- Life insurance financially protects your beneficiaries in case of your death.

- Life insurance is also a core financial tool one can use to plan their estate.

- The death benefit can be used to settle estate taxes on capital gains from property or business sales, as well as protect retirement savings.

- Whole life insurance is commonly chosen for estate planning as the coverage lasts until death.

You may purchase life insurance to protect your family’s well-being in case of your death. But life insurance is also a core aspect of planning your estate.

This article discusses the benefits of incorporating life insurance into your estate planning and how different life insurance policies can accommodate your estate planning needs.

What is estate planning?

Estate planning is the process of organizing your assets and determining how they will be managed and distributed during your lifetime and after your death.

In Canada, estate planning typically involves drafting legal documents like a will, trust, and power of attorney. It also includes making decisions about tax planning, charitable giving, and appointing guardians for minor children.

Life insurance plays a crucial role in estate planning, as it can provide liquidity to cover expenses like taxes, debts, and probate fees, ensuring your heirs receive their inheritance without financial burdens.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

Why do Canadians plan their estates?

How life insurance payouts work in estate planning

If you pass away with an active life insurance policy, your beneficiaries (such as surviving family members) receive a tax-free cash payout from your insurance company. This payout is not considered part of your income or your beneficiaries’ incomes and is not taxed as such when you pass. This is because you paid your life insurance premiums using funds on which you paid income tax as well.

The insurance provider ensures that payouts go directly to your beneficiaries. The payout bypasses your estate and the probate process. As a result, if you have outstanding debts at your death, creditors can’t access this death benefit unless the payout goes to your estate.

Further, because your life insurance benefit skips the estate process, the payout is free from probate fees — also known as estate administration tax.

Naming beneficiaries vs. Leaving the payout to the estate

When it comes to estate planning, you can either name specific beneficiaries on your life insurance policy or leave the payout to your estate:

Naming beneficiaries: By naming individuals (such as family members or charities) as beneficiaries, the payout bypasses probate and goes directly to them. This results in faster access to funds and avoids probate fees, preserving the full value of the payout. It also provides privacy since the transfer is not subject to public records.

Leaving the payout to the Estate: If the payout is left to your estate, it becomes part of your overall assets and may be subject to probate. While this allows for a more comprehensive estate distribution plan, it can delay access to the funds and incur probate fees. Additionally, creditors may claim a portion of the payout to settle outstanding debts.

Can a life insurance death benefit pay for estate taxes?

Yes, a life insurance benefit can help pay or fully cover estate taxes. Estate taxes can be a large financial burden on your loved ones and an unexpected expense if you suddenly pass away. When you die, there are common estate taxes that come in the form of capital gains. A capital gain occurs when you sell an asset, such as your cottage, for more than the purchase price. The difference between your purchase price and the sale price is the capital gain. In Canada, 50% of the capital gain is taxable at your highest marginal tax rate.

So, if you purchased a cottage for $100,000 and sold it for $150,000, you would have a capital gain of $50,000. Half of that amount, $25,000, is then added to your taxable income for the year.

How do capital gains on properties work?

When you pass away, Canadian tax laws consider your assets to have gone through a deemed disposition. A deemed disposition assumes that, for tax purposes, your assets are “sold”, and a capital gain is triggered. An exception is if the beneficiary of your assets is your spouse. In this instance, there’s a “rollover” that allows your spouse to receive the assets without paying capital gains tax.

But, if your children or other family members receive your assets as part of your will, a tax consequence will likely arise. With the value of real estate properties appreciating so much over the past decade, a deemed disposition of the family cottage or rental properties could mean a significant capital gain and a significant capital gains tax.

If your family doesn’t have enough cash to pay the capital gains tax at the time of your death, the situation could force them to sell the cottage or other assets.

However, life insurance proceeds can provide an immediate source of liquid cash upon your death to pay these taxes. It’s common for individuals to purchase life insurance so that their beneficiaries can prevent a forced sale of cherished assets, like the family cottage.

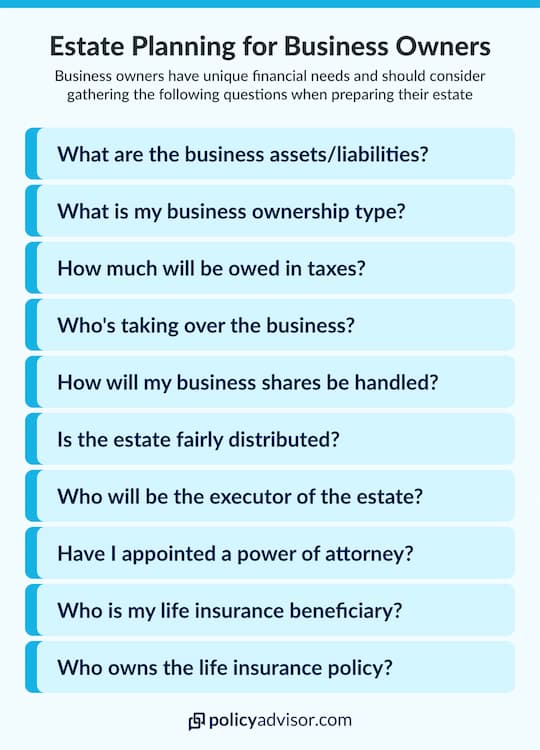

How do capital gains on a family business work?

If you own a business, the value of its assets may have increased over its years of operation. This can create a tax consequence when you die.

When you die, there’s a deemed disposition of your business’ assets, which can create a massive tax bill for your beneficiaries. Like the capital gains of your cottage, your beneficiaries may have to sell the business to pay the affiliated taxes. A death benefit could help provide cash to remedy the situation.

An alternative is to implement an estate freeze, which can “freeze” the value of your business’ assets for tax purposes and defer the tax payable to the next generation or whenever your family chooses to sell the business. However, estate freezes are a complicated area of tax law and require expert lawyers and accountants, which can cost a lot of money.

How is a Registered Retirement Savings Plan (RRSP) taxed at death?

At death, the full amount of your RRSP or Registered Retirement Investment Fund (RRIF) is added to your final year’s income and is taxed as such. This can create a significant tax liability for your estate unless your situation qualifies for the exception.

As previously mentioned, if neither your beneficiaries nor estate has enough cash to pay estate taxes and fees, it may mean selling the assets in your RRSP or RRIF. Although selling RRSP/RRIF assets might not have the same emotional ramifications as selling the family cottage or business, it may not be preferable to sell if there’s a market downturn. Having cash on hand, such as that from a death benefit, can prevent the need to sell RRSP/RRIF assets at a less-than-ideal time.

What end-of-life expenses can life insurance cover?

Life insurance can cover your funeral costs, outstanding debts, and financial goals.

The average Canadian burial costs between $5,000 and $10,000 while the average Canadian cremation costs $2,000 to $5,000. If your estate doesn’t have enough money to pay for your funeral, it can leave your surviving family members with a hefty bill. To ensure that your family won’t have novel financial stresses in addition to the emotional stress of your death, a life insurance policy can be there to pay for your funeral costs.

A death benefit can also cover outstanding debts, such as a line of credit or mortgage, so your family won’t need to worry about these either. Alternatively, it can help surviving family members reach financial goals such as saving for post-secondary education or buying their first home.

What type of life insurance is best for estate planning?

The best type of policy for estate planning depends on your needs and budget. Both term and whole life insurance provide payouts when you die. But whole life insurance (or a permanent life insurance policy) is often more effective in estate planning because the policy lasts for your whole life.

Term life insurance only lasts for a particular term (10 years, 20 years, etc). Therefore, term insurance would only work as an estate planning tool if you die within that time period.

Term life insurance may be more affordable than whole life insurance, especially when you’re young. But if you pass away after the term expires, your family still has to deal with costs associated with your death with whatever’s left in the estate.

This could force them to sell the family cottage or pay your funeral expenses themselves. This isn’t an issue with permanent insurance because the “term” essentially lasts as long as you pay the premium.

Other policies, like a universal life policy, are not well suited for estate planning and are more so a wealth-building tool as it requires constant monitoring and offers uncertain returns.

Term life insurance vs. permanent life insurance for estate planning

Term life insurance provides temporary coverage, ideal for covering debts or income replacement during key financial years. However, it’s less suited for estate planning due to its limited duration.

Permanent life insurance, such as whole or universal life, offers lifelong coverage, ensuring a guaranteed payout to support estate goals, cover taxes, and provide inheritances.

Suitability of whole life insurance and universal life insurance for Canadian estate planning

Whole life insurance is well-suited for estate planning, offering a guaranteed death benefit and cash value growth, which can fund trusts or cover estate taxes.

Universal life insurance provides flexible premiums and investment options, making it ideal for those who want control over coverage and savings. Both ensure a tax-free payout, preserving wealth for heirs.

Why is life insurance good for estate planning?

Life insurance is beneficial for estate planning because it provides a tax-free, guaranteed payout that can cover final expenses, pay off debts, and minimize the financial burden on loved ones.

It helps preserve the estate’s value by providing immediate liquidity, ensuring heirs receive their intended inheritances without having to sell assets.

Additionally, life insurance can offset taxes, such as capital gains and probate fees, ensuring more wealth is passed on to beneficiaries. It also offers flexibility in structuring trusts or funding charitable bequests, making it a versatile tool for achieving estate planning goals.

Common mistakes to avoid when using life insurance for estate planning

When using life insurance for estate planning, avoid common mistakes like not updating beneficiaries after major life events, which can lead to unintended recipients.

Overlooking probate fees by naming the estate as a beneficiary can increase costs and delays. Also, underestimating coverage needs may leave your heirs with insufficient funds to cover taxes or debts. Regular updates and careful planning are key.

How to choose the right life insurance for your estate plan?

Choosing the right life insurance for your estate plan is essential for protecting your assets and ensuring that your loved ones are financially secure.

To make an informed decision, you need to assess your financial goals, understand the tax laws and estate planning regulations in Canada, and consider speaking with a licensed insurance advisor to help align your policy with your financial goals.

Frequently asked questions

Is life insurance considered part of an estate in Canada?

In Canada, whether life insurance is considered part of your estate depends on how you have structured the policy. If you name a beneficiary, the death benefit is paid directly to them and is not included in your estate. However, if you name the estate as the beneficiary, the payout will become part of your estate, which may be subject to probate and taxes. Therefore, naming a direct beneficiary can help avoid including the payout in the estate.

Can life insurance avoid probate in Canada?

Yes, life insurance can avoid probate in Canada if you name a specific beneficiary for the policy. By designating a beneficiary, the life insurance payout goes directly to them without having to go through the probate process, which can be time-consuming and costly. This ensures your beneficiaries receive their benefits promptly and in full.

What happens if I outlive my life insurance policy?

If you outlive your term life insurance policy, the coverage simply ends at the conclusion of the term, and there is no payout. In the case of permanent life insurance, such as whole or universal life, the policy remains in force as long as premiums are paid, and you can receive the cash value accumulated during the policy’s life. However, some term policies may offer renewal or conversion options to extend coverage or switch to permanent life insurance.

How do I set up a trust for my life insurance in Canada?

To set up a trust for your life insurance in Canada, you’ll need to work with an estate planning lawyer to establish a formal trust. You can designate the trust as the beneficiary of your life insurance policy, ensuring the payout is distributed according to your instructions. The trustee you choose will manage the funds and distribute them as per your wishes, which can provide greater control over how the benefits are used, particularly for minors or those who need ongoing financial management.

What are the tax implications for life insurance beneficiaries in Canada?

In Canada, life insurance proceeds paid to beneficiaries are generally tax-free, meaning they are not subject to income tax. However, if the estate is named as the beneficiary, the payout may be included in the estate and could be subject to probate fees or taxes, such as capital gains tax.

Life insurance also plays a vital role in estate planning. Protecting your family’s finances is an important part of life insurance; but, it’s only part of the story. Death benefits can be used strategically, being passed down to family members to build wealth, as well as to cover expenses like funerals, estate taxes and capital gains.