- Seniors in Canada can qualify for term, whole life, or no medical life insurance, depending on their age and health

- Buying life insurance earlier in retirement can help secure lower premiums and more coverage options

- Seniors with pre-existing medical conditions may still qualify through simplified issue or guaranteed issue policies

- Whole life insurance is a great option for seniors who either own businesses or are looking to protect their estate

Life insurance for seniors in Canada is available to adults aged 60 and older, including retirees and those with certain pre-existing health conditions. Depending on your age, health, and financial goals, you can choose from term life insurance, whole life, simplified issue, or guaranteed issue policies. In Canada, many insurers, including Sun Life, Canada Life, iA, and RBC Insurance, offer life insurance policies.

Quick summary:

| Eligibility | Widely available for ages 60 and above |

| Policy options | Choose from term life, whole life, simplified issue, or no medical life insurance |

| Medical exam | Not always required. Many guaranteed issue policies ask zero health questions |

| Best companies for seniors | Canada Life, Wawanesa, iA, Canada Protection Plan, and Manulife |

| Benefits | Helps cover final expenses, debts, income replacement, or estate planning needs |

Can seniors get life insurance in Canada?

Yes. Most Canadian seniors can still buy life insurance, including options that do not require a medical exam, although choices and costs depend strongly on age and health. Healthy seniors may qualify for fully underwritten term or whole life insurance, which often provides lower premiums, higher coverage amounts and more policy options than no medical life insurance.

Seniors with pre-existing medical conditions may be better suited to simplified issue or guaranteed issue life insurance that requires minimal to no medical questionnaires. Although premiums are generally higher for older applicants, guaranteed issue coverage allows many seniors with serious medical conditions to obtain life insurance without being declined.

Life insurance options for seniors in Canada

Seniors in Canada can choose from term life insurance, whole life insurance, or no medical life insurance. Here are the most common life insurance options available to Canadian seniors.

Term life insurance for seniors

- Overview: Term life insurance provides coverage for a fixed period, typically 10, 20, or 30 years. If you pass away during the policy term, your beneficiaries receive a tax-free death benefit. Since it offers temporary coverage, premiums are generally lower than those for permanent life insurance

- Best for: Healthy seniors who need affordable coverage for a specific period, such as paying off a mortgage, replacing income for a spouse, or covering outstanding debts

- Things to consider:

- Typically, the most affordable life insurance option

- Coverage ends when the policy term expires

- May be renewable or convertible, depending on the insurer

- Available term lengths become more limited with age, as most term life insurance policies only provide coverage until around age 85

Whole life insurance for seniors

- Overview: Whole life insurance provides permanent coverage that lasts for your lifetime, provided premiums are paid. It also builds guaranteed cash value over time, which can be borrowed against or accessed under certain conditions. It is a good option for those looking for lifelong financial protection, estate planning benefits, or coverage for final expenses.

- Best for: Seniors who want lifelong coverage, estate planning benefits, or to leave a guaranteed inheritance for loved ones

- Things to consider:

- Provides lifelong protection

- Includes guaranteed cash value growth

- Premiums are generally higher than term life insurance

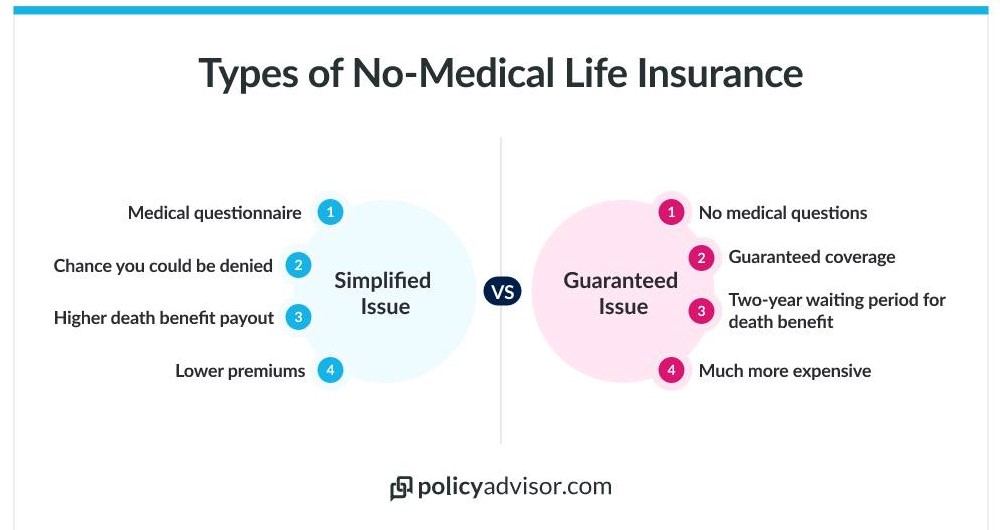

No medical life insurance for seniors

- Overview: No medical life insurance allows seniors to apply for coverage without completing a medical examination. Depending on the insurer and your health, you may qualify for either simplified issue life insurance, which requires a few health questions, or guaranteed issue life insurance. Simplified issue policies require a few health questions, while guaranteed issue policies generally require neither a medical exam nor health questions

- Best for: Canadian seniors who want life insurance without undergoing a medical exam or those with pre-existing health conditions

- Things to consider:

- Approval is generally faster than fully underwritten life insurance

- Available as simplified issue or guaranteed issue coverage

- Premiums are typically higher, and coverage amounts may be lower than fully underwritten life insurance

- Simplified issue life insurance often offers coverage of up to around $500,000, while guaranteed issue life insurance is usually capped at about $50,000

- Guaranteed issue policies typically include a two-year waiting period before the full death benefit is paid for non-accidental deaths, while simplified issue policies may offer immediate coverage depending on the insurer

What happens if seniors have pre-existing medical conditions?

Having a pre-existing medical condition doesn’t automatically prevent Canadian seniors from getting life insurance. Many insurers offer coverage to applicants with conditions such as diabetes, high blood pressure, heart disease, or a history of cancer, although eligibility, premiums, and coverage options may depend on the type and severity of your condition, your overall health and the insurer’s underwriting requirements.

If you have a pre-existing condition, you may qualify for one of the following options:

- Simplified issue life insurance: Requires a short health questionnaire but no medical exam, making it suitable for seniors with minor or well-managed medical conditions. For example, applicants with controlled Type 2 diabetes or well-managed high blood pressure may still qualify for simplified issue coverage or even traditional life insurance with some insurers. Coverage amounts are generally higher than guaranteed issue policies, but premiums may be higher than fully underwritten plans

- Guaranteed issue life insurance: Requires neither a medical exam nor health questions and is designed for seniors with serious or multiple health conditions who may not qualify for other types of coverage. These policies typically have lower coverage limits (often up to $50,000), higher premiums, and usually include a two-year waiting period before the full death benefit is payable for non-accidental deaths

How much does life insurance for seniors cost in Canada?

The cost of life insurance for seniors can range from approximately $98 to $2070 per month, based on a $250,000 policy. However, the exact cost will vary based on your age, health, coverage amount, smoking status, and the type of policy you choose.

Cost of life insurance for seniors over 60 in Canada

Seniors over 60 can typically qualify for term life insurance, whole life insurance, and no-medical life insurance, provided they meet the insurer’s eligibility requirements. Applicants in good health generally have access to more policy options, higher coverage amounts, and lower premiums than those applying later in life.

The monthly cost of life insurance for seniors over 60 in Canada can range from about $98 for a 10-year term policy to around $320 for a no-medical life insurance policy, for a sample $250,000 policy. Applying in your early 60s can help you lock in lower premiums before age-related health risks begin to significantly affect pricing.

Cost of life insurance for seniors over 70 in Canada

Life insurance remains available for seniors over 70 in Canada, although policy choices may become more limited depending on the insurer and your health. While some insurers continue to offer term life insurance, many applicants in this age group choose whole life or no-medical life insurance for lifelong coverage and simplified eligibility.

For a $250,000 policy, monthly premiums for seniors over 70 generally range from about $293 for a 10-year term policy to approximately $1,088 for a no-medical life insurance policy. If you have well-managed health conditions, you may still qualify for fully underwritten coverage, which can offer better rates than no-medical policies.

Cost of life insurance for seniors over 80 in Canada

Seniors over 80 can still purchase life insurance through select Canadian insurers, although eligibility, coverage amounts, and policy types are typically more limited. At this age, whole life insurance and guaranteed issue life insurance are often the most widely available options, while new term life policies are generally available with select insurers.

The cost of a 20-pay non-participating whole life insurance policy for an 80-year-old starts at approximately $2,070 per month for $250,000 of coverage. Because premiums are significantly higher at this age, many seniors choose lower coverage amounts to help cover funeral expenses, estate settlement costs, or leave a tax-free benefit for their beneficiaries.

Life insurance cost for seniors in Canada (2026)

| Age | 10-year Term Life Insurance | 20-Pay Non-Participating Whole Life Insurance | 20-year Term Simplified Issue Life Insurance |

| 60 | $98.33 | $765.45 | $319.73 |

| 65 | $173.03 | $950.97 | $573.30 |

| 70 | $293.40 | $1,192.75 | $1,087.65 |

| 75 | $557.33 | $1,525.53 | — |

| 80 | $931.30 | $2,070.90 | — |

Disclaimer: Sample monthly premiums shown are based on a $250,000 life insurance policy.Actual premiums may vary based on your age, health, smoking status, coverage amount, policy type, and the insurer’s underwriting criteria

How much does $250,000 of life insurance cost for a 70‑year‑old in Canada?

The cost of a $250,000 life insurance policy for a 70-year-old in Canada depends on the type of policy you choose and your health. Based on our sample rates, a 10-year term policy starts at approximately $293 per month, a 20-pay whole life policy costs around $1,193 per month, and a 20-year no-medical life insurance policy starts at about $1,088 per month.

How much does Life Insurance cost?

Get instant quotes from Canada's top life insurance providers and find the perfect coverage for your family.

Powered by

![]()

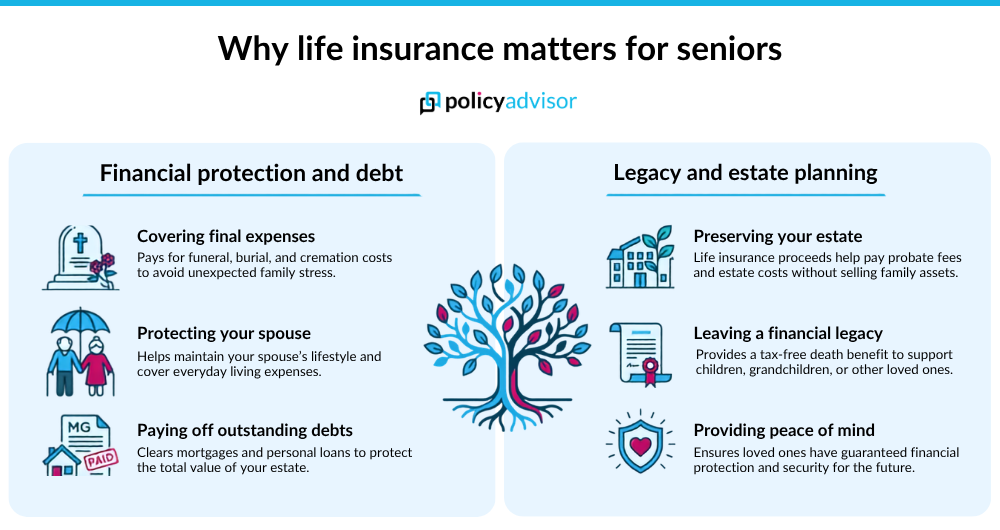

Is life insurance worth it for seniors?

Yes, life insurance can be worth it for many seniors in Canada who want to protect their loved ones from financial burdens after they pass away. It can help cover final expenses, outstanding debts, probate fees, estate settlement costs, and provide financial support to a spouse or other dependents.

Some of the key benefits of life insurance for seniors include:

- Covering final expenses: The average traditional funeral and burial in Canada costs between $8,000 and $15,000. The Canada Pension Plan (CPP) death benefit is a flat $2,500, leaving a massive shortfall that life insurance can cover immediately

- Protecting your spouse: Provides financial support to help replace lost retirement income and cover everyday living expenses after your passing

- Preserving your estate: Helps beneficiaries pay estate settlement costs, probate fees, and other settlement costs without having to sell family assets or investments

- Leaving a financial legacy: Provides a tax-free death benefit that can help support children, grandchildren, or other loved ones in the future

- Paying off outstanding debts: Covers remaining mortgages, personal loans, credit card balances, or other financial obligations that could reduce the value of your estate

- Providing seniors with peace of mind: Ensures loved ones have financial protection and won’t face unexpected expenses after the policyholder passes away

Is a senior’s life insurance policy a costly mistake?

No, the cost of life insurance for seniors is not a costly mistake, given its benefits. When you consider how the death benefit can be used to pay off debts, cover final expenses, and protect your estate, life insurance becomes a valuable investment rather than a costly mistake.

While premiums generally increase with age, life insurance can provide valuable financial protection when you choose the right coverage. To avoid overpaying, compare quotes from multiple insurers, choose the right policy type, and buy only the amount of coverage you need. Applying earlier can also help you secure lower premiums and a wider range of coverage options.

Factors affecting life insurance costs for seniors

The cost of life insurance premiums for Canadian seniors depends on factors such as their age, health history, smoking status, gender, and the type of policy that they have purchased. The following factors can affect the cost of life insurance for seniors in Canada:

- Age: Age is one of the biggest factors affecting your premium. Seniors who apply in their 50s or early 60s pay lower premiums than those applying in their 70s or 80s

- Gender: Women generally pay lower life insurance premiums than men because, on average, they have a longer life expectancy. The difference in pricing varies by insurer and policy type

- Health and medical history: Conditions such as diabetes, heart disease, high blood pressure, or a history of cancer may affect your eligibility and premium. Depending on your health, you may qualify for fully underwritten or no medical life insurance for seniors in Canada

- Policy type: Term life insurance is usually the most affordable option for healthy seniors, while whole life and no medical life insurance generally have higher premiums because they provide lifelong coverage or easier eligibility

- Coverage amount: Higher coverage amounts result in higher premiums. Choosing coverage based on your actual financial needs can help keep your policy affordable

- Medical underwriting: Policies that require a medical exam often offer lower premiums for healthy applicants. No medical life insurance for seniors in Canada provides easier access to coverage but usually comes at a higher cost

- Smoking status: Smokers pay significantly more for life insurance due to the increased health risks associated with tobacco use

Best life insurance companies for seniors in Canada (2026)

Some of the best life insurance companies for Canadian seniors include Manulife, Canada Life, Wawanesa, Industrial Alliance (iA), and Canada Protection Plan. Take a deep dive into their offerings and ratings

Top life insurance companies for seniors (2026)

| Company | Key features | Best for | Rating |

| Manulife | Canada’s largest life insurer, offering strong participating whole life insurance with competitive dividends and excellent estate planning value. Alternatively, seniors who don’t qualify for traditional coverage can access one of the highest guaranteed issue coverage limits with up to $100,000 in coverage. | Seniors looking for whole life insurance and estate planning solutions | 5/5 |

| Canada Life | Offers a unique 5-year term option for older applicants, Pick-A-Term coverage up to age 85, and lifelong coverage options. | Seniors who want flexible term lengths later in life | 4/5 |

| Wawanesa | Uses your actual age instead of your nearest age to calculate premiums, which can result in lower rates, and offers coverage starting at $10,000 to help keep premiums affordable. | Seniors looking for lower premiums or smaller coverage amounts | 4/5 |

| Industrial Alliance (iA) | Takes a more accommodating approach to certain health conditions and offers coverage starting at $25,000 to help keep premiums affordable. They also offer guaranteed issue life insurance. | Seniors with pre-existing medical conditions | 4/5 |

| Canada Protection Plan (CPP) | Offers guaranteed issue life insurance, offering up to $50,000 in coverage with no health questions, which is higher than many comparable guaranteed issue plans. | Seniors with significant health concerns or those who may not qualify for traditional underwriting | 4/5 |

How much life insurance coverage do seniors need in Canada?

Unlike younger applicants who have greater financial obligations, seniors need life insurance mainly to cover final expenses. However, others may require a larger policy to replace income for a surviving spouse, pay off debts, leave an inheritance, or cover estate settlements.

To know the exact coverage seniors need, here are the factors that they should consider:

- Outstanding mortgage, loans, and other debts

- Expected funeral, burial, or cremation costs

- Whether your spouse or dependents rely on your retirement income

- Any estate taxes or probate costs your beneficiaries may need to pay

- Existing savings, pensions, investments, and other financial assets

- The financial legacy you want to leave to your loved ones

When is it a good time to get life insurance for seniors?

The best time for seniors to buy life insurance is as early as possible. Applying in your 50s or early 60s can help you qualify for lower premiums, higher coverage amounts, and a wider range of policy options. As you age, life insurance generally becomes more expensive, and health conditions may limit your eligibility for certain policies.

Is it too late to get life insurance after 70 in Canada?

No, it is not too late to get life insurance after age 70 in Canada. While your options may be more limited than they were at a younger age, many insurers still offer whole life, simplified issue, and guaranteed issue life insurance to seniors in their 70s. Some insurers also offer term life insurance, depending on your health at the time of application

Common mistakes seniors make when buying life insurance

The most common mistakes seniors make when buying life insurance include waiting too long to apply, choosing the wrong type of policy, buying too much or too little coverage, and not comparing quotes from multiple insurers. Avoiding these mistakes can help you secure the right coverage at a more affordable premium while ensuring your family’s financial needs are met.

- Waiting too long to apply: Premiums generally increase with age, and delaying your application can limit your coverage options

- Buying more coverage than you need: Many seniors base their coverage on financial obligations they no longer have. Choosing a larger policy than necessary can lead to higher premiums without added value

- Choosing the wrong policy type: Select between term, whole life, or no-medical life insurance based on your age, health, budget, and long-term needs

- Not disclosing your medical history: Always provide accurate health information to avoid delays, policy changes, or claim issues

- Focusing only on the lowest premium: The cheapest life insurance for seniors in Canada may not provide the coverage, features, or flexibility you need. Compare benefits, exclusions, renewal options, and insurer reputation alongside the premium

- Not comparing multiple insurers: Premiums, eligibility requirements, and policy features vary by insurer, so comparing quotes can help you find better value

Our advisor’s take on the best life insurance for seniors

At PolicyAdvisor, our licensed advisors help seniors compare life insurance policies based on their age, health, budget, and financial goals. Recently, one of our advisors assisted a 68-year-old retiree who wanted affordable coverage to help cover final expenses and leave a financial benefit for their spouse without paying for more insurance than they need.

The client profile

- Age: 68 years old

- Coverage required: $100,000

- Health: Non-smoker with well-controlled high blood pressure

- Primary goal: Cover final expenses and provide financial security for a surviving spouse

The policy comparison: After comparing quotes from several leading Canadian life insurance providers, we recommended a fully underwritten whole life insurance policy. Although no-medical life insurance offered a faster approval process, the client’s good overall health meant they qualified for significantly lower premiums through traditional underwriting while receiving the same lifetime protection and a higher coverage amount

Our advisor’s recommendation

For most seniors, the best life insurance policy depends on why they need coverage rather than age alone. Seniors in good health can often save money by choosing a fully underwritten policy, while those with more complex medical histories may benefit from simplified issue or guaranteed issue life insurance. Comparing senior life insurance quotes in Canada online from multiple insurers helps identify the best combination of affordability, coverage, and long-term value for your individual needs.

How to choose the best life insurance policy as a senior

Seniors can easily buy life insurance in Canada once they have figured out their needs. For a more customized experience, you can speak to a licensed Canadian life insurance advisor at PolicyAdvisor.

- Figure out your coverage needs: Start by thinking through your reason for buying life insurance and what you need to secure. This will help you determine what kind of coverage you need. Our advisors will help you with the best plans available based on your coverage needs

- Get free life insurance quotes: Our quoting tool searches the Canadian insurance market for you in seconds. Compare senior life insurance quotes in Canada online

- Apply for the quote: Once you have selected the right policy, our advisors will help you apply for the right life insurance quote online. Schedule a call now to get started!

Frequently asked questions

Is life insurance for seniors over 60 in Canada available without a medical exam?

Yes, seniors in Canada who are over 60 can get life insurance without a medical exam. Many insurers offer simplified issue and guaranteed issue life insurance policies, which are designed for applicants who want coverage without undergoing a medical examination.

How much life insurance do seniors need?

Normally, experts say you should get 10-15x your annual income in coverage. Canadian life insurance for seniors is different; many are already retired and only want to help pay for final expenses or leave an inheritance for their family.

Is life insurance for seniors different from other types of insurance?

Life insurance for seniors generally costs more than it does for younger applicants because age and health increase the insurer’s risk. While many seniors choose lower coverage amounts to help cover final expenses or estate costs, they can still purchase higher coverage amounts if they qualify and need them.

What is the best life insurance for seniors?

The best life insurance for seniors depends on your age, health, budget, and financial goals. Term life insurance is often suitable for temporary needs, while whole life insurance offers lifelong protection. Seniors with health concerns may benefit from simplified issue or guaranteed issue life insurance.

Is whole life insurance better than term life insurance for seniors?

It depends on your needs. Term life insurance is generally more affordable and provides coverage for a set period, while whole life insurance offers lifelong protection, guaranteed premiums, and cash value growth. The right choice depends on your financial objectives and budget.

How can seniors get the best life insurance rates?

Seniors can often secure better rates by applying as early as possible, maintaining good health, choosing an appropriate coverage amount, avoiding tobacco use, and comparing quotes from multiple insurers before purchasing a policy. If you are in good health, qualifying for a fully underwritten policy can also help reduce your premiums.

Is life insurance worth it after age 70?

Yes, life insurance can still be worthwhile after age 70 if you want to cover funeral expenses, pay off outstanding debts, protect a surviving spouse, or leave a financial legacy. While premiums are generally higher than for younger applicants, many insurers continue to offer whole life, simplified issue, and guaranteed issue policies for seniors.

Can I get life insurance for my 80‑year‑old parent in Canada?

Yes, you can purchase life insurance for your 80-year-old parent in Canada, provided you have their consent and meet the insurer’s requirements. While coverage options are more limited at this age, many insurers still offer whole life, simplified issue, and guaranteed issue life insurance. The exact eligibility, coverage amounts, and premiums vary based on the insurer and your parent’s health.

Up to what age can you buy life insurance in Canada?

The maximum age to buy life insurance depends on the insurer and the type of policy. Many insurers offer term life insurance up to ages 75-85, while whole life, simplified issue, and guaranteed issue policies may be available up to age 85 or older. The maximum entry ages and coverage limits vary by insurer.

Life insurance for seniors in Canada helps cover final expenses, outstanding debts, estate costs, and financial support for loved ones. This guide explains eligibility, policy options, coverage amounts, costs, factors affecting premiums, and tips to help seniors choose the right life insurance policy.