- Group insurance plans for small businesses offer comprehensive benefits to the employees of an organization

- Small businesses in Canada are increasingly recognizing the importance of group benefits which help with cost savings and tax advantages

- Pooled insurance plans are a collaborative strategy that allow multiple small businesses to come together and provide coverage to their employees

- The cost of a group insurance plan for a small business will depend on employee demographics, claims history, and plan details

- It's not mandatory to provide health and dental benefits to your employees, but it's an important part of maintaining a healthy workforce

Offering group health insurance is more than just a benefit; it is a strategic investment in your people and your business. It strengthens employee loyalty, increases job satisfaction, and supports a healthier, more engaged workforce that drives productivity, retention, and long-term success.

In this guide, we explain how small business group health insurance works in Canada, what it typically covers, and how employers can choose the right plan for their workforce.

How much does Group Insurance cost?

Get instant quotes from Canada's top group insurance providers and find the perfect coverage for your business.

Powered by

![]()

Understanding group health insurance for small businesses in Canada

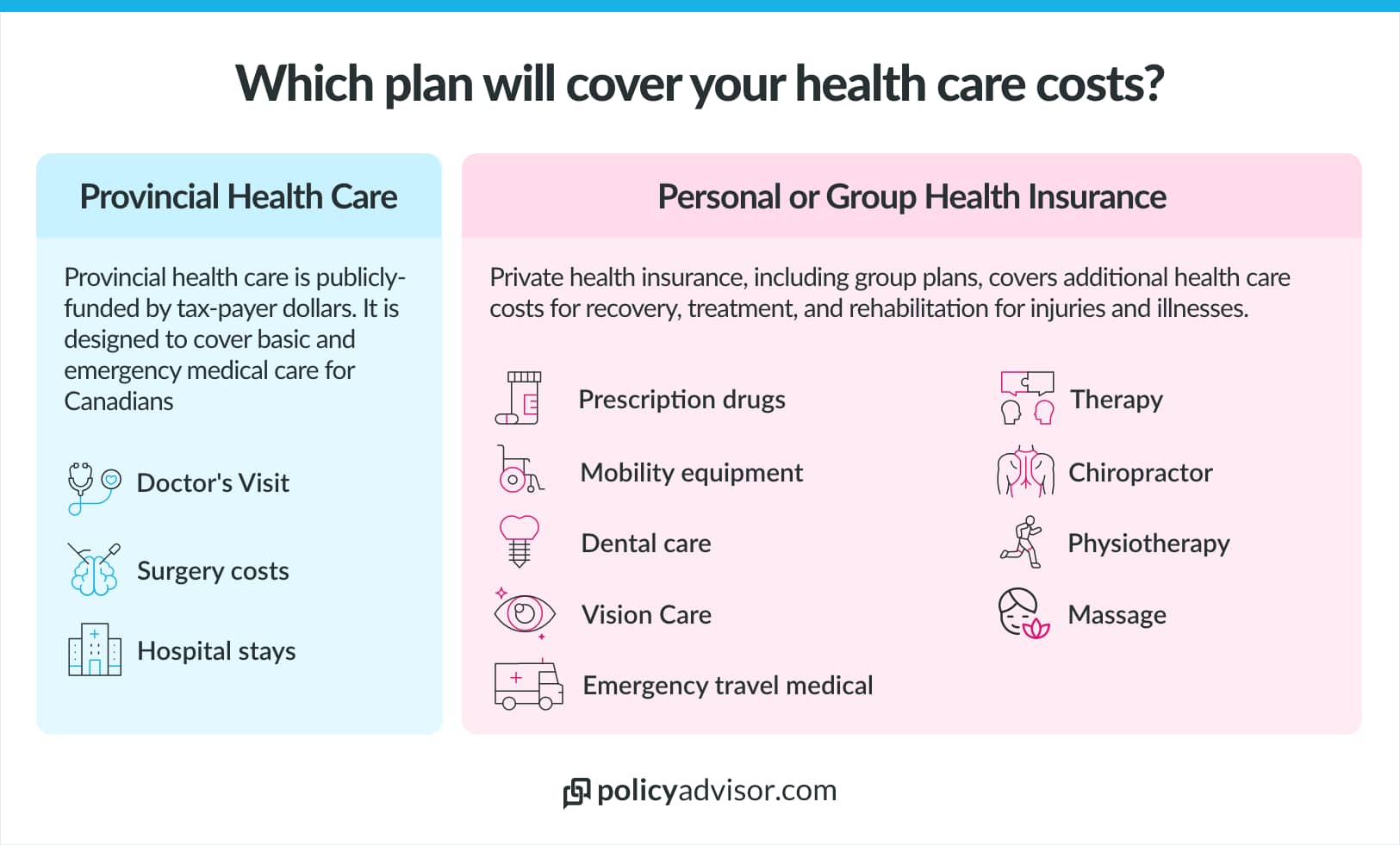

Small business group health insurance is a benefits plan that employers offer to employees as part of their compensation package. Instead of buying individual policies for its employees, the employer purchases a single policy that covers the entire team, often at more affordable rates.

Because the risk is spread across multiple employees, group insurance plans are typically more affordable and offer broader coverage compared to individual health policies.

These plans commonly include coverage for:

- Prescription medications

- Dental care

- Vision care

- Paramedical services

- Mental health services and counselling

- Life and disability insurance

- Emergency travel medical coverage

- Health spending account (HSA)

What does small business group health insurance cover?

Group employee benefits provide coverage for a variety of services, depending on the benefits package the business owner chooses. Here is what the group benefit plan will typically cover; some of these benefits are optional for businesses.

| Coverage Category | Covered Services & Items |

|---|---|

| Healthcare | Private hospital coverage, medical expenses and equipment, some elective surgeries, care homes and nurses |

| Vision care coverage | Eye exams, glasses, contacts |

| Dental coverage | Teeth cleanings, x-rays, cavity fillings, orthodontics (braces) |

| Prescription drugs | Cost of medication prescribed by a medical practitioner |

| Health spending account | A set amount per year that employees can spend on any item or service that improves their health |

| Health access | Some providers have online access to doctors and health service providers when you sign up for their group insurance plans |

| Emergency travel medical | Coverage if you have a medical emergency while travelling |

| Critical illness | A lump sum payment when you are diagnosed with a critical illness |

| Life insurance | A lump sum payment if you pass away from natural or accidental death |

| Short & long-term disability insurance | Salary replacement if you become disabled and cannot work for a short or long period of time |

| Accidental death and dismemberment (AD&D) insurance | Financial assistance if you have an accidental death, are dismembered or lose your sight. This would be in addition to a life insurance payment |

Why do small businesses need group health insurance?

Small businesses in Canada are increasingly recognizing the importance of group benefits. Some of the key reasons why small businesses need to offer group benefits to their employees are:

- Cost savings: Group health insurance pools risk among a group of people, leading to lower premiums. This makes it easier for small businesses to offer comprehensive coverage to their employees in a cost-effective manner

- Comprehensive coverage: Small business health insurance offers comprehensive benefits to cover hospitalization costs, preventive care, chronic disease management, and mental health support

- Tax advantages: Premiums paid for employee benefits packages are tax-deductible for businesses. This means that the cost of offering group benefits can be offset against the business’s taxable income

- Employee retention: Job seekers are increasingly prioritizing group benefits when considering employment opportunities. Offering comprehensive group benefits ensures higher rates of employee retention

- Wellness resources: Provides easy access to additional resources such as wellness programs and health management tools

What does a small business benefits package look like?

The following table illustrates what a group benefits plan looks like:

| Coverage | Basic | Standard | Enhanced |

| Health | |||

| Drug maximum | $3,000/person | $5,000/person | $10,000/person |

| Drug coinsurance | 80% | 80% | 80% |

| Paramedical services | $300/practitioner | $300/practitioner | $500/practitioner |

| Vision care | NA | $150/person for 24 months | $200/person for 24 months |

| Dental | |||

| Basic dental maximum | $700/person | $1,000/person | $1,500/person |

| Basic dental coinsurance | 80% | 80% (for basic)May include 50% (for major) | 80% (for basic)50% (for major) |

| Recall exam | 1 every 9 months | 1 every 6 months | 1 every 6 months |

| Pooled benefits | |||

| Life insurance | Optional | Optional | Optional |

| Accidental Death & Dismemberment (AD&D) | Optional | Optional | Optional |

| Disability benefits | Optional | Optional | Optional |

| Other benefits | |||

| Health Spending Account (HSA) | $100/year | $500/year | $1,000/year |

| Allowance account | As requested | As requested | As requested |

| Travel insurance | Yes | Yes | Yes |

*Representative illustration of what a small business health insurance plan looks like. Actual costs will vary.

How much does a small business employee benefits package cost in Canada?

The cost of an employee benefits package for a small business will depend on employee demographics, claims history, and plan details. Typical costs are approximately:

- $150/month/employee for a very basic plan: Covers essential healthcare needs such as limited prescription drugs, basic dental (preventive services only), and minimal paramedical coverage

- $205/month/employee for standard plan: Offers more balanced coverage, including higher coverage for medical services and covering basic and major dental expenses

- $275/month/employee for enhanced plan: Provides comprehensive coverage with higher reimbursement levels for any health issues and extensive dental care

Sample cost for small business employee benefits

| Coverage | Basic Plan | Standard Plan | Enhanced Plan |

| Health | |||

| Employees – single | $50/month | $70/month | $92/month |

| Employees – couple | $98/month | $130/month | $180/month |

| Employees – family | $110/month | $170/month | $195/month |

| Dental | |||

| Employees – single | $30/month | $60/month | $81/month |

| Employees – couple | $100/month | $128/month | $140/month |

| Employees – family | $170/month | $200/month | $250/month |

| Pooled Benefits | |||

| Life insurance & AD&D ($25,000/$50,000/$75,000) | $12/month | $18/month | $26/month |

| Critical illness | Not selected | Not selected | Not selected |

| Long-term disability | Not selected | Not selected | Not selected |

| Total monthly premium for 20 employees | $3,000/month | $4,100/month | $5,500/month |

| Cost per employee | $150/month | $205/month | $275/month |

*Illustrative pricing for a small business with 20 employees. Actual costs will vary.

Who qualifies for small business group benefits in Canada?

To be eligible for a small business group benefits plan in Canada, both the business and its employees must meet certain insurer-defined criteria. These typically include:

- Group size: Most insurers need a minimum of 2-3 members for participation; the actual group size varies from insurer to insurer

- Employee eligibility: Canadian under age 75, covered by their provincial healthcare plan, and working full-time

- Participation basis: Mandatory to join the plan

- Family content: Must be a true-employer-employee relationship receiving wages and/or a T4 from the plan sponsor

- Termination age: Retirement or age 75 (depending on insurer)

How is a small business benefits package set up?

A small business benefits package is set up in the following way:

- Sign up documents and group set up: Your sign up documents are shared by your advisor and need to be completed and signed. Once done, your group coverage is set up which can take up to two weeks

- Employee enrolment: Employees will get an activation email with instructions on how to enroll

- Billing: Once your employees are enrolled, you will receive the first billing statement

- Plan activation: Your plan is activated and your employees can start using their benefits

- Administrator access: Once your plan is all set up, you will receive the credentials to the administrator portal and the insurer will walk your designated administrator through the portal

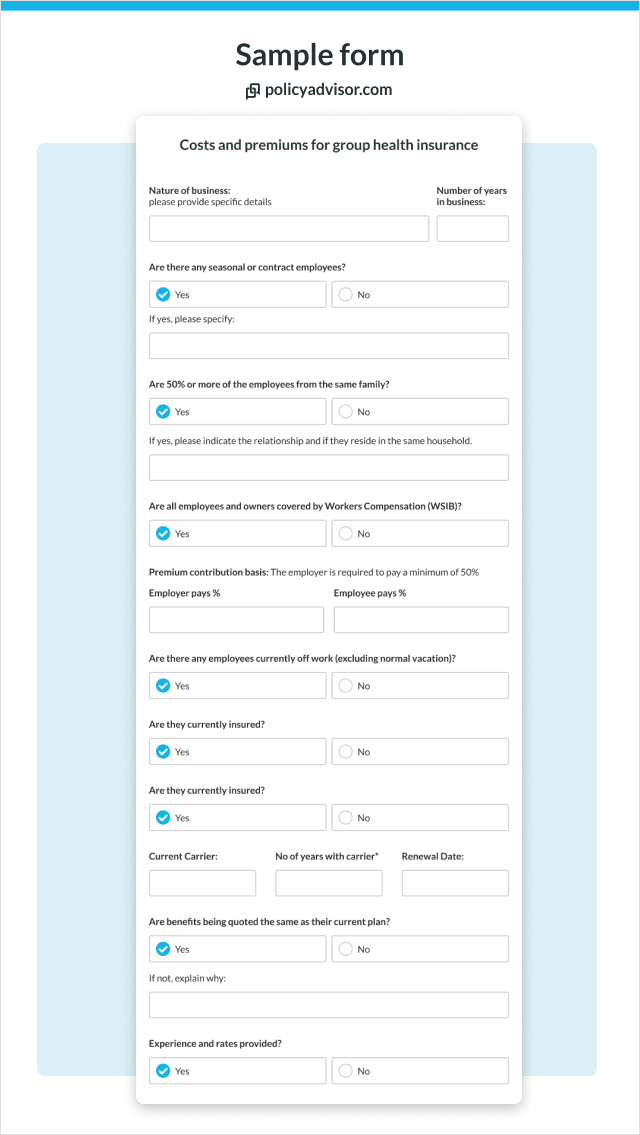

What will insurers ask on a company benefits package application?

Insurers will ask you about your company profile and employee demographics. Some of the questions that they might ask are:

- How many employees do you have?

- What industry is this business?

- Has your company had group insurance before? If so, provide a claims history.

- Is your company associated with a group or union?

- Do you want your benefits to differ by class (i.e. managers get one plan, regular employees get another)

- Are there any employees currently absent or on maternity leave?

- Are all your employees participating in this plan?

- Are your employees covered by worker’s compensation?

- Are any of your employees regularly working outside of Canada?

- About your employees. Tell us about their…

- Job title

- Date of employment

- Salary

- Hours

- Province of residence

- Date of birth

- Sex

- Family status (married, single, common-law)

- Dependents

Pooled vs experience-rated group benefits plans

Pooled plans combine multiple businesses to share risk and stabilize costs, while experience-rated plans price premiums based on how the employer utilizes the claim. Here is a table illustrating the difference between the two:

| Feature | Pooled plan | Experienced-rated plan |

| How pricing works | Premiums are based on the combined claims experience of multiple businesses | Premium is based on the company’s claim record |

| Premium stable | More stable | Often on the expensive side |

| Impact of high claims | Spread across the pool, hence less impactful | Directly affects the premium during renewals |

| Risk level | Lower risk for the employer | Higher risk for the employer |

| Best for | Businesses looking for affordable plans | Best for businesses with stable claims |

How to choose the best company benefit package for your small business?

When choosing a company benefit package for your business in Canada, ask yourself the following questions:

What kind of plan is the most suitable for my business?

Depending on your budget, decide if you want to pay for all the coverage or split the cost with your employees. You should also think about whether you want to offer group health benefits to your part-time employees or only to full-time staff.

What kind of coverage do my employees need?

Analyze your employees’ needs and find a plan that truly works for them. For instance, if you operate in a high-risk industry such as construction, you might want to consider a plan with comprehensive disability or accident coverage.

How much do I want to spend on group health benefits?

Assess your employees’ needs and finalize a budget that works for your organization. Compare plans and choose the one that best suits you.

How much will the cost increase during renewals?

Many small businesses focus only on the initial premium and overlook how it will change during renewal. Group health insurance premiums are typically reviewed annually, and high claims usage can lead to significant increases at renewal, which need to be taken into account

How much will the employee share?

Consider how premium costs will be shared between the employer and employees, and how this may affect both your budget and employee satisfaction

Which are the best companies for small business health insurance in Canada?

There are several group insurance providers out there with a wide range of plans to fit your business’s needs. At PolicyAdvisor, we work with 30 of Canada’s top insurance companies to get you the best rates on the benefits plans you need for your business.

| Company name | PolicyAdvisor rating | What sets them apart |

| Manulife | 5/5 | Flexible and customizable coverage |

| Equitable Life | 5/5 | Standardized and pooled plans |

| Sun Life | 5/5 | High dental and vision coverage |

| Empire Life | 4.5/5 | Mental health & virtual care |

| Canada Life | 4.5/5 | Extensive nationwide coverage |

| Desjardins | 4/5 | High paramedical coverage options |

| GreenShield (GSC) | 4/5 | Integrated digital care & claims process |

| Blue Cross | 3.5/5 | Higher travel coverage |

| Victor | 3.5/5 | Specialized solutions for unique industries |

| GMS | 3.5/5 | Cost-effective small business coverage |

While some companies offer different benefits and different prices, ultimately the best insurance company is the one that works best for your business needs. Like all insurance products, pricing and coverage will be specific to your unique business needs.

Get quotes for small business benefits package

If you’re looking for an affordable group benefits package for your small business, or business of any size for that matter, our licensed insurance experts at PolicyAdvisor are here to help. We’ll ask some questions about your business (like the ones listed above) and shop around to find you the best rate for health benefit plans for your employees.

Book a call with one of our friendly expert insurance advisors to chat about protecting your personal and financial health today!

Is group insurance for small businesses mandatory in Canada?

No. Employee benefits, such as health insurance, are not mandatory. However, providing insurance for your employees may provide that competitive edge your business needs to maintain employee retention.

The premium costs may seem like another additional expense to take on, but ultimately, having a healthy and consistent employee base will save you money in high turnover costs. Plus, insurance premiums can be claimed as tax-deductible business expenses.

Is group insurance tax-deductible for my business?

Yes. The premiums paid for group benefits are tax-deductible for businesses. This means that the cost of offering group benefits can be offset against the business’s taxable income.

What is an HSA? Can I just give employees a HSA instead of group benefits?

A Health Spending Account (HSA) is a personal fund designated for employees and their eligible dependants. It covers health and dental expenses not included in provincial health insurance or employer-sponsored group benefit plans for a fixed amount. However, they can’t replace full group benefits, as the money might be insufficient for large or unexpected medical expenses.

How can small businesses in Canada manage company health insurance plans?

Small businesses can manage group health insurance by working with licensed insurance advisors such as those at PolicyAdvisor. They can utilize online tools for employee enrolment and claims processing that insurers such as Sun Life, Benefits by Design, Equitable Life, etc. offer.

How can small businesses qualify for lower insurance premiums in Canada?

Small businesses can qualify for lower insurance premiums by evaluating their providers for competitive rates, opting for a higher deductible (which reduces premium costs), and regularly reviewing their plan (typically annually) to avoid any redundancies, such as covering employees no longer on their payroll.

Small businesses can also manage their premiums better by offering subsidized gym memberships or preventive care programs, which can lower long-term costs.

What are the consequences of not providing group health insurance for employees in small businesses in Canada?

There are significant consequences for small businesses that don’t provide group health insurance to employees:

- Difficulty in attracting and retaining talent: Nearly half (49%) of small business employees would choose health benefits over a pay raise, while 76% of employees without health benefits would leave their current job for one offering better coverage. These numbers highlight that any business, irrespective of its size, will find it difficult to attract or retain talent without employee benefits

- Lower employee productivity: A lack of health benefits can lead to decreased morale and engagement, as employees may feel undervalued and unsupported

- Increased business risks: Over 160,000 small businesses in Canada (1 in 8) have seen employee resignations due to better health benefits elsewhere. This turnover not only disrupts operations but also incurs high costs (in recruiting and training new employees), and increases business risks

How often should small businesses review and adjust their group health insurance plans?

Small businesses in Canada should review and adjust their group health insurance plans annually to evaluate changing employee needs, compare market offerings, adapt to workforce demographics, and optimize costs while maintaining valuable benefits.

How is group health insurance regulated in Canada?

Health insurance in Canada is strictly regulated and under the constant supervision of certain federal and provincial enforcement bodies. Canadian federal regulations, such as the Canada Health Act and Income Tax Act, govern most health insurance policies.

If you’re a small business owner buying group health insurance for your workforce, you must abide by regulatory guidelines for the greater good of your company and its assets. Using various educational resources and remaining up to date with the latest laws will help you keep up with regulatory changes.

Employee benefits plans attract and retain workers, promoting work-life balance. These plans usually include health and dental insurance, life insurance, disability insurance, retirement savings, and more. The cost of a small business employee benefits package depends on factors like employee demographics, location, claims history, and plan details. Employers can deduct the cost of providing group benefits from their taxable income.