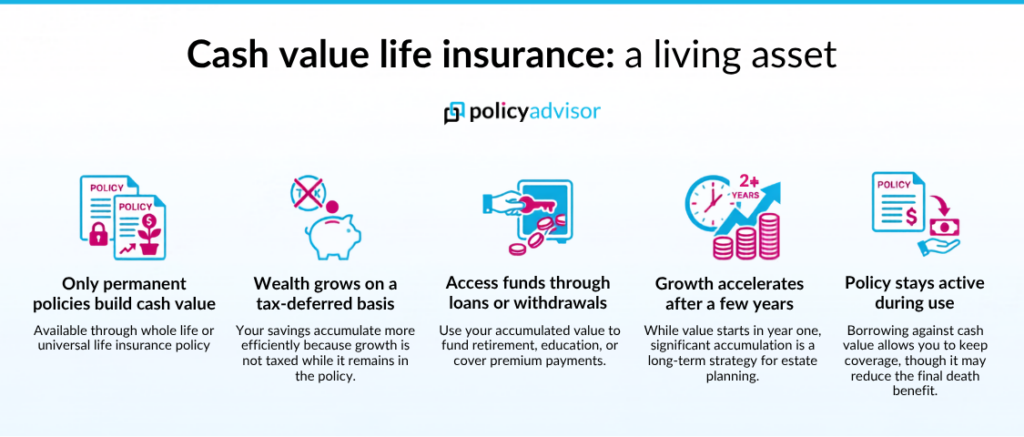

- Permanent life insurance policies, such as whole and universal life insurance, accumulate cash value

- Cash value grows over time on a tax-deferred basis and may increase through dividends or investment returns

- You can access the cash value of life insurance through policy loans, withdrawals, premium payments, or surrendering the policy

- Cash value life insurance is best suited for long-term financial and estate planning rather than short-term savings

Permanent life insurance can do more than provide a death benefit; it can also become a long-term financial asset. Some permanent policies, like cash value life insurance, build cash value that policyholders may access during their lifetimes, making them useful for financial goals such as estate planning, retirement, or wealth preservation.

Quick overview:

- Main types: Whole life and Universal life

- Pros: Provides lifelong coverage and wealth accumulation

- Cons: Can be more expensive than term life insurance

What is the cash value of life insurance?

A cash value life insurance policy is a type of permanent life insurance that provides both lifelong coverage and a built-in savings component. As you pay premiums, a portion goes toward your insurance coverage while the rest accumulates as cash value inside the policy. This cash value grows over time and can be accessed during your lifetime through policy loans, withdrawals, or by surrendering the policy, depending on the terms of your contract.

Not all life insurance policies have cash value. Only permanent policies, such as whole life insurance and universal life insurance, include this feature. The way cash value grows depends on the type of policy you choose. For example, participating whole life policies may increase cash value through dividends, while universal life policies grow based on the performance of the investments you select.

How does cash value life insurance work in Canada?

Let’s understand how cash value life insurance works with an example:

Suppose Sarah, a 35-year-old non-smoking woman, purchases a $500,000 participating whole life insurance policy and pays a $250 monthly premium. Part of each premium covers her lifelong insurance, while the rest builds her policy’s cash value, which grows on a tax-deferred basis and may increase further through insurer dividends.

After 20 years, Sarah could accumulate approximately $60,000 to $90,000 in cash value, depending on the insurer and policy design. She can use this money by borrowing against it, withdrawing it, or using it to help pay future premiums. Any outstanding loans or withdrawals may reduce the death benefit ultimately paid to her beneficiaries.

Disclaimer: The figures shown are for illustrative purposes only. Actual cash values vary by insurer, policy design, and individual circumstances

Which life insurance policies build cash value?

In Canada, only permanent life insurance policies include a cash value feature. These policies provide lifelong coverage while allowing a portion of your premiums to accumulate as cash value over time.

The following types of life insurance can build cash value:

- Whole life insurance: Includes guaranteed cash value that grows steadily over time. Participating whole life policies may also increase cash value through insurer dividends, although dividends are not guaranteed

- Universal life insurance: Combines permanent life insurance with an investment component. Your cash value grows based on the performance of the investment options you choose and their performance, so returns are not guaranteed

How is cash value in life insurance calculated?

The cash value of a life insurance policy is calculated based on how your premiums are allocated, the type of permanent policy you own, how long you have held the policy, and more. The amount of cash value your policy builds depends on several factors, including:

- Policy type: Whole life policies typically offer guaranteed cash value growth, while universal life policies grow based on the performance of the investments you choose

- Premium amount: Higher premiums generally result in faster cash value accumulation

- Policy duration: Cash value grows gradually and typically becomes more substantial after the policy has been in force for several years

- Dividend performance: Participating whole life policies may increase cash value through dividends declared by the insurer, although these are not guaranteed

- Interest or investment returns: Universal life policies earn returns based on the investment options selected, which can affect how quickly the cash value grows

- Policy fees and insurance costs: Administrative fees and the cost of insurance reduce the portion of your premium that goes toward building cash value

How long does it take cash value to build?

The cash value of a participating whole life insurance policy begins accumulating in the first year. However, it typically takes 10 years or more to build a significant amount of cash value. How quickly your cash value grows depends on how the policy is structured. Some policy designs prioritize higher cash value in the early years, while others focus on maximizing long-term growth or estate value.

Cash value growth is not the same for every participating whole life insurance policy. It varies based on the policy’s design and your financial objectives. Some policy designs are structured to build cash value more quickly in the early years, while others prioritize long-term growth or maximizing the tax-free death benefit.

Illustration assumptions:

The illustrative example below is based on a 40-year-old male non-smoker contributing $1,500 per month ($18,000 annually) to a participating whole life insurance policy for 20 years. It compares two policy designs using the same premium to demonstrate how cash value growth can vary depending on the policy structure.

Cash value over time for 2 different strategies

| Policy year | Age | Strategy 1 – Cash value focused | Strategy 2 – Death Benefit / Estate focused |

| 1 | 41 | $11,333 | $496 |

| 5 | 45 | $68,264 | $12,558 |

| 10 | 50 | $186,275 | $108,393 |

| 15 | 55 | $371,006 | $319,837 |

| 20 | 60 | $588,439 | $492,971 |

| 25 | 65 | $771,875 | $680,169 |

| 30 | 70 | $1,000,214 | $920,578 |

| 40 | 80 | $1,622,627 | $1,612,889 |

| 50 | 90 | $2,512,086 | $2,633,954 |

| 60 | 100 | $3,804,984 | $4,147,227 |

Disclaimer: This example is provided for educational and illustrative purposes only. It is not a projection or guarantee of future policy performance. Actual cash values will vary based on factors including the insurer, policy design, dividend scale, premium structure, policy charges, and individual circumstances. Participating policy dividends are not guaranteed and may increase or decrease over time. Consult a licensed insurance advisor for an illustration based on your specific situation.

Why do cash values differ across different whole life strategies?

Cash values can differ significantly between participating whole life insurance policies, even when the premium amount is identical. This is because policies can be structured with different goals and funding strategies. Some policy designs prioritize faster cash value growth, allocating more of the early premiums toward building accessible funds that can support future financial needs. Others focus on maximizing the death benefit, directing more of the premium toward creating a larger estate value from the beginning, which may result in slower cash value accumulation in the early years.

Over the long term, the difference between these strategies may become smaller, and in some cases, a policy designed primarily for estate protection may generate stronger cash value growth over time. The right policy design depends on your financial objectives, whether you prioritize early access to funds, retirement income planning, business succession, or maximizing the tax-free legacy passed on to beneficiaries.

How to borrow from the cash value in life insurance?

There are a few ways to borrow from your life insurance policy’s cash value: you can withdraw money, take a policy loan, use it to pay your premiums, or surrender your policy for its cash surrender value. In each scenario, there are a few things to note.

- Borrow against the cash value: Most permanent life insurance policies allow you to take a policy loan using your cash value as collateral. Since the cash value secures the loan, you typically don’t need a credit check or additional security. Your policy remains active, but interest accrues on the loan, and any unpaid balance, including interest, will reduce the death benefit paid to your beneficiaries

- Withdraw cash value: Some policies let you withdraw a portion of your accumulated cash value without cancelling your coverage. This provides access to funds when needed, but it reduces your policy’s cash value and may also decrease the death benefit

- Use cash value to pay premiums: If your policy has built up enough cash value, you may be able to use it to cover future premium payments. This can reduce your out-of-pocket expenses while keeping the policy in force. However, using cash value for premiums lowers the amount available for future growth and could affect the policy’s long-term value

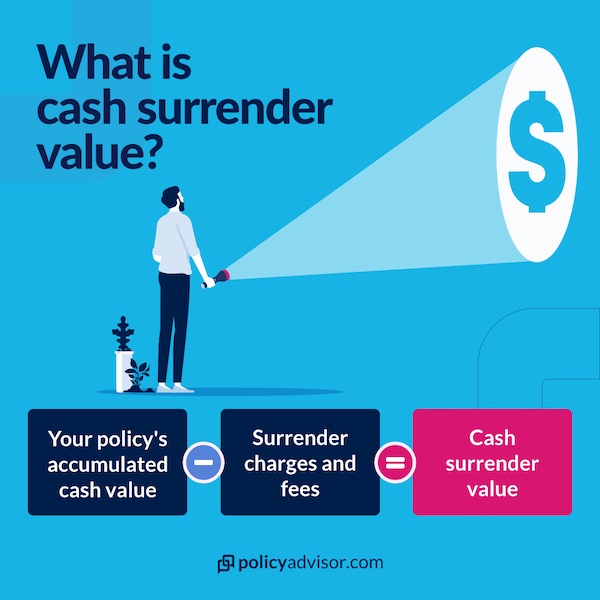

- Surrender your policy: If you no longer need the coverage, you can surrender your policy and receive its cash surrender value. This is the amount remaining after deducting any applicable surrender charges, outstanding policy loans, or fees. Once surrendered, your life insurance coverage ends, and your beneficiaries will no longer receive the death benefit

What happens when you withdraw cash from life insurance?

Withdrawing cash from a permanent life insurance policy gives you access to your accumulated cash value, but it can affect your policy, death benefit, and your taxes.

- Tax implications: Withdrawals up to your policy’s Adjusted Cost Basis (ACB) are generally tax-free. Any amount above the ACB may be treated as taxable income under Canadian tax rules

- Reduced death benefit: Taking money out of your policy typically lowers the cash value and may reduce the death benefit paid to your beneficiaries

- Potential fees: Depending on your insurer and policy terms, you may have to pay withdrawal or surrender charges

- Policy loan considerations: If you borrow against your cash value instead of withdrawing it, the loan is not usually taxable immediately. However, if the policy later lapses with an outstanding loan, the unpaid amount may become taxable

Cash value vs. cash surrender value vs. death benefit

| Feature | Cash value | Cash surrender value | Death benefit |

| What is it? | The savings component that accumulates within a permanent life insurance policy | The amount you receive if you surrender (cancel) your policy | The lump-sum amount paid to your beneficiaries after your death |

| Who receives it? | The policy owner | The policy owner | The policy’s beneficiaries |

| When is it available? | While the policy is active | Only when the policy is surrendered | After the insured person’s death |

| How is it calculated? | Builds over time from premiums, dividends, or investment returns, depending on the policy | Cash value minus any surrender charges, fees, and outstanding policy loans | Determined by the policy’s coverage amount and may be reduced by unpaid policy loans or withdrawals |

| Does the policy remain active? | Yes | No, surrendering the policy permanently ends the coverage | Not applicable, as the policy ends after the death benefit is paid |

| Can it change over time? | Yes, it generally grows over time, depending on the policy | Yes, it changes as the cash value and deductions change | Generally remains the same unless affected by policy loans, withdrawals, or dividend options |

What are the benefits of cash value life insurance?

Cash value life insurance offers a unique blend of lifelong coverage and financial flexibility, along with other benefits like access to cash value, guaranteed savings growth, and estate planning advantages, making it a valuable financial planning tool for Canadians.

- Lifelong coverage: Unlike term life insurance, cash value life insurance protects your entire life as long as premiums are paid, ensuring your loved ones receive a guaranteed death benefit

- Tax-deferred growth: The cash value component grows on a tax-deferred basis, allowing your savings to accumulate more efficiently over time. This is especially beneficial for Canadians looking to build long-term wealth

- Access to cash value: Policyholders can access the cash value through loans or withdrawals. These funds can be used for various purposes, such as funding education, supplementing retirement income, or covering emergencies

- Financial flexibility: The ability to borrow against your policy or use the cash value to pay premiums provides financial flexibility during times of need or as part of retirement planning

- Estate planning advantages: The death benefit is generally paid out tax-free to beneficiaries, making it an effective tool for estate planning and ensuring a financial legacy

What are the disadvantages of cash value life insurance?

Some of the disadvantages of cash value life insurance include:

- Permanent life insurance costs significantly more than term life insurance

- It can take some years before the policy builds meaningful cash value

- Accessing cash value through withdrawals and policy loans can lower your cash value and death benefit

- Cash value policies have more features and fees than basic term life insurance, making them more complex to understand and manage

Common myths about cash value life insurance

Common myths about cash value life insurance include that it grows quickly, does not affect the death benefit, and is guaranteed, among others.

| Myth | Reality |

| All life insurance policies build cash value | Only permanent life insurance policies, such as whole life and universal life insurance, accumulate cash value |

| Cash value grows quickly | Cash value typically builds gradually and is intended as a long-term savings feature |

| You can withdraw cash without affecting your policy | Withdrawals and policy loans can reduce your cash value and may lower the death benefit |

| Cash value is always guaranteed | Guaranteed cash value is available in many whole life policies, but dividends and investment returns are not guaranteed |

Is a life insurance policy with cash value right for you?

Deciding which life insurance policy is best depends on your family’s financial goals. Permanent life insurance policies with cash value options do come at a higher premium cost compared to term life insurance plans, but they can be extremely beneficial for those looking for a guaranteed death benefit with the bonus of investment opportunities.

Book a call with one of our licensed life insurance advisors at PolicyAdvisor today and get the right policy. We work with over 30 of Canada’s best life insurance companies and can help you to make sure you get the policy that’s right for you. Schedule a call now!

Frequently asked questions

Can you use the cash value as collateral for a loan in Canada?

Yes, the cash value of a life insurance policy can be used as collateral for a loan in Canada. This is often referred to as a collateral assignment. Many lenders accept the cash value as security, allowing you to access funds without surrendering the policy. The loan amount typically depends on the cash value available. Using cash value as collateral lets you retain the policy benefits, but it is important to ensure loan repayment to avoid affecting the policy’s death benefit.

What happens to unused cash value in participating whole life insurance?

In participating whole life insurance, unused cash value remains within the policy and continues to grow on a tax-deferred basis. At the policyholder’s death, the cash value is not typically paid out in addition to the death benefit. Instead, the insurer retains it, and only the death benefit is provided to beneficiaries. However, dividends earned on the policy can increase the death benefit or cash value, depending on the dividend option chosen by the policyholder during their lifetime.

Can I cash out my life insurance policy in Canada?

Yes, you can cash out a permanent life insurance policy if it has accumulated cash value. You can either make a partial withdrawal, borrow against the cash value, or surrender the policy for its cash surrender value. Keep in mind that surrendering your policy ends your life insurance coverage, and withdrawals or loans may reduce your death benefit.

How long does it take to build cash value in life insurance?

Cash value begins accumulating from the first year of most permanent life insurance policies, but it generally takes 10 years or more to build a significant amount. Growth depends on factors such as the policy type, premium amount, dividend performance, and how long the policy has been in force.

Do beneficiaries receive both the cash value and the death benefit?

No, beneficiaries will not receive both the cash value and death benefit. In most Canadian permanent life insurance policies, beneficiaries receive the death benefit, not the policy’s accumulated cash value in addition to it. The cash value is generally used by the insurer to help fund the death benefit unless your policy specifically provides otherwise.

Is cash value life insurance taxable in Canada?

The growth of cash value inside a permanent life insurance policy is generally tax-deferred. However, withdrawals exceeding the policy’s Adjusted Cost Basis (ACB) may be taxable. If you surrender your policy, any gain above the ACB may also be subject to tax. Because tax treatment depends on your policy and individual circumstances, consider speaking with a licensed insurance advisor or tax professional before accessing your policy’s cash value.

Cash value life insurance combines lifelong insurance coverage with a built-in savings component that grows over time. Available only with permanent life insurance policies such as whole life and universal life insurance, it can help you build tax-deferred wealth while providing financial protection for your loved ones. Depending on your policy, you can access the accumulated cash value through loans, withdrawals, premium payments, or by surrendering the policy, making it a valuable tool for long-term financial and estate planning.