1-888-601-9980

1-888-601-9980Group Health Insurance for Small Businesses

Employee benefits plans attract and retain workers, promoting work-life balance. These plans usually include health and dental insurance, life insurance, disability insurance, retirement savings, and more. The cost of a small business employee benefits package depends on factors like employee demographics, location, claims history, and plan details, typically ranging from $50 to $300 per employee per month. Employers can deduct the cost of providing group benefits from their taxable income.

- Group health insurance for small businesses

- How group health insurance works

- Types of group health insurance plans

- Understanding pooled insurance plans

- Key benefits of group health insurance for small businesses

- Factors to consider for group health insurance

- Understanding provincial vs private vs group health plan

- Group benefits coverage

- Best group health insurance for small businesses

- Group health insurance cost and pricing

- Compliance and regulations

- Frequently asked questions

When you run a small business, your tiny (but mighty) team means everything. They deserve to be compensated for their hard work—and we mean more than just their salary. Health insurance for small businesses are a great way to attract and retain workers for the long term.

These benefits, often known as employee benefits or group benefits, can make employees feel protected against all odds, enhancing job satisfaction. They also promote substantial work-life balance and help employees develop a sense of loyalty towards their company.

But what will it cost you to provide employee benefits? When you run a small business, we know every penny counts. Our blog aims to provide comprehensive insights into what employee group benefits cover if you have to offer them and how to get the best deal for group health insurance for small businesses.

Understanding group health insurance for small businesses

Group health insurance is a specific type of insurance plan that companies can offer their employees. This plan safeguards employees and their dependents in case of any unforeseen medical emergency that can potentially impact their finances.

Group health insurance may cover an employee’s overall health and dental insurance. However, companies may even customize their plans to include other benefits such as vision care, disability insurance, prescription drug coverage, and more.

Learn more about the types of group health insurance for small businesses in Canada

How group health insurance works

Group health insurance usually works in the following way:

- A company or a small business purchases a group health insurance plan from an insurance provider for its employees

- The plan typically allows employees to enroll their dependents, such as spouses and children

- Group health insurance plans usually have lower premiums because the risk is distributed across a larger pool of people

- When a group member submits a claim, the provider (generally the hospital, clinic, pharmacy, etc.) submits the claim to the insurance company which reimburses the provider

- Group members may have to pay some expenses, such as deductibles and copays

- Employers may either cover part or all of the premium as an added benefit to their employees

- Group plans often provide comprehensive coverage, including doctor visits, hospital stays, prescription drugs, and more

- These plan usually provide coverage for pre-existing conditions without any waiting period

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

Types of group health insurance plans in Canada

If you’re looking to provide additional perks to your employees and earn their unwavering loyalty, providing health insurance benefits is definitely the way to go. Several types of medical insurance plans are available for small businesses operating in Canada. They are as follows:

1. Employer-sponsored benefits

Employer-sponsored benefits are health insurance plans provided by a company to its employees as part of their compensation package. The employer may cover the premium expense completely or partially on behalf of their employees.

Advantages

- Reduced premium costs due to employer contributions

- Often includes additional benefits like dental, vision, and wellness programs

Disadvantages

- Limited plan options are available compared to the individual market

- Coverage is tied to employment status and losing a job usually means losing coverage

2. Government-sponsored benefits

Government-sponsored benefits, as the name suggests, are health insurance policies that are provided to Canadian citizens by the provincial or federal governments. These health insurance plans typically cover a specific demographic that may not receive lucrative coverage from other health insurance plans.

Advantages

- Provides access to essential health care services for vulnerable populations

- Often includes comprehensive benefits with low out-of-pocket costs

- Medicaid and CHIP offer additional support services, such as transportation to medical appointments

Disadvantages

- Eligibility requirements can be strict, limiting access only to certain individuals

- Some programs may have limited provider networks, leading to challenges in accessing care

3. Professional association benefits

Professional association benefit is a special insurance policy that is offered to members of a specific association, such as trade organizations, retirement committees, alumni groups, etc. These plans are designed to provide group coverage to individuals who share a common profession, industry, or affiliation.

Advantages

- Access to group rates for individuals who might not otherwise qualify for employer-sponsored insurance

- Tailored coverage options that meet the specific needs of the association’s members

- May offer additional benefits such as professional development resources or networking opportunities

Disadvantages

- Coverage and benefits can vary widely depending on the association

- Smaller risk pools compared to employer-sponsored plans

4. Health Spending Accounts (HSAs)

HSAs are a type of tax-advantaged savings account that provides a mutually beneficial way for companies and small businesses to provide health and dental benefits to their employees and receive tax benefits from them.

HSAs offer several benefits to both employers and employees alike, making it a top choice for many small businesses.

Benefits for employers

- Offering an HSA plan can help to minimize an employer’s healthcare premium expenses as compared to other health plans

- Employer contributions to employee HSAs are exempt from payroll taxes

- Providing HSAs may also boost a sense of loyalty among employees and improve employee retention rates

Benefits for employees

- Employees have full control over their HSA account, allowing them to keep a tab on their medical expenses

- Employees also receive tax benefits from their HSA account as the total taxable income goes down

- HSAs can easily be ported even if an employee decides to switch companies

What is a pooled insurance plan?

The two biggest factors in determining the price of your group health insurance are your claims history and industry. But what if it’s your first time? Or what if your business is in a high-risk industry?

If you don’t have any history, an insurance company might put you in a pooled insurance plan. In this scenario, insurance companies pool your business with others so that they can collect the premiums from everyone and use that to cover any claims.

Benefits of pooled insurance for small businesses

- Affordability: This plan makes health insurance more affordable by reducing premium and administrative costs

- Stability: Pooled insurance reduces the risk of large, unpredictable claims, which can help small businesses manage their budgets more effectively.

- Flexibility: Pooled plans usually offer flexible coverage options that can be tailored to meet employees’ diverse needs.

Once you have a few years of claims history under your belt, you may qualify for your own individual pricing. This is because the insurance underwriter has a better idea of how often they’ll be paying out for your employee’s claims.

Having health insurance means more than financial protection—it provides peace of mind. Your quality of life is directly linked to your health care. Having health insurance allows you to focus on your well-being without worrying about potential expenses. And that is priceless!

What are employee benefits?

Employee benefits, also known as a group benefits package, refer to a set of perks and advantages provided by an employer to their employees as part of their overall compensation package. These benefits go beyond the basic salary or wages and are designed to attract, retain, and motivate key employees while enhancing their overall well-being. Benefits usually include health & dental insurance, life insurance, disability insurance, stock options, and retirement savings plan matching.

Key benefits of group health insurance for small businesses

Small businesses can have a lot of benefits from investing in group health insurance for their employees. Some of the key benefits are as follows:

- Cost savings: Group health insurance offers lower premiums, which helps in cost savings for the company

- Comprehensive coverage: It offers a wide range of coverage benefits, including hospitalization costs, preventive care, chronic disease management, and mental health support

- Guaranteed coverage: Small business health plans cover employees with pre-existing conditions, so the chances of not getting insurance are small

- Tax advantages: This insurance plan can offer tax-based advantages and significant deductions for both the employer and their employees

- Employee retention: Offering lucrative group health insurance benefits ensures higher rates of employee retention

- Wellness resources: This plan provides easy access to additional resources such as wellness programs and health management tools

Factors to consider when choosing a group health insurance plan

While choosing the best group health plan that can be mutually lucrative, there are a few things that must be taken into consideration. They are as follows:

- The company size and demographics

- Budget

- Coverage options

- Customization options

- Ease of administration

We’ve explained each of these below so that you can choose the perfect group health insurance plan for your work squad:

1. Company size and employee demographics

Company size can play a crucial role in choosing the right group health insurance plan. Small to mid-sized companies have fewer employees than large organizations with thousands of employees worldwide. It is important to understand your employees’ needs and craft personalized plans that suit them.

2. Budget and cost considerations

An in-depth budget consideration is a must before making a group health insurance purchase. Conducting thorough research before choosing an insurance plan may help you get a reasonable premium quote without the added burden of scaling your revenue just to keep up with the costs.

3. Coverage options

While purchasing a medical insurance plan for your employees, it’s important to consider the types of benefits that you might want to add. Some companies provide only health and dental benefits, whereas other companies may provide additional coverage such as vision care, pre-existing disease coverage, disability rider, and more.

4. Flexibility and customization

Every individual may have a unique set of medical problems or complications. Offering customization may also help your employees choose the benefits that they want, curated to their diverse needs.

Additionally, small businesses may customize their group health insurance plans based on their business parameters and employee demographics. Providing flexibility helps cater to a diverse range of medical requirements with ease

5. Ease of administration

In this day and age, too much paperwork can be tedious for small businesses to deal with. Group health insurance plans offering administrative simplicity have become the top choice for most employers.

Businesses look for insurance plans that provide complete support, guidance, and additional tools to streamline record maintenance, premium deposit, payout, and more, ensuring smooth plan management from start to finish.

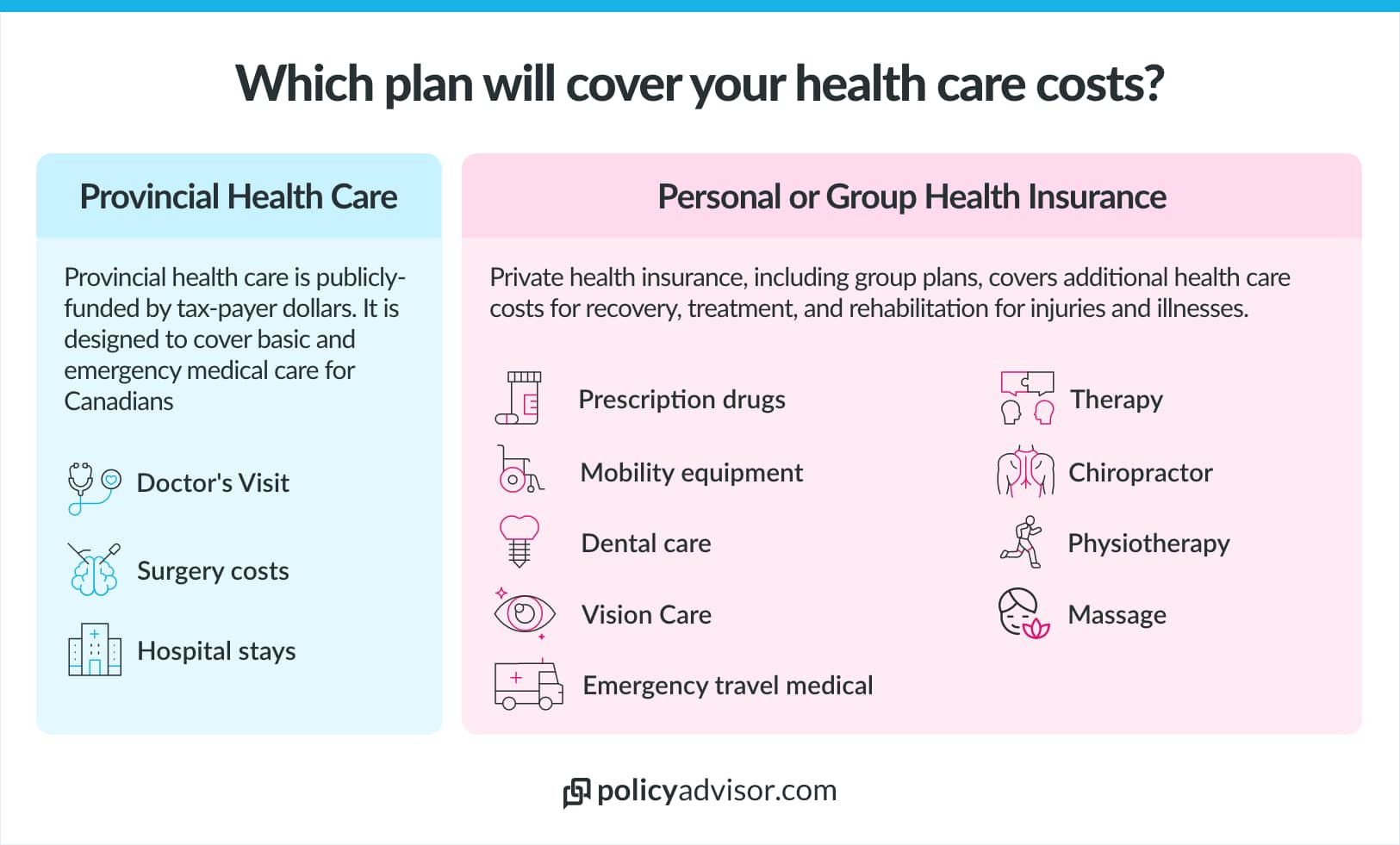

Provincial health plans vs group health plans vs private health plans

Canada is known for having “free” health care, so some might be wondering why private or group health insurance is even needed. Government health care in Canada is administered by each province. Provincial health care plans are designed to cover emergency and basic medical care. For example, surgeries and doctor visits. Extended benefit plans provide coverage for recovery efforts after an emergency or general health maintenance.

What do group benefits cover?

Group employee benefits can cover a variety of insurance products, depending on the group plan the business owner chooses.

| Coverage Category | Covered Services & Items |

|---|---|

| Healthcare | – Private hospital coverage

– Medical expenses – Medical equipment – Some elective surgeries – Care homes and nurses |

| Vision care coverage | – Eye exams

– Glasses – Contacts |

| Dental coverage | – Teeth cleanings

– X-rays – Cavity fillings – Orthodontics (braces) |

| Prescription drugs | – Medication |

| Health spending account | A set amount per year that employees can spend on any item or service that improves their health |

| Health access | Some providers have online access to doctors and health service providers when you sign up for their group insurance plans |

| Emergency travel medical | – Coverage if you have a medical emergency while traveling

– Trip cancellation/interruption |

| Critical illness | A lump sum payment when you are diagnosed with a critical illness |

| Life insurance | A lump sum payment if you pass away from natural or accidental death |

| Short & long-term disability insurance | Salary replacement if you become disabled and cannot work for a short or long period of time |

| Accidental death and dismemberment (AD&D) insurance | Financial assistance if you have an accidental death, are dismembered or lose your sight. This would be in addition to a life insurance payment |

Who are the best health insurance companies for small business owners?

There are a lot of group insurance providers out there with a wide range of plans to fit your business’s needs. At PolicyAdvisor, we work with 30 of Canada’s top insurance companies to get you the best rates on the benefits plans you need for your business.

| Company | Best for… |

|---|---|

| Desjardins | Combo plans |

| GMS | Comprehensive coverage (80-90%) |

| Blue Cross | Customized coverage options |

| SunLife | More than 50 employees |

| Equitable Life | Health spending accounts |

| Canada Life | Small business owners |

While some companies offer different benefits and different prices, ultimately the best insurance company is the one that works best for your business needs. Like all insurance products, pricing and coverage will be specific to your unique business needs.

What will they ask about my business on a group health insurance application?

Applications for group health insurance are a little different from individual plans. With private health insurance, the insurance provider is concerned about the individual’s health history and age. With group insurance, they don’t do as much individual underwriting. Instead, they’ll want to know more about the general employee demographics.

What will be asked on a group insurance application?

|

Employees will notice that when they sign up for their group employee benefits, they won’t be asked as many health questions that normally come with individual insurance applications. Instead, the underwriting factors are more heavily weighted on your business’s claims history and industry claims history. If your employees claim a lot, the insurance company will price their premiums accordingly.

- MetLife

Costs and pricing of group health insurance

Once you’ve decided to buy group health insurance for your team, it’s time to set up a budget and compare your options accordingly. The cost of premiums may vary significantly depending on the plan you choose, add-on features, and your team size.

Here are some factors that can affect the price of a small business medical insurance in Canada:

- Number of employees

- Age and health status of employees

- Coverage levels

- Industry and location

Based on the above factors, each insurance company develops a premium amount that must be paid periodically. Companies with a higher number of employees, older employees, or businesses located in the prime cities of Canada may have to pay a higher premium than smaller companies with a relatively younger workforce.

Know more about the costs and premiums of group health insurance.

How much does a small business employee benefits package cost in Canada

The cost of a group insurance plan for a small business owner will really depend on their employee demographics, claims history, and plan details. In general, the larger the employee base, the cheaper the cost per employee. This is because the insurance company can spread the risk out—the employees that don’t claim a lot make up for the ones that do. For a small business, the price will be more contingent on industry type and claims history.

| Mike’s Diner |

| Employee count: 9 |

| Province: Ontario |

| Industry type: Retail |

| Claims history: None |

| Unions or groups: None |

| Absences or leaves: 1 on maternity leave |

| All employees participating? Yes |

| Workers compensation? Yes |

| Working outside of Canada? No |

| Do benefits differ by class? No |

| Benefits plan type: Basic |

| Cost to employer per month for benefits plan: Basic (no dental) $445 ($50/employee) Basic (with dental) $1,175 ($130/employee) |

Who pays the group insurance premiums?

It depends on the company. Some companies will provide their health and dental plans to their employees completely free. This means the business owner will cover all the health insurance premiums. Other businesses will charge a small fee to their employees to participate—usually deducting this premium directly from the employee’s paycheck. Some small businesses will offer free participation for standard plans and if the employees want more comprehensive coverage, they can opt for additional deductions from their pay.

Are group benefits tax deductible in Canada?

Yes, group benefits provided by an employer are generally tax-deductible in Canada. Employers can deduct the cost of providing group benefits, such as health and dental insurance, from their business income when calculating their taxable income.

| The Canada Revenue Agency (CRA) has specific guidelines regarding the deductibility of employee benefits.

Here are a few key points:

It’s important for employers to consult with a tax professional or review the CRA guidelines to ensure they are complying with the specific rules and requirements for deducting group benefits. |

Compliance and regulations

Health insurance in Canada is strictly regulated and under the constant supervision of certain federal and provincial enforcement bodies. Basically, each level of government plays a distinct role in ensuring the proper functioning of the health insurance system.

Canadian federal regulations, such as the Canada Health Act and Income Tax Act, govern most health insurance policies. Several provincial regulations, such as insurance legislatures, consumer protection rights, etc., are also prevalent in most provinces to ensure the complete security of the insured individual and their dependents.

Similarly, voluntary organizations such as the Canadian Life and Health Insurance Association (CLHIA) represent insurance companies to ensure regulatory fair play and present a united front when voicing an opinion on a national scale.

For instance, the Canadian government also legally recognizes substance usage and alcoholism as disabilities, ensuring such individuals and their families are well-protected.

If you’re a small business owner buying group health insurance for your workforce, you must abide by regulatory guidelines for the greater good of your company and its assets. Using various educational resources and remaining up to date with the latest laws will help you keep up with regulatory changes.

Get quotes for group health and dental insurance

If you’re looking for an affordable group benefits plan for your small business, or business of any size for that matter, our licensed insurance experts at PolicyAdvisor are here to help. We’ll ask some questions about your business (like the ones listed above) and shop around to find you the best rate for health benefit plans for your employees.

Book a call with one of our friendly expert insurance advisors to chat about protecting your personal and financial health today!

Frequently Asked Questions

Are employee benefits mandatory?

No. Employee benefits, such as health insurance, are not mandatory. However, providing insurance for your employees may provide that competitive edge your business needs to maintain employee retention. The premium costs may seem like another additional expense to take on, but ultimately having a healthy and consistent employee base will save you money in high turnover costs. Plus, insurance premiums can be claimed as tax-deductible business expenses.

What is the cheapest group health insurance for small businesses?

Some plans offer group benefits for as low as $25-75 per employee, but it depends on the plan. Cheap plans usually mean minimal coverage—just basic medical expenses with no dental, vision, and/or minimal paramedical expense coverage. However, cheaping out on benefits can leave your employees high and dry when they need the coverage the most. Having a healthy employee base means they’re able to work and having adequate coverage to pay for health expenses is an important aspect of this.

What is an HSA?

An HSA is short for “Health Spending Account.” This is an additional benefit sometimes included in group health insurance plans that a lot a certain dollar amount each year for an employee to spend on health-promotional or recreational products. For example, you might use your health spending account to pay for part of your gym membership, an exercise bike, or an Apple watch. It’s designed to offer flexible coverage for services and items that still promote healthy living but don’t necessarily fit.

How much do benefits cost per employee?

The cost of group benefits really depends on your group plan. Generally, it can range from $50-$300 per month per employee. Some employers will have their employees contribute a fraction of this premium to help cover the cost. Business owners can also count these premiums as a deductible business expense on their tax return.

Do certain small businesses get discounts depending on their industry?

It’s not a discount, per se. But industry type is one of the more weighted factors in determining the price of group insurance. If historically, that industry has more claims than others, businesses in that industry would have higher premiums for their group insurance.

- Employee benefits are important for attracting and retaining employees in small businesses

- The cost of group benefit plans depends on factors like employee demographics, claims history, and plan details

- Employers can expect to pay anywhere from $25-$300 per month per employee for benefits depending on their plan type

- It's not mandatory to provide health and dental benefits to your employees, but it's an important part of maintaining a healthy workforce