- Group size, employee demographics, plan usage, occupation type, and plan selection impact group health insurance costs in Canada

- Employers can choose to cover the entire premium, split costs with employees, or divide expenses for different group health benefit packages

- Group health benefit plans can also be offered based on seniority, with different coverage levels for various employee groups

- Companies can apply for group health insurance by researching insurance companies, connecting with their advisors, providing company and employee information, answering carrier questions, reviewing and selecting plans, and enrolling employees

The cost of group health insurance in Canada typically ranges between $80 and $350 per employee per month in 2026, depending on the size of your business, coverage level, and employee demographics. For small businesses, premiums tend to be higher per employee, while larger organizations benefit from lower rates due to risk pooling.

In this guide, we break down key cost factors, monthly averages by business size, and proven ways to optimize your plan without overspending.

How much does Group Insurance cost?

Get instant quotes from Canada's top group insurance providers and find the perfect coverage for your business.

Powered by

![]()

What does group health insurance typically cover?

Group plans are often offered in different packages that are priced differently, with some that cover more benefits than others. Most insurers categorize group health insurance plans in three ways: basic, advanced, and premium.

To help you understand what each plan actually includes, here’s a detailed comparison of coverage across different plan types:

| Coverage | Basic | Standard | Enhanced |

| Health | |||

| Drug maximum | $3,000/person | $5,000/person | $10,000/person |

| Drug coinsurance | 80% | 80% | 80% |

| Paramedical services | $300/practitioner | $300/practitioner | $500/practitioner |

| Vision care | NA | $150/person for 24 months | $200/person for 24 months |

| Dental | |||

| Basic dental maximum | $700/person | $1,000/person | $1,500/person |

| Basic dental coinsurance | 80% | 80% (for basic)

May include 50% (for major) |

80% (for basic)

50% (for major) |

| Recall exam | 1 every 9 months | 1 every 6 months | 1 every 6 months |

| Pooled benefits | |||

| Life insurance | Optional | Optional | Optional |

| Accidental Death & Dismemberment (AD&D) | Optional | Optional | Optional |

| Disability benefits | Optional | Optional | Optional |

| Other benefits | |||

| Health Spending Account (HSA) | $100/year | $500/year | $1,000/year |

| Allowance account | As requested | As requested | As requested |

| Travel insurance | Yes | Yes | Yes |

*Representative illustration of what a small business health insurance plan looks like. Actual costs will vary.

What factors influence group health insurance costs in Canada?

Group health insurance costs in Canada are largely impacted by these factors:

- Group size and health

- Employee’s age and gender

- Claim history

- Occupation type

- Plan selection

- Group composition

- Coverage levels

- Use of the group plan

Group size and health: The size of an employee pool influences premiums, with larger groups often enjoying lower costs, meaning group health benefits for small businesses come with higher premiums compared to larger companies. However, pre-existing conditions within the group can make these expenses vary. For example, a company with 200 employees might pay lower premiums per employee compared to a small business with only 20 employees.

Employees’ age and gender: Group health insurance premiums often take into account the age and gender distribution of employees. For instance, the premium for employees over the age of 50 will be higher than for younger employees because they have a higher risk of illness.

Claim history: If an organization has a higher number of group health insurance claims in the past, its premium will be higher upon plan renewal.This is because a higher number of claims increases the risk an insurer takes when offering a group health plan.

Occupation type: Office-based occupations generally incur lower premiums because the risk of falling sick or of an accident is far lower than in hazardous sectors like construction.

Plan selection: Depending on how comprehensive the plan is and the benefits it offers significantly impacts the cost of group health insurance.

Group composition: Employers may offer tiered benefit plans that provide different levels of coverage based on seniority or job level. Executives or senior management may have access to premium plans with enhanced benefits, while junior staff members may be enrolled in standard plans with basic coverage.

Coverage levels: Group insurance rates are influenced by the coverage levels chosen, including copayments, deductibles, maximum coverage limits, and the number of insured individuals. Plans with lower co-pays and deductibles or higher coverage limits typically result in higher premiums.

Use of the group plan: The claims experience, or how frequently and extensively the plan is used by members, also affects costs. Higher utilization rates and frequent claims can drive up the overall cost of the group health plan.

Average group health insurance costs in 2026

The cost of a group health plan varies depending on the type of package an employer purchases, with options such as basic, advanced, and premium offering different levels of coverage.

Cost breakdown by plan type:

| Coverage | Basic Plan | Standard Plan | Enhanced Plan |

| Health | |||

| Employees – single | $50/month | $70/month | $92/month |

| Employees – couple | $98/month | $130/month | $180/month |

| Employees – family | $110/month | $170/month | $195/month |

| Dental | |||

| Employees – single | $30/month | $60/month | $81/month |

| Employees – couple | $100/month | $128/month | $140/month |

| Employees – family | $170/month | $200/month | $250/month |

| Pooled Benefits | |||

| Life insurance & AD&D ($25,000/$50,000/$75,000) | $12/month | $18/month | $26/month |

| Critical illness | Not selected | Not selected | Not selected |

| Long-term disability | Not selected | Not selected | Not selected |

| Total monthly premium for 20 employees | $3,000/month | $4,100/month | $5,500/month |

| Cost per employee | $150/month | $205/month | $275/month |

*Illustrative pricing for a small business with 20 employees. Actual costs will vary.

Cost breakdown by coverage:

| Category | Typical Cost Contribution | What Drives the Cost |

| Health & Prescription Drugs | 40–60% (highest) | High-cost medications, frequent claims, chronic conditions |

| Dental Coverage | 20–30% | Regular usage (cleanings, checkups), major procedures like crowns & bridges |

| Paramedical Services | 10–20% | Number of services covered (physio, chiro, massage) and annual limits |

| Vision Care | 2–5% (low) | Predictable claims (eye exams, glasses every 1–2 years) |

| Life Insurance | 5–10% | Employee salaries, age distribution |

| Disability Insurance (STD/LTD) | 5–15% | Industry risk, workforce demographics |

Who pays for a group health plan in Canada?

Different organizations have different rules when it comes to paying group health insurance premiums. Generally, there are three ways in which the premiums for group health insurance are paid. These are:

- Employer-sponsored plans: The employer pays the entire cost of the group health benefits plan, and the employee is not expected to contribute

- Cost sharing with employees: An employer and their employees split the premium costs at a predefined rate. Commonly used splits are 50 percent each or 70 percent by the employer and 30 percent by the employee. These arrangements can differ depending on the specific plan and the agreements between the employer and its employees

- Employee add-on costs: If employees want to add dependents or get an advanced plan with additional benefits, they have the option to pay the extra premium

Depending on organizational budgets, goals, and employee requirements, employers can choose to pay for or split the cost of group health insurance premiums; the choice truly lies with the employer.

For instance, a startup may opt for a cost-sharing arrangement, with the employer covering 70% of the premiums to make it more affordable, while still providing valuable benefits to employees. Alternatively, a larger corporation may choose to pay for a comprehensive group health insurance plan without any contribution from the employees.

How to manage and reduce group health insurance costs?

You can attempt to reduce your group plan costs by considering the following:

- Evaluate and customize plans: Regularly reviewing and tailoring health plans to fit the group’s specific needs can prevent overpaying for unnecessary coverage

- Promote preventive care: Encouraging preventive care measures, such as regular checkups and screenings, can reduce the incidence of serious health issues and lower long-term costs

- Virtual health care: Offering virtual health care options can decrease costs by reducing the need for in-person visits and providing convenient access to medical advice

- Cost-sharing models: Implementing cost-sharing models, where employees contribute to the cost of their care through co-pays and deductibles, can help manage overall expenses

- Health and wellness programs:Introducing comprehensive health and wellness programs can improve overall employee health, leading to fewer claims and lower healthcare costs

- Wellness incentives: Providing incentives for healthy behaviours, such as gym memberships or wellness challenges, can encourage a healthier workforce and reduce healthcare spending

Is group health insurance worth the cost for small businesses?

For most small businesses in Canada, group health insurance is less of a cost and more of a strategic investment. Even a basic plan can help you:

- Attract and retain employees in a competitive market

- Improve productivity and reduce absenteeism

- Offer meaningful benefits without significantly increasing salaries

For small teams, even limited coverage can deliver strong value (both for employees and the business). The costs can be controlled through plan design and cost-sharing. Plus, premiums are typically tax-deductible, making them more cost-efficient than direct compensation.

Key considerations for choosing group insurance plans

Employers should look at supporting their employees’ health and wellness by offering a comprehensive group health benefits plan that includes:

- Benefits covering pharmacy, healthcare, and dental care needs

- Short and long-term disability coverage

- Critical illness benefits

- Employee and family assistance programs to aid stress management

- Resources on identifying and managing prevalent mental health concerns

Alongside diverse benefits, employers must also compare:

- Premiums: The monthly/annual payment for employees’ initial expenses for health insurance coverage

- Deductibles: Annual amounts employees must pay before insurance coverage starts, in addition to premiums, unless the employer chooses to pay them

- Copayments: Fixed charges employees incur for health services

- Coinsurance: Amounts employees are obligated to pay after meeting deductibles and other conditions

How to apply for group health insurance in Canada

Applying for group health insurance in Canada is a straightforward process, typically initiated by the employer on behalf of their employees. Here’s a step-by-step guide:

- Research carriers: Start by researching insurance carriers in Canada that offer group health insurance plans. Some well-known carriers that offer group plans include Sun Life, Manulife, Canada Life, Equitable Life, Blue Cross, GMS, and Wawanesa. Each carrier may offer different plans and options, so it’s essential to compare their offerings to find the best fit for your organization

- Connect with our advisors: >Reach out to our advisors at PolicyAdvisor and inquire about our group health insurance plans. Our insurance experts will provide you with information about the plans we offer, including coverage options, premiums, and any additional benefits. They will also make it easy to review and compare plans across the market, helping you find the best plans for your coverage needs

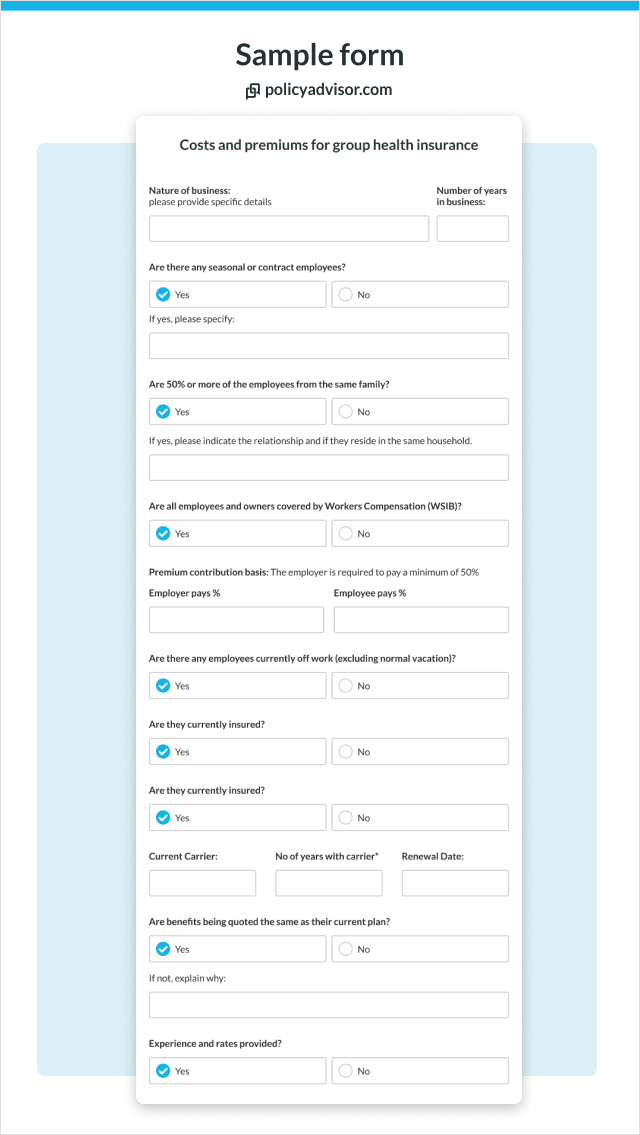

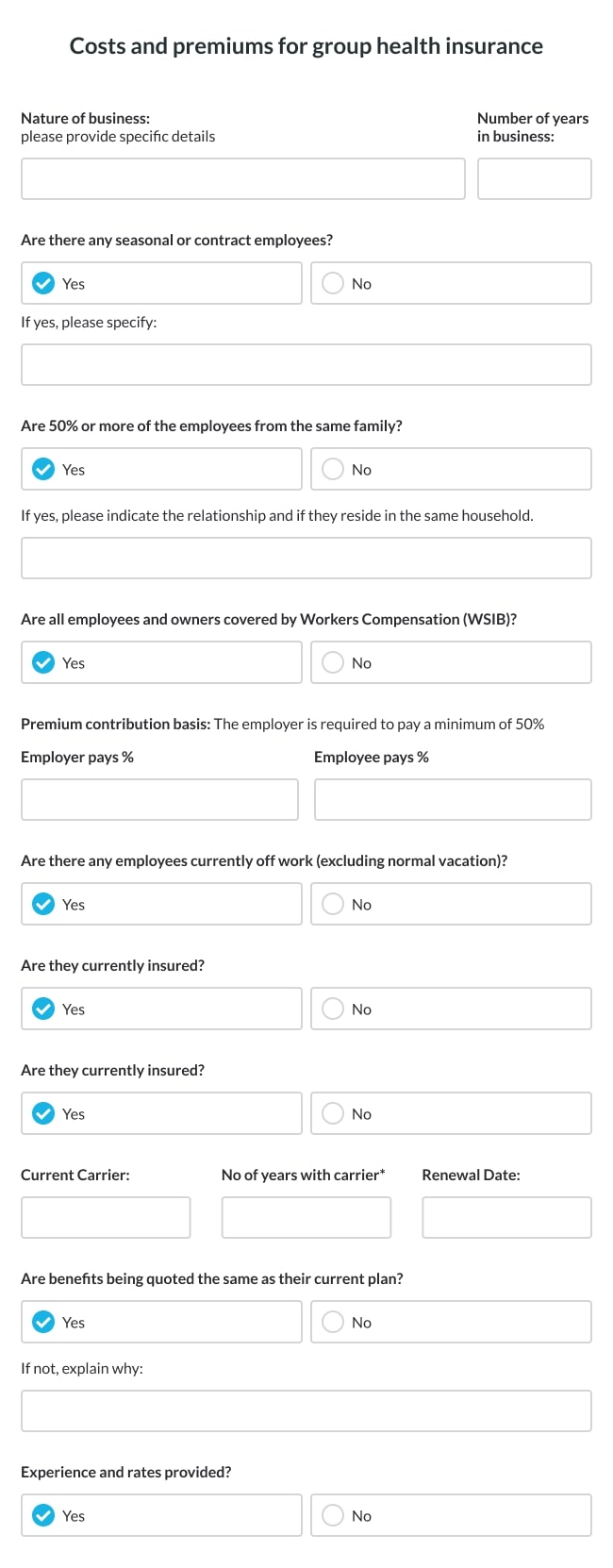

- Provide information through a form: During the application process, the insurance carrier will likely ask for details about your company, such as the number of employees, industry type, and business structure. They may also request information about the desired coverage levels and any additional benefits you wish to include in the plan

- Review and select:Once you have provided all the necessary information, the insurance companies will review the information and provide quotes for the proposed plans. You can then review the proposed group health insurance plans from each carrier. Consider factors such as coverage, premiums, network of healthcare providers, and additional benefits before making a decision

- Enrolment: After selecting a plan, the next step is to enroll your employees in the group health insurance program. The carrier will assist with the enrollment process, including providing enrollment forms and instructions for your employees to complete

Know more about the best health insurance companies in Canada

How to buy an affordable group health insurance plan in Canada?

At PolicyAdvisor, we have a team of licensed insurance experts who will help you buy the best group health insurance plans and provide you with information about the coverage options, premiums, and any additional benefits that you would like to offer your employees. Schedule a call with our experts today!

Frequently asked questions

Why is group insurance cheaper for large companies?

Larger companies benefit from risk pooling, where the cost is spread across a bigger group of employees. This reduces the impact of individual claims and allows insurers to offer lower premiums per employee.

Can I customize my group benefits plan?

Yes, most insurers offer flexible plans where you can adjust coverage types, limits, and employer contributions. This allows businesses to design a plan that fits both their budget and employee needs.

What is the minimum number of employees required?

Most insurers require at least 2 full-time employees to qualify for group coverage. Some providers may have additional eligibility criteria based on business type and structure.

Can I change or upgrade my plan later?

Yes, businesses can usually review and update their plans at renewal time each year. This allows you to adjust coverage, add benefits, or optimize costs as your team grows.

What factors increase group insurance costs?

Costs can rise due to comprehensive coverage (dental, paramedical), older workforce, high claims history, and high-risk industries. Adding more benefits or higher limits also increases premiums.

Is group insurance cheaper than individual health insurance?

Generally, yes. Group insurance offers better pricing and broader coverage because the risk is shared across multiple employees, making it more cost-effective than individual plans.

What if an employee has a pre‑existing condition?

Group plans generally do not require medical underwriting for extended health and dental at enrolment, but waiting periods and exclusions can apply based on the contract.

Understanding and calculating the costs of group health insurance plans in Canada can be daunting, with various factors influencing premiums. In this article, we shed light on the key determinants affecting pricing, such as group size, claims history, and plan selection. Moreover, we provide insights into applying for group insurance and offer expert advice on finding affordable plans tailored to your organization’s needs.