts in a single critical illness policy.

11. Humania: Best for children

15-year term

20-year term

25-year term

30-year term

up to age 75

PolicyAdvisor Rating

We give Humania a 4/5 because it offers the most comprehensive critical illness coverage for children in Canada. Its Children360 plan covers 37 conditions, including several illnesses that are specific to childhood, and includes a compassionate allowance for parents in the event of a child’s death.

For adults, Humania offers separate critical illness plans covering 25 conditions, with limited partial payouts for select non-life-threatening illnesses. While partial benefits are more restricted than many competitors, the wide range of term options and child-focused design make Humania a strong choice for families prioritizing children’s coverage.

Why choose Humania

- Market-leading coverage for childhood conditions

- Compassionate allowance supports parents during difficult events

- Wide range of term options allows tailored family planning

Unique selling point (USP): Humania’s Children360 plan delivers the most comprehensive critical illness protection for children, including coverage for child-specific conditions and compassionate benefits for parents.

12. ivari: Best for bundling as a rider

4 partial conditions

20-year term

up to age 65

PolicyAdvisor Rating

We give ivari a 4/5 because its critical illness insurance is designed to reward bundling. Policyholders can add up to $2 million in critical illness coverage as a rider to an existing ivari life insurance policy and save up to 15% on premiums.

The plan covers 25 critical illnesses with partial payouts for 4 non-life-threatening conditions (up to $50,000). Optional children’s coverage can be added for an additional cost. While coverage options are limited to term policies and lack permanent or limited-pay structures, ivari offers meaningful savings for clients consolidating insurance with one provider.

Why choose ivari

- Bundling with life insurance reduces overall premiums

- Optional children’s coverage for added family protection

- Simple, streamlined policy structure with digital access

Unique selling point (USP): ivari’s critical illness insurance rewards brand loyalty by offering meaningful savings when bundled with life insurance coverage.

13. Manulife: Best for brand reliability and balanced coverage

6 partial conditions

20-year term

up to age 65

up to age 75

permanent coverage

PolicyAdvisor Rating

We give Manulife a 4/5 rating for its well-rounded critical illness insurance offering backed by one of Canada’s most trusted insurers. Lifecheque provides coverage up to $2 million, with 10- and 20-year terms, term-to-age options, and permanent coverage, making it suitable for both short- and long-term financial planning.

While the plan includes partial payouts for six non-life-threatening conditions and optional riders, return-of-premium features are expensive and second event coverage is not available. Still, Manulife remains a strong choice for Canadians prioritizing stability, flexibility, and comprehensive protection.

Why choose Manulife

- Trusted, long-established Canadian insurer

- Flexible term and permanent options for short- and long-term planning

- Optional riders provide coverage for children and loss of independence

Unique selling point (USP): Manulife stands out for its combination of strong brand credibility and flexible coverage options, making it a dependable choice for Canadians seeking long-term critical illness protection.

14. RBC: Best for long-term care conversion

7 partial payout

20-year term

up to age 65

up to age 75

permanent coverage

PolicyAdvisor Rating

We give RBC a 4/5 because it is the only major Canadian insurer offering a long-term care conversion option with its critical illness insurance. Policyholders can convert their critical illness coverage into long-term care benefits later in life without additional proof of insurability, making it a strong option for long-term planning.

RBC provides coverage for 25 critical illnesses, with partial payouts for 7 non-life-threatening conditions, typically paid once during the policy’s lifetime. While children’s critical illness coverage is limited and may require riders, RBC does not offer permanent CI policies or return-of-premium options.

Why choose RBC

- Long-term care conversion without underwriting

- Partial payouts provide early financial support

- Backed by a large, established Canadian insurer

Unique selling point (USP): RBC’s critical illness insurance stands out for its long-term care conversion option, allowing Canadians to transition coverage as care needs change later in life.

Methodology: How we ranked critical illness insurance companies

We ranked critical illness insurance companies based on detailed research into the most important factors for Canadian buyers. These include:

- Conditions covered

- Partial conditions covered

- Waiting periods

- Premium rates

- Application process

- Online access

- Financial strength ratings

Our team of licensed insurance advisors assessed each policy carefully. This allowed us to identify which insurer excels in which area and recommend the best critical illness insurance options for different needs.

How much does CI cost in Canada

Critical illness insurance rates in Canada depend on age, gender, smoking status, coverage amount, and province.

The table below shows illustrative monthly premiums for healthy non-smokers, broken down by age and gender.

| Age | Male | Female |

| 30 years | $23.94 | $23.31 |

| 40 years | $35.55 | $37.44 |

| 50 years | $77.22 | $68.49 |

* Illustrative premiums for healthy non-smokers. Actual rates vary by insurer, coverage amount, and health profile.

The table below shows illustrative monthly premiums for smokers, broken down by age and gender.

| Age | Male | Female |

| 30 years | $30.51 | $25.92 |

| 40 years | $62.10 | $59.76 |

| 50 years | $176.40 | $132.48 |

*Illustrative monthly premiums for $100,000 of 10-year term critical illness coverage with no return of premium. Rates assume smoker status and may vary by insurer, health, and underwriting.

Note: Rates differ by province, health history, and optional riders such as return-of-premium or partial benefit coverage.

Who should consider critical illness insurance?

Critical illness insurance is designed for people whose finances could be significantly affected by a serious illness. It provides financial stability at a time when income and expenses may both be under pressure, allowing you to focus on recovery with greater peace of mind.

This coverage is especially relevant for:

- Individuals with financial dependents, such as children or aging parents

- Homeowners carrying mortgage obligations

- Self-employed workers or professionals with variable income

- People with limited savings or emergency reserves

- Those with a family history of major illnesses

- Anyone relying mainly on basic or limited workplace health benefits

- For these groups, critical illness insurance can act as a financial buffer, helping protect both personal finances and long-term plans during a serious health event.

What to consider when buying critical illness insurance in Canada

If critical illness insurance still makes sense for your situation, these are the factors that matter most when choosing a policy:

- Illnesses covered: Review the specific illnesses and medical definitions in each policy. Most plans include cancer, heart attack, and stroke. Some policies also offer partial or early-stage benefits for certain conditions, subject to strict definitions

- Coverage amount: Choose an amount based on expected medical costs not covered by provincial health insurance, income disruption, debt obligations, and household expenses during recovery

- Payment terms: Depending on the insurer, you may be able to choose limited-pay options (such as 10- or 20-pay) or ongoing premiums over the policy term

- Additional benefits or riders: Optional riders, such as return-of-premium, may refund some or all premiums under specific conditions, but they increase policy cost and vary by insurer

How to get the best CI quotes in Canada

Get your best critical illness insurance quote in three simple steps:

- Share your age, basic health details, and coverage goals

- Compare critical illness plans and features side by side from leading Canadian insurers

- Confirm your rate with support from a licensed PolicyAdvisor advisor at no cost

To begin, you only need your age, general health history, desired coverage amount, and an estimate of how much financial protection you want if a serious illness occurs.

After you choose a plan, PolicyAdvisor’s licensed insurance experts continue to support you by explaining your coverage clearly and helping you make informed decisions with confidence.

Frequently asked questions

Is critical illness insurance worth it in Canada?

Critical illness (CI) insurance is worth considering if a serious diagnosis would disrupt your income or create out‑of‑pocket costs. CI pays a tax‑free lump sum you can use for anything. If you have dependants, debt, or limited savings, talk to an advisor about a right‑sized amount and term for your budget.

Which three illnesses are covered under most critical illness policies?

Cancer, heart attack, and stroke are covered under most critical illness policies in Canada.

What is a good amount for critical illness insurance?

The right amount of critical illness insurance in Canada depends on your lifestyle, family needs, savings, medical expenses not covered by provincial health care, and the income required to support you and your family during your illness.

What is the difference between critical illness insurance and regular health insurance?

Critical illness insurance provides a one-time, tax-free lump sum payment upon diagnosis of specific conditions, such as cancer, heart attack, and stroke. Regular health insurance, in contrast, covers a broad range of conditions and reimburses you for the actual treatment costs after you submit bills and related documentation.

Check our review of the top 14 critical illness insurance companies in Canada for 2026. We compared coverage, payout rules, payment terms, and policy flexibility. Canada Life, Desjardins, and iA Financial rank highest for coverage depth and customization. Other providers stand out for affordability, children’s coverage, or long-term care options.