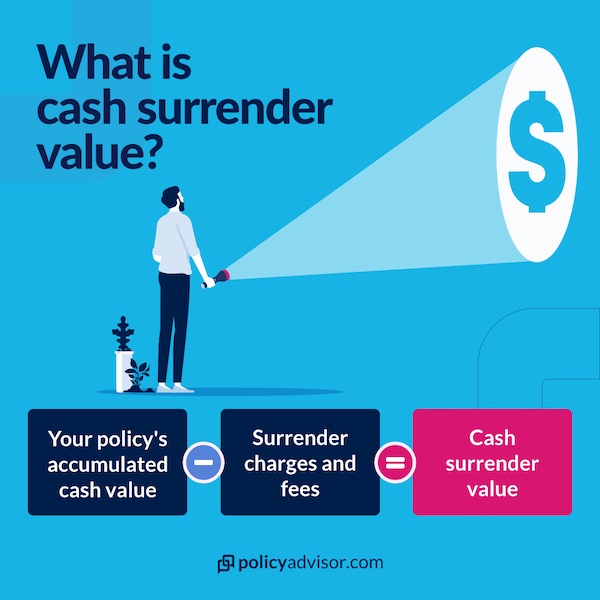

- Cash surrender value = cash value - applicable fees

- Only permanent life insurance policies have a cash value component—it does not apply to term insurance

- If you experience a capital gain by accessing your cash value, it may be taxed

- Some insurers allow you to access your cash value right away

Cash surrender value is the dollar amount you receive after cancelling a permanent insurance policy, minus any applicable fees. You can also withdraw all or part of this amount while keeping your insurance intact.

While we’re in the business of providing policies, and generally not cancelling them, there are circumstances where cancelling your policy and utilizing your cash surrender value may be beneficial to you.

At PolicyAdvisor, we want to make sure you hit your financial goals, both short-term and long-term. Utilizing your cash surrender value may be attractive when you’re short on cash, but it’s important you understand all the terms and conditions when doing so. This article explains how cash surrender values work and provides examples to illustrate its functions.

Cash surrender value is the dollar amount you receive after cancelling a permanent insurance policy, minus any applicable fees. You can also withdraw all or part of this amount while keeping your insurance intact.

While we’re in the business of providing policies, and generally not cancelling them, there are circumstances where cancelling your policy and utilizing your cash surrender value may be beneficial to you.

At PolicyAdvisor, we want to make sure you hit your financial goals, both short-term and long-term. Utilizing your cash surrender value may be attractive when you’re short on cash, but it’s important you understand all the terms and conditions when doing so. This article explains how cash surrender values work and provides examples to illustrate its functions.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What is cash surrender value?

Over time, permanent life insurance policies accumulate a cash value. Cash surrender value is your cash value minus any surrender charges or fees. Others might describe cash surrender value as an amount you receive when you cancel your insurance. Although this is an accurate description, cancelling your policy isn’t mandatory to access your policy’s cash surrender value.

The surrender fee is present because insurance companies don’t want policyholders to cancel their insurance and stop paying premiums. It’s also a deterrent for early withdrawals. In some cases, these surrender fees can be a few hundred dollars. Your surrender fee may also change over time. In fact, it’s common for surrender fees to hit zero after ten to fifteen years of a policy’s life.

Accumulating cash value comes in many forms. Some policies guarantee cash value throughout the policy’s lifetime. Others may invest the money, and the cash value then depends on the well-being of select investments. You may even have the option to choose where to invest the cash value, such as universal life insurance.

Factors such as active years and total premiums paid to date also influence your cash value. Ultimately, it’s vital to understand the contract between you and your insurer to learn how your policy’s cash value will grow over the years.

It’s important to note that your cash surrender value doesn’t necessarily equal your policy’s death benefit. Withdrawing the cash value from the policy, however, usually decreases the death payout.

Why cash surrender value is important

The obvious fact is that you can withdraw the cash surrender value from your insurance policy. But a policy’s cash surrender value also has important implications for corporate-owned life insurance, loans, and premium payments.

Corporations often purchase life insurance policies with a cash surrender value to facilitate transactions and structures like insurance-tracking shares or buy-sell agreements.

It’s vital for corporations to understand the cash surrender values of any policies it owns. If a corporation owns a whole life policy, for example, the whole life insurance’s cash surrender value contributes to the business’s fair market value. This can result in significant tax complications.

Furthermore, a policy with a cash surrender value has inherent monetary worth. As a result, lenders are open to accepting such a life insurance policy as collateral on a loan.

A lender, like a major Canadian bank or even your insurance company, usually provides a loan based on 50-90% of the cash surrender value. Where this percentage lands depends on factors like your credit score.

If you don’t or cannot make premium payments, your insurer may leverage your policy’s cash surrender value to compensate for the unpaid premium. Generally, insurance companies take a loan backed by your policy to cover the payments. You’ll be responsible for any interest that these loans accrue.

Similarly, you could convert your policy into a reduced paid-up insurance policy. This means you’re insured at a lower amount but will no longer have to make premium payments because it’s taken care of by your cash surrender value.

Another way to see it is that you’re taking your policy’s cash surrender value to purchase a fully paid-up (i.e., you won’t have to make further premium payments to maintain the benefit) life insurance policy.

What type of life insurance has cash value?

Cash surrender values are available for permanent life insurance plans such as whole life insurance or universal life insurance. Permanent life policies contrast term-life policies, which only provide a death benefit if you pass away during a particular period. Permanent policies provide lifetime coverage and pay a death benefit as long as you maintain the premiums. They also have some living benefits, like accessing cash value.

Only permanent life insurance policies contain a savings or investment portion to them. Term policies do not.

Whole life insurance and universal life insurance also have their differences. Whole life coverage covers your entire life on a fixed premium. Premiums won’t change as you grow older, change occupations, or find new hobbies. Part of these payments also go into a savings or investment account to accumulate and grow tax-free.

Universal life insurance also covers you for your entire life and similarly puts part of your premiums into a savings or investment account to accumulate and grow tax-free. The difference is a universal policy offers flexibility in premium payments. You can choose to pay a minimum amount or increase your payments to boost the cash value.

Read more about the difference between whole vs. universal life insurance.

Cash value versus surrender value: What’s the difference?

Cash value is the accumulation of a portion of your permanent life insurance premiums that are redirected towards a savings or investment component. This money accumulates on a tax-deferred basis. You’re also able to access this cash value as the policyholder.

Cash surrender value is similar and is part of every policy with a cash value. Essentially, when you cancel a permanent life insurance policy or withdraw the cash value, there’s a surrender charge or fee. The cash surrender value is what you would receive upon cancelling your policy or making a withdrawal after the surrender charges.

Example of cash value versus surrender value

Suppose the following terms were part of a universal life insurance policy:

- Monthly premium of $100 ($1,200 per year);

- 30% of premium goes towards the cash value;

- A surrender fee of $300; and,

- Current cash value of $3,500.

The policy’s current cash value of $3,500 is the amount built over time by the accumulation of 30% of the premiums. It may have further grown if your insurance company invested the money and said investments performed well over time.

Suppose you want to withdraw this money or cancel the policy at this very moment. This action requires paying the $300 surrender fee. As a result, you’d receive $3,200, the difference between the policy’s cash value and the surrender charge. This $3,200 is your cash surrender value.

When can I withdraw my policy’s cash surrender value?

The limitations to withdrawing your cash surrender value are usually only limited to your policy’s terms and conditions. Some policies let you withdraw the cash at any time, while others won’t let you withdraw it at all. Alternatively, you could just cancel your life insurance to access the cash surrender value, but this would mean you forgo life insurance protection.

How to access cash without surrendering your policy

There are multiple ways to access your cash surrender value without breaking your policy.

The easiest way is to withdraw the money through your insurer. However, this only works if your policy allows you to make such a withdrawal. Some policies also allow you to withdraw some or all of your cash value, for a fee. Your policy’s cash value minus the surrender fees is what your “cash surrender value” will be. In some cases, this penalty can be a few hundred dollars, but in other cases, it may be a percentage based on the cash value accumulated. With policy withdrawals, the loan is final and cannot be repaid—whatever you take will reduce your death benefit. This is an option for you if you’re short on cash, but may wipe out your death benefit altogether depending on the withdrawal.

An insurance policy loan or reduced paid-up insurance policy are also ways to access the cash surrender value. An insurance policy loan or collateral loan allows you to borrow against a cash surrender value through your insurer or a third-party lender.

An insurance policy loan usually refers to an insurer loan, while a collateral loan usually refers to a third-party loan. Each may have unique tax considerations depending on your circumstances.

On the other hand, reduced paid-up insurance allows you to maintain a death benefit from the policy (albeit a reduced one) without making further premium payments. You could also forward your cash surrender value to pay for a term life insurance policy. This is commonly referred to as extended term insurance.

Do you have to pay tax on cash surrender value?

The taxation of cash surrender values is complex. It’s ideal to speak with a tax expert or insurance advisor to learn more. However, upon a policy withdrawal, you may be taxed on any gains made by the accumulated dollars.

For example, suppose a total of $1,000 of your premium payments went to the policy’s savings or investment account. This $1,000 is referred to as the Adjusted Cost Base (ACB). But because the investments grow or the savings account accumulates interest, your total cash surrender value is $1,500. (Additionally, let’s pretend the surrender fee is zero here.)

Now, suppose you withdraw the $1,500. This $1,500 is your Proceeds of Disposition (PD). When you withdraw the money, you’re taxed on any gains, which is the difference between your PD and ACB. In this example, you’re taxed on $500 as a capital gain.

But let’s say your investments on the initial $1,000 didn’t do too well. As a result, when you withdraw your cash surrender value, the PD is $900. Because the difference between the PD and ACB is negative, there’s no taxable gain. Your withdrawal is, therefore, likely not taxed.

Instead of withdrawing the cash surrender value, many policyholders leave it as part of their death benefit. This move has significant tax advantages as death benefits are usually paid tax-free to beneficiaries. This tax advantage is why many insurers promote their policies as an estate planning tool.

If you’re looking for a permanent life insurance policy, reach out to one of our expert advisors today. Book some time with us below, and we can discuss your insurance needs and provide you with a no-obligation quote.

The information above is intended for informational purposes only and is based on PolicyAdvisor’s own views, which are subject to change without notice. This content is not intended and should not be construed to constitute financial or legal advice. PolicyAdvisor accepts no responsibility for the outcome of people choosing to act on the information contained on this website. PolicyAdvisor makes every effort to include updated, accurate information. The above content may not include all terms, conditions, limitations, exclusions, termination, and other provisions of the policies described, some of which may be material to the policy selection. Please refer to the actual policy documents for complete details. In case of any discrepancy, the language in the actual policy documents will prevail. All rights reserved.

If something in this article needs to be corrected, updated, or removed, let us know. Email editorial@policyadvisor.com.

Permanent life insurance policies accumulate a cash value. A cash surrender value is the original cash value, minus any applicable charges and fees. You can access a policy’s cash surrender value after cancellation or while keeping the policy in force, depending on the terms and conditions of your policy.