There are a lot of different products on the market to insure your new home. One of those options is mortgage protection insurance through an insurance company.

We created a list of the 6 Best Mortgage Insurance Companies in Canada based on our years of expertise and research. These ratings and reviews are based on factors like type of policy, range of products, financial strength, and more.

We also give our reviews of some of the types of mortgage protection we don’t recommend. And, we show you why a traditional life insurance policy is the best coverage for homeowners. (Click here to skip to that part now)

Top mortgage protection insurance in Canada

Our team of experts at PolicyAdvisor.com has picked 6 companies as having the best mortgage protection in Canada. We’ve ranked them based on different categories based on their strengths and weaknesses.

We have worked with the largest insurance companies for years, giving us insight into the best of what Canadian providers have to offer. This lets us review the country’s best insurance for mortgage protection to help you know which one you should pick.

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

Canada’s Best Mortgage Protection Insurance Companies

- Assumption Life: Best for simplified issue

- Beneva: Best for combination coverage

- Canada Life: Best for financial strength

- Empire Life: Best for personalization

- Industrial Alliance (iA): Best for flexibility

- UV: Best for riders

Compare the best mortgage protection insurance companies

Here are Canada’s best mortgage insurance companies that offer diverse features. If you’re looking for the best mortgage protection plan, these are some of the companies to consider:

| Insurance Provider | Best for | What we like | Maximum Coverage |

| Assumption Life | Simplified issue | FlexTerm that lets you choose your policy term and quick electronic applications in less than 15 minutes | $10,000,000 |

| Beneva | Combination coverage | Offers term life insurance, disability and critical illness coverage | $10,000,000 |

| Canada Life | Financial strength | Wide range of policy options, strong financial stability | $20,000,000 |

| Empire Life | Personalization | Solution 20 rider that adds to your critical illness coverage and protects against 23 covered illnesses | $10,000,000 |

| Industrial Alliance (iA) | Flexibility | Pick-a-term lets you choose your term between 10 and 40 years | $10,000,000 |

| UV Insurance | Riders | MyUniverse portal lets you apply online and choose between different riders | $500,000+ |

Reviews of top mortgage protection insurance companies in Canada

1. Assumption Life Mortgage Protection Insurance – Best for simplified issue

If you want to quickly get coverage for your mortgage without having to take a medical exam, then you should look at Assumption Life’s Flexterm plan. This is called simplified insurance. You can get approved much faster, although at a higher cost.

Assumption offers terms ranging from 10 to 35 years, as well as a decreasing term option that you can match with your mortgage.

They also have regular plans if you don’t mind doing a health assessment. And, getting a fully underwritten plan gives you far more options for premium rates, riders, and benefits:

- Critical Illness Rider covers 16 illnesses, which is more than many of Assumption’s competitors cover

- Disability Income Rider gives extra coverage on top of regular income replacement in the event of disability

- Extreme Disability Benefit is included at no additional cost — very rare in Canada!

Assumption Life Mortgage Protection Insurance Pros and Cons

| Pros | Cons |

|---|---|

| A built-in Extreme Disability Benefit is unique in the industry | Can be expensive |

| Multiple term coverage options | Long underwriting process |

| Simplified, non-medical issue options | High policy fees and rider fees |

| Both level and decreasing options — decreasing term option can be used to match your mortgage | Additional insurance options (riders and benefits) not available with simplified option |

| Online access to account | |

| Digital e-policy | |

| Ability to exchange shorter term policies into longer term policies | |

| Several optional riders, including term life and children’s life | |

| Critical illness rider covers 16 illnesses |

2. Beneva Mortgage Protection Insurance – Best for combination coverage

Beneva’s Term Plus is a good choice for homeowners seeking an all-in-one solution for mortgage protection. It’s a multi-purpose plan that you can put to good use for several things. And, the company gives you some pretty tempting options to help maximize your coverage.

You can pick a decreasing term to match your mortgage, and get optional add-on riders at a small extra cost to create a plan with multiple types of coverage at a great price — all in one place.

Plus, Beneva has a rare Extreme Disability Benefit included for free in all of its plans. Most other companies only give you these kinds of insurance coverage if you pay an additional cost.

Add that to their riders for critical illness and disability insurance protection, and you have an easy way to tick all of your insurance boxes in one go!

Beneva Mortgage Protection Insurance Pros and Cons

| Pros | Cons |

|---|---|

| A built-in Extreme Disability Benefit is unique in the industry | Longer turnaround times for policy approval |

| Optional critical illness and disability riders make for comprehensive mortgage insurance coverage | Critical illness rider only 10 or 20-year term and only covers 3 conditions |

| Critical illness rider includes psychological assistance and second medical opinion | |

| Several optional riders including accidental death & dismemberment and child rider | |

| Preferred rates available starting at $1,000,000 for those in excellent health condition | |

| Digital e-policy |

3. Canada Life Mortgage Protection Insurance – Best for financial strength

Canada Life is an excellent choice if you want to be insured with a company that has financial stability. According to our records, they’re one of the largest life insurance companies in all of Canada. You can feel secure getting coverage with them and knowing they’re probably not going anywhere anytime soon.

They also have a Business Growth Protection rider that’s particularly useful for business owners. It lets them buy more insurance coverage when their share of the business grows. So, you can get easier access to more insurance while protecting your mortgage at the same time.

You can choose any term length from 5 to 50 years with Canada Life. And, they have optional add-on riders like child’s term life insurance to let you create comprehensive mortgage insurance coverage.

One downside is that they don’t have a rider that can cover you for disability. They only have a full disability insurance policy. But, it is an amazing plan for helping to protect your mortgage in the event of disability.

Canada Life Mortgage Protection Insurance Pros and Cons

| Pros | Cons |

|---|---|

| Unique Business Growth Protection rider | Limited additional insurance options: no critical illness or disability riders |

| Preferred rates available for those in excellent health condition | Limited access to online account features |

| Accidental death and disability waiver of premium benefits | |

| Several optional riders including accidental death and child’s term life | |

| Digital e-policy |

4. Empire Life Mortgage Protection Insurance – Best for personalization

Empire Life has some of the most versatile mortgage protection insurance in Canada. They give you 6 different, customizable policies and a ton of rider options that can cover a wide range of needs. You can create exactly the kind of policy you want to get coverage for almost anything!

Their Solution 25 policy is great if you need insurance for loans. You can also apply for longer or shorter term lengths, or buy optional critical illness and/or disability riders at an extra cost to cover all of your mortgage needs.

Empire gives you two options for critical illness riders: CI Protect for basic coverage or CI Protect Plus for more comprehensive mortgage insurance coverage. And, the basic plan includes a small death benefit for free. Add their disability rider on top of that and you have a great mortgage protection strategy.

Empire Life Mortgage Protection Insurance Pros and Cons

| Pros | Cons |

|---|---|

| Provides some of the most innovative insurance solutions in Canada | Critical Illness Protect Insurance only 10 or 20-year term |

| Several optional riders including accidental death & dismemberment, children’s life, and children’s critical illness rider | Disability Credit Protection maximum payment period only 1 or 2 years |

| Ability to exchange shorter term policies into longer Empire Life term policies (20, 25, and 30-year coverage options) | |

| Instant approval possible | |

| Electronic contract delivery possible | |

| Highly competitive annual or monthly premiums | |

| Comprehensive offering of insurance riders | |

| Online account access | |

| Digital e-policy |

5. iA Mortgage Protection Insurance – Best for flexibility

Industrial Alliance (iA) is a great choice if you want mortgage protection that’s flexible and gives you a lot of different options. Most mortgage protection plans are used to cover expenses. But this one is specifically meant to help you cover outstanding debts and loans, including your mortgage.

iA lets you choose from many different options, like coverage type and length. They also give you options for more coverage with a disability credit rider and critical illness transition. Both of these add-ons give you even more options so you can get exactly the type of coverage you want.

Tip: If you pick these rider options and decreasing coverage, you end up with a very strong mortgage protection plan.

iA Mortgage Protection Insurance Pros and Cons

| Pros | Cons |

|---|---|

| High degree of flexibility to design personalized coverage | There may be less expensive alternatives available for term coverage |

| Pick-a-term feature has few industry parallels | |

| Both level and decreasing options — decreasing term option can be used to match your mortgage | |

| Optional disability rider and critical illness riders make for strong overall mortgage protection | |

| Non-medical simplified and guaranteed product options available through Access Life product | |

| Online access to account | |

| Digital e-policy | |

| iA’s underwriting can be more accommodating than other providers |

6. UV Mortgage Protection Insurance – Best for riders

Many of the mortgage protection insurance products we’ve listed as the best in Canada give you options for riders — small add-ons you can buy for more coverage. But mutual Insurance company UV takes it a step further.

Their plan, Term Superior, is also offered as an optional rider. This is on top of their wide range of rider options for credit insurance, disability, and critical illness. And, you don’t need to do a medical exam or answer extra questions for their critical illness rider. It’s easy to see why we rated them the best for rider options!

UV’s plans also cover you for severe loss of autonomy for free. So, if you cannot perform at least 4 of the 6 activities of daily living before age 60, you will get up to 50% of the amount you were originally covered for.

UV’s Term Superior is also a great choice if you have multiple financial responsibilities. It helps if you want to use a strategy called laddering to get additional coverage for a low cost.

For Example

UV Mortgage Protection Insurance Pros and Cons

| Pros | Cons |

|---|---|

| Built-in Severe Loss of Autonomy benefit, at no extra charge | Critical illness rider benefit period only 2 years and only covers 3 conditions |

| Several optional riders including credit insurance and critical illness | |

| Preferred rates available starting at $500,000 | |

| Term 10, 20, 25, and 30 riders can be used for effective life insurance laddering strategy | |

| Digital e-policy |

Reviews of banks and lenders offering mortgage insurance

Although we strongly recommend that you get term life insurance for your mortgage, we did some research into what lenders are offering. This will help you to understand and compare the choices.

Keep reading to see some of the biggest banks and lenders for mortgage insurance, and how we’ve ranked them.

CIBC Insurance Mortgage Insurance Review

CIBC Insurance offers four types of coverage for mortgage insurance:

- Life insurance (unexpected death)

- Critical illness insurance

- Basic disability insurance

- Disability insurance plus (extended plan)

The first two types will make lump sum payments of either $750,000 or $500,000 (respectfully) of your outstanding mortgage balance. The two tiers of disability insurance offer different levels of coverage, and you can only apply for one.

Product details:

- Available Term Lengths: Up to age 70

- Available Term Types: Decreasing coverage

- Maximum Amount of Coverage: $750,000

Pros:

- Additional options to cover mortgage costs: critical illness insurance, disability insurance, disability insurance plus

- Discounts on mortgage critical illness, disability and disability plus for two approved applicants

- 30-day free look period

Cons:

- Only covers your mortgage, nothing else

- Only issued between ages 18 and 64, unless the client has an existing insured mortgage

- Only covers two people per mortgage

- Individuals cannot be covered for both disability and disability plus/job loss on the same mortgage

- Critical illness coverage only available up to age 55

- Limited number of critical illnesses covered (life-threatening cancer, acute heart attack, or stroke)

- Restrictions on coverage for disability and disability plus insurance

Manulife Mortgage Insurance Review

Manulife offers two options for mortgage protection: mortgage disability insurance and mortgage life insurance coverage. Their mortgage life insurance policy is the default option. The mortgage disability insurance is an extra option you can pay a little more to add on.

But, there’s a reason why we rated Manulife higher than the rest although we don’t recommend lender’s mortgage insurance. They cover a high amount of your outstanding mortgage.

Manulife’s mortgage insurance plan also includes two benefits at no additional cost:

- Waiver of premium due to job loss

- Terminal illness benefits

The company will waive monthly premiums for up to 3 months if you lose your job, or up to 24 months if you are diagnosed with a severe illness. But you can’t access either of these until you’ve had the plan for 6 months.

Product details:

- Available Term Lengths: Up to age 70

- Available Term Types: Decreasing coverage

- Maximum Amount of Coverage: $1,000,000

Pros:

- Additional options to cover mortgage costs: life insurance and disability insurance policies

- Added complimentary benefits: waiver of premium due to job loss and terminal illness

- 60-day free look period

- Competitive long-term rates compared to other lenders

- Coverage is portable and can be changed to different lender

Cons:

- Only covers your mortgage, nothing else

- Only issued between ages 18 and 64, unless client has existing insured mortgage

- No discounts for combined coverage

RBC Royal Bank Mortgage Insurance Review

RBC Insurance offers three options to cover mortgage payments:

- Mortgage life insurance – will pay out up to $750K in the event of death

- Mortgage critical illness insurance – will pay out up to $300K if you are diagnosed with a covered severe illness

- Mortgage disability insurance – will pay up to $3,000/month if you become disabled and cannot work

The mortgage life insurance policy is their default. Between the other two, you have to choose carefully — RBC Insurance only lets you get covered for one.

But one benefit is that RBC Royal Bank lets you use the payments for costs other than just your outstanding mortgage balance. You can use it to help pay off interest, overdrawn balances, prepayment charges, and other costs associated with ending your mortgage early (such as discharge fees, etc.)

Product details:

- Available Term Lengths: Up to age 70

- Available Term Types: Decreasing coverage

- Maximum Amount of Coverage: $750,000

Pros:

- Additional options to cover mortgage costs: critical illness insurance, disability insurance policies

- Payouts can be used for fees as well as actual mortgage balance

- 30-day free look period

Cons:

- Only covers your mortgage, nothing else

- No discounts for combined coverage

- Only covers two people per mortgage

- Individuals cannot have both critical illness and disability insurance protection under one mortgage

- Only issued between ages 18 and 64, unless client has existing insured mortgage

- Critical illness coverage only available up to age 55

- Limited number of critical illnesses covered (life-threatening cancer, heart attack, or stroke)

Scotiabank Mortgage Insurance Review

Scotiabank’s mortgage insurance will cover you in 4 different scenarios:

- If you suddenly die (life insurance)

- If you are diagnosed with a covered critical illness

- If you become disabled and cannot work

- If you lose your job/monthly income

They each will cover a decent amount of your outstanding mortgage debt. But the devil’s in the details. Only a certain amount of your outstanding debt will be covered. And only certain illnesses, disabilities, or circumstances will be covered.

Product details:

- Available Term Lengths: Up to age 70

- Available Term Types: Decreasing coverage

- Maximum Amount of Coverage: $1,000,000

Pros:

- Additional options to cover mortgage costs: life insurance, critical illness insurance, disability insurance, and job loss insurance

- Discounts for purchasing two or more insurance types and for mortgages over $350,000

- 30-day free look period

Cons:

- Only covers your mortgage, nothing else

- Only issued between ages 18 and 64, unless client has existing insured mortgage

- Job loss insurance only available with purchase of disability insurance policy

- Limited number of critical illnesses covered (life-threatening cancer, acute heart attack, or stroke)

- Restrictions on coverage for disability, critical illness, and job loss

To learn more about how mortgage default insurance works and how much it costs, head to our CMHC Mortgage Default Insurance Calculator.

What is mortgage insurance?

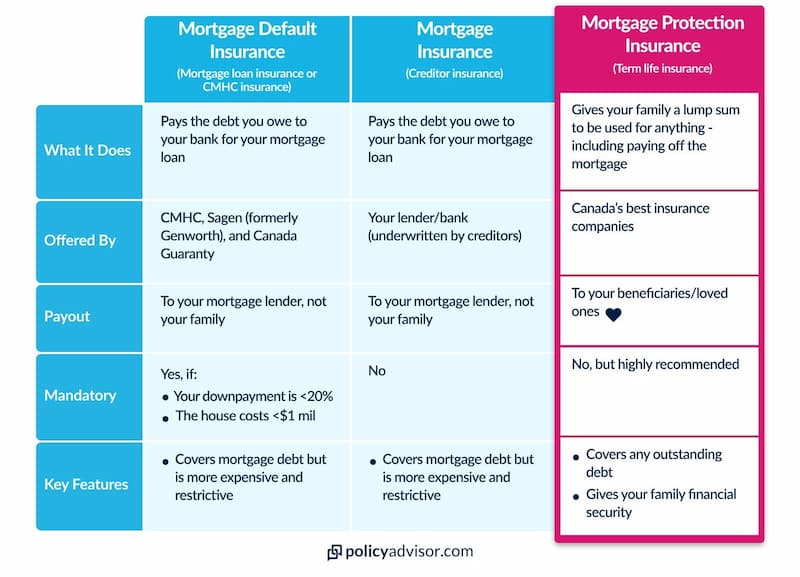

Mortgage insurance is a type of life insurance plan mostly sold by banks. It will pay the outstanding balance on your mortgage in case you suddenly pass away.

Mortgage insurance is not the same as Mortgage Loan Insurance or Mortgage Protection Insurance. This is one of the reasons why people get roped into buying it — there are so many different names out there that it can be confusing.

Private mortgage insurance or mortgage protection insurance is a term life insurance plan. It gives a payout called a death benefit to your beneficiaries at the time of death. They can then use that money for anything — the mortgage and/or something else too.

You do need some of these insurance products to secure your mortgage, but others you do not. The chart below will help you be able to tell the difference.

How does mortgage insurance work?

Mortgage insurance is primarily sold by banks. When you sit down with your mortgage broker or lender, they’ll likely offer you insurance on your mortgage. This insurance will pay off your mortgage in the event of death.

This is mortgage insurance. It only goes toward the insured balance of your mortgage. As you pay your mortgage off, the amount this type of insurance pays also decreases.

Mortgage insurance premiums are conveniently tacked onto your monthly mortgage payments. So, it sounds like a great protection plan for the biggest purchase of your life. But there are better options out there beyond what your broker or lender has to offer.

Who needs mortgage insurance?

Mortgage insurance can be a crucial financial safeguard for certain individuals like first time home buyers and young families. Here are some key groups that should consider mortgage insurance:

- First-time homebuyers

- Young families

- Single-income households

- Homeowners with high debt

- Elderly homeowners

Do I need to buy mortgage insurance from my bank?

No, you do not need to buy mortgage insurance from your bank or lender.

When you apply for a mortgage with a lender, it’s the mortgage broker or bank agent’s job to cross-sell their products to you. They may make it seem like you have to say yes to their insurance, but that’s not the case. You can opt for mortgage protection through life insurance instead.

Addtionally, you must remember that private mortgage insurance means the same thing as mortgage protection insurance. It’s a term life insurance product that gives a tax-free payment to your loved ones at the time of death. The payment can be used for anything, and it won’t change even if your mortgage changes.

Are mortgage life insurance and mortgage default insurance the same?

Mortgage life insurance and mortgage default insurance serve distinct purposes despite their similar-sounding names. Mortgage life insurance is designed to pay off your mortgage in full if you pass away during the mortgage term, ensuring your loved ones are not burdened with mortgage payments.

On the other hand, mortgage default insurance, often required by lenders for high-ratio mortgages with a down payment of less than 20%, protects the lender in case you default on your mortgage payments.

For example, think of John, a new homeowner, who decides to purchase his first home with a mortgage. Because John’s down payment is less than 20% of the home’s value, his lender requires him to obtain mortgage default insurance.

This insurance protects the lender in case John defaults on his mortgage payments, ensuring that the lender recovers their investment in the event of financial hardship.

Additionally, John decides to safeguard his family’s future by also purchasing mortgage life insurance. Unfortunately, John passes away unexpectedly during the mortgage term.

His mortgage life insurance policy pays off the remaining mortgage balance directly to the lender, relieving his loved ones from the burden of mortgage payments and allowing them to remain in their home.

Mortgage life insurance vs life insurance: What is the difference?

Mortgage life insurance and regular life insurance policies serve different financial purposes. Mortgage life insurance pays off the remaining mortgage balance if the insured passes away during the mortgage term.

On the other hand, regular life insurance provides broader coverage, offering a lump sum payment (death benefit) to beneficiaries in the event of the insured’s death. This can be used for various financial needs such as income replacement, debt payoff, and education expenses.

Difference between mortgage life insurance and life insurance

| Mortgage life insurance | Life insurance | |

| Purpose | Pays off the remaining mortgage balance if the insured dies during the mortgage term | Provides a lump sum payment (death benefit) to beneficiaries if the insured dies during the policy term |

| Coverage amount | Generally matches the outstanding mortgage balance | Can cover various financial needs, such as income replacement, debt payoff, education expenses, etc |

| Beneficiary | Typically pays the mortgage lender directly | The beneficiary can be designated by the insured and can use the funds as needed (e.g., family, estate, trust) |

| Premiums | Generally fixed premiums, often based on the mortgage amount and the insured’s age | Premiums can differ based on factors like age, health, coverage amount, and policy type (term, whole life, universal life) |

| Coverage duration | Typically matches the mortgage term (e.g., 15, 20, 30 years) | Policy terms can vary from short-term (e.g., 5 years) to lifetime coverage (whole life) |

| Flexibility | Limited flexibility; coverage is tied to the mortgage and decreases as the mortgage balance decreases | Offers more flexibility in terms of coverage amount, policy duration, and optional riders (e.g., critical illness, disability) |

| Underwriting requirements | Often simplified underwriting; may not require a medical exam for approval | Depending on the policy type and coverage amount may require medical underwriting, including a medical exam and health history review |

| Use of funds | Solely pays off the mortgage balance | Beneficiaries can use the funds for various purposes, including mortgage payments, living expenses, education costs, etc |

Is mortgage protection insurance better than lender’s mortgage insurance?

Yes. Private mortgage insurance from an insurance company is often far better than what banks and lenders offer, for many reasons including usage, lower costs, flexibility, higher coverage and more.

- Use — It can be used for debt repayment or anything, not just the monthly payments for your mortgage

- Lower cost — It’s usually a lot cheaper than lender mortgage insurance from a bank or creditor

- Flexibility — It can be changed into a permanent life insurance plan to cover you for the rest of your life

- Portability — It’s not tied to your home, so it will still protect you even if your mortgage changes

- Guaranteed death benefit — Your life insurance benefit amount doesn’t decrease as your mortgage is paid off

- More coverage — Easily combine life insurance with riders to protect your mortgage in the event of disability, illness, or more

PMI does a better job at covering your family. On the other hand, lender’s mortgage insurance only goes toward your mortgage. It’s for protecting the bank or lender, not you or your family.

Mortgage insurance may sometimes have its own benefits that may make the highest cost worthwhile to you. But, in general, we do not recommend that you buy this type of coverage.

How to connect with a mortgage insurance advisor in Canada?

If you want to speak with a professional to go over your options, talk to our expert advisors at PolicyAdvisor! Unlike the banks, our interest is in helping you protect the biggest financial risk you’ll take in your life.

Let us help you find the right mortgage insurance policy to form an iron-clad financial plan. Book a call with one of our insurance experts today!

Frequently asked questions

Do I have to have mortgage insurance?

Not necessarily. You may need to have Mortgage Default Insurance or CMHC Insurance in some circumstances. But you are not obligated to buy the mortgage insurance your bank is offering.

Instead, you should think about getting private mortgage insurance or mortgage protection insurance. They’re two terms that mean the same thing.

Mortgage protection insurance is sold by a third party, such as an insurance company or insurance broker like PolicyAdvisor.com. It is usually cheaper, gives you better coverage, and is more flexible — you can use it for anything you need, not just the mortgage.

Is private mortgage insurance worth it?

Yes, private mortgage insurance is worth it. It gives you more bang for your buck than creditor mortgage insurance from a bank or lender does. That flexibility, the lower cost, and the better peace of mind make PMI worth it.

Plus, you can use our online platform to get personalized quotes for mortgage protection in minutes — much easier than it takes to go through getting mortgage insurance from a bank or lender!

Does mortgage insurance go away after reaching 20 percent of payment in Canada?

No, the mortgage default insurance does not “go away” automatically after reaching 20 percent of the payment. The insurance premium is paid upfront initially because your down payment was less than 20 percent. The coverage lasts for the entire duration of the loan.

However, you can cancel the coverage once your loan balance reaches 80 percent or less of the borrowed amount.

Does mortgage insurance cover job loss?

Whether mortgage insurance covers a job loss depends on the type of insurance you get. Mortgage default insurance primarily protects the lenders and does not cover job loss. Mortgage protection insurance is designed to protect buyers and covers mortgage payments in the event of a job loss.

Canada’s best mortgage insurance companies are Canada Life, Industrial Alliance, Empire Life, Beneva, Assumption Life, and UV. We’ve given these ratings and reviews based on years of insurance expertise and research to help you make the best decision on how to protect your biggest asset.

These companies provide excellent protection for your mortgage through their term life insurance products when compared to bank-offered mortgage protection plans.