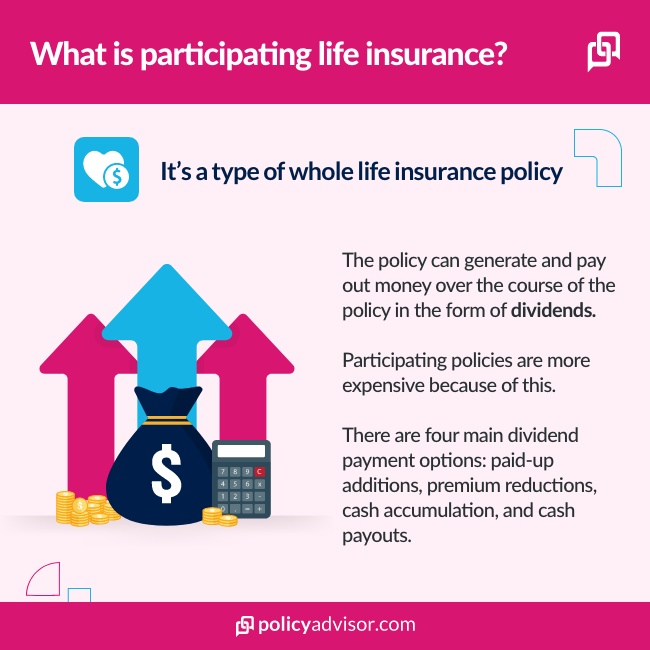

- Participating life insurance policies are more expensive due to the investment component.

- There are four main dividend payment options are paid-up additions, premium reductions, cash accumulation, and cash payouts.

- Dividends can fluctuate greatly, and some may prefer to invest their money in more stable financial options.

Participating life insurance has the potential to pay out more than straight life insurance, but it does so at the cost of greater volatility.

What is participating in life insurance in Canada?

Participating life insurance in Canada is a type of whole life insurance policy that gives policyholders a share in the insurer’s profits. These profits are distributed in the form of dividends.

These dividends can be used to lower premiums or buy additional coverage. The policy provides lifelong protection and includes a cash value that continues to grow over time. Book a call with us and find out if this insurance policy will suit your needs!

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

How does participating life insurance work in Canada?

Participating life insurance, in addition to the guaranteed death benefit, can generate and pay out money over the course of the policy in the form of dividends.

These dividends, which are determined by the insurance company’s performance and profits, are typically issued to the policyholder annually. The general idea is that the permanent life insurance policyholder can share in the insurance company’s profits while they are living.

Where do the dividends come from exactly? In short, they come from earnings generated by the premiums that the policyholder pays to the insurance company. Participating policy premiums are pooled and invested by the insurer. The investment income is then used by the insurance company to pay out benefits and other expenses.

The dividends, therefore, come from any surplus profits from the participating investment fund. It should also be noted that dividends are not guaranteed (in contrast to the death benefit) and can fluctuate depending on investment performance.

How much does participating life insurance cost?

Participating life insurance in Canada can cost somewhere between $44 to $450 per month depending on an individual’s age, gender and health condition. Due to the potential for annual investment earnings, participating life insurance is significantly more expensive than term life insurance and standard whole life insurance.

In some cases, participating life insurance policyholders can save money in the long term (via dividends and cash value), though again, this is not guaranteed.

As a form of whole life insurance, participating life insurance has fixed premiums, meaning that you pay a fixed rate over the course of your entire policy. In general, whole life insurance has higher premiums than term life insurance because policies lifetime coverage and must therefore account for the added risk of aging and health issues.

Here’s what the cost of participating life insurance may look like:

Cost of participating life insurance in Canada

| Age | $100K coverage – Male | $100K coverage – Female |

| 20 | $54/month | $44/month |

| 30 | $75/month | $63/month |

| 40 | $110/month | $92/month |

| 50 | $164/month | $138/month |

| 60 | $263/month | $217/month |

| 70 | $444/month | $376/month |

*Quotes based on $100k in coverage for a non-smoker in regular health on a life-pay plan. Quotes based on average prices from leading insurance companies in Canada.

What are the different types of participating life insurance policies?

Participating life insurance policyholders have a few options when it comes to how their dividends are issued in their life insurance plan. Before we take a closer look at these dividend options it is important to understand how the dividends are calculated.

Every year the insurance provider will calculate the dividend rate by taking a number of factors into account, including investment earnings, expenses, mortality (which influences the amount of benefits paid), and taxes. When investment earnings exceed the expenses, benefits, and taxes, a dividend may be issued to participating insurance holders.

The four main dividend payment options in participating life insurance products

Paid-up additions

With paid-up additions, policyholders can put their dividends towards purchasing additional coverages which are added to their existing policy. This is a good option for those who want to increase their insurance coverage as well as future dividends. It is also a reliable way to increase your policy’s non-guaranteed cash value. This is also sometimes referred to as additional paid-up insurance.

Premium reduction:

Policyholders can also choose to use their dividends to pay their life insurance premiums (or at least a portion of them). In this case, the dividend would reduce the amount of money owed annually to the insurance provider.

Typically, dividends can only be used to reduce premium payments if the policyholder has an annual premium payment plan.

On deposit/Cash accumulation

In this scenario, the life insurance company simply puts any dividends into an interest-earning account—not unlike a savings account.

The interest rate is set on an annual basis by the insurance provider and policyholders can access their dividends whenever needed.

Paid in cash

Policyholders can choose to receive their dividends as a direct cash payment, which is issued annually by insurance providers. It should be noted that if you choose to receive your dividends as a cash payout, the money may be subject to income tax.

What is the difference between a participating and non-participating life insurance policy?

Participating policies allow policyholders to share in the insurer’s profits through dividends, which help to reduce premiums or can be taken as cash. Non-participating policies do not provide dividends.

Difference between participating and non-participating life insurance

| Feature | Participating life insurance | Non-participating life insurance |

| Definition | Offers policyholders a share in the insurer’s profits through dividends | Does not provide dividends; only offers guaranteed death benefits |

| Premiums | Higher due to the potential for dividends and additional benefits | Lower as it only includes guaranteed benefits and no profit-sharing |

| Dividends | Policyholders may receive dividends | No dividends are paid to policyholders |

| Cash value growth | Cash value grows faster | Cash value grows at a fixed rate |

| Suitability | Suitable for individuals seeking long-term growth | Ideal for those wanting a straightforward, cost-effective policy |

Why a participating policy may not be for you?

Non-participating policies are usually cheaper than participating ones because of the dividend expense. Life insurance providers charge more in order to return the excess dividends to the policyholder. Additionally, there are added tax implications for the policy, as the excess proceeds from the dividends may be considered income.

What is considered to be a participating insurer?

A participating insurer is an insurance company that issues participating insurance policies, allowing policyholders to share in the company’s profits through dividends. These dividends are typically distributed from the insurer’s surplus earnings and can be received as cash or reinvested to increase policy benefits.

Participating policies are common in life insurance and provide both guaranteed and non-guaranteed benefits. The insurer’s financial performance determine the amount and frequency of dividends.

Who should consider getting participating life insurance in Canada?

Participating life insurance policy can be the right for a number of individuals including high net-worth individuals, families who prioritise estate planning, small business owners and more.

Participating life insurance is a versatile option offering lifelong coverage and the potential to earn dividends. It’s particularly suited for individuals with specific financial goals:

- High-net-worth individuals: Ideal for those looking to preserve and grow wealth while ensuring a tax-efficient inheritance for their beneficiaries

- Families looking for estate planning solutions: Helps cover estate taxes, leaving a more significant legacy for loved ones

- Small business owners: Provides liquidity for succession planning or buy-sell agreements while building cash value for future opportunities

- People seeking long-term wealth-building opportunities: Combines life insurance protection with savings growth through dividends and cash value accumulation, supporting long-term financial goals

What are the benefits of participating life insurance in Canada?

Participating life insurance is a versatile financial product offering a blend of lifetime protection and wealth-building opportunities such as tax-advantages cash value growth, flexible dividend options, guaranteed death benefit and participation in insurer’s profits. Find more about these benefits:

- Tax-advantaged growth of cash value: The policy’s cash value grows on a tax-deferred basis, helping Canadians accumulate wealth more efficiently. This can be especially advantageous for retirement planning or funding future expenses

- Flexibility with dividend options: Policyholders receive dividends based on the insurer’s performance and can use them to purchase additional coverage, reduce premium payments, take cash payouts, or leave them to grow within the policy for enhanced cash value

- Guaranteed death benefit and lifelong coverage: Participating life insurance provides a tax-free death benefit that offers financial security for loved ones while guaranteeing lifelong coverage as long as premiums are paid

- Participation in the insurer’s profits: As a policyholder, you share in the company’s profits through annual dividends. This adds an investment-like component to the policy, enabling long-term financial growth

- Stability and long-term financial planning: Participating policies offer consistent returns and stability, making them an excellent option for Canadians focused on long-term financial security and estate planning

What is the disadvantage of participating in whole life insurance?

Participating in whole life insurance can come with certain disadvantages such as higher cost of premiums, complexity, and surrender charges that may not make it ideal for everyone. Understanding these drawbacks is essential before committing to a policy.

Here are some key disadvantages of participating in whole life insurance:

- High premium costs: Whole life insurance premiums are significantly higher than term insurance, which can strain your budget over time

- Limited investment control: While dividends provide an additional benefit, the policyholder has no control over how the insurer invests the funds

- Complexity and fees: Whole life insurance policies can be complicated, with surrender charges and administrative fees reducing the cash value if you decide to exit early

Carefully weigh these disadvantages against your financial goals and make sure to do a life insurance comparison before choosing the right one for you.

What are the common mistakes to avoid when buying participating life insurance?

If you are looking to buy participating life insurance, you must steer clear of mistakes like misunderstanding the dividend performance, overcommitting to higher premiums, ignoring the cash value component and not comparing policies by the top insurers.

- Misunderstanding dividend performance: Assuming dividends are guaranteed without recognizing they depend on the insurer’s financial performance

- Choosing the wrong dividend option for financial goals: Selecting dividend options without aligning them with personal objectives, such as growth, premium reduction, or liquidity needs

- Overcommitting to premiums without assessing affordability: Committing to higher premiums than your budget allows, which could lead to policy lapse

- Ignoring the cash value component: Failing to understand how the cash value grows and how it can be accessed or utilized effectively

- Not comparing policies across insurers: Overlooking better rates or benefits by not shopping around and comparing options from multiple companies

- Neglecting long-term needs: Buying a policy that doesn’t account for future changes in financial circumstances or coverage requirements

Frequently asked questions

How are dividends calculated for participating policies in Canada?

Dividends for participating policies are calculated based on the insurer’s financial performance. Factors include investment returns, claims payout, and operating expenses. Insurers typically allocate a portion of their surplus earnings to policyholders as dividends.

Dividends are distributed annually and vary depending on market conditions and company performance. These dividends can be used to reduce premiums, purchase additional coverage, or grow the policy’s cash value, providing flexibility and added benefits to the policyholder.

Are participating policies worth the higher premiums?

Participating policies can be worth the higher premiums for individuals seeking both lifelong coverage and financial growth. They provide guaranteed death benefits and cash value growth, plus the potential for dividends, which can enhance the policy’s value over time.

These policies also offer flexibility, such as using dividends to reduce premiums or access funds. While they cost more than term or non-participating policies, the added benefits make them a strong choice for long-term wealth building and financial security.

Can I switch from a non-participating policy to a participating policy?

Yes, you can switch from a non-participating policy to a participating policy but it depends on the insurer’s terms and your eligibility. This may typically require underwriting and a health assessment, as participating policies have different structures and premiums.

But before you switch, consider the higher costs and potential surrender charges from your existing policy. Consulting with an insurance advisor (such as our experts at PolicyAdvisor) can help you assess whether switching aligns with your financial goals or not.

Is participating life insurance taxable in Canada?

The death benefit from participating life insurance is generally tax-free for beneficiaries in Canada. Additionally, the policy’s cash value grows on a tax-deferred basis, allowing wealth to accumulate efficiently. However, withdrawals or loans taken against the policy may be subject to taxation if they exceed the adjusted cost basis.

How do participating policies compare to other investment options?

Participating policies provide stable, long-term growth through cash value and dividends. While they offer guaranteed death benefits and tax-advantaged growth, the returns are typically lower than high-risk investments.

They can be ideal for individuals prioritizing security and financial stability over aggressive growth, but may not replace higher-yield investments for those seeking maximum returns.

Participating life insurance policies can generate and pay out money over the course of the policy in the form of dividends share by the insurance company managing the funds. However, participating in the policy comes at a greater cost and you share some financial risk with the insurance provider.