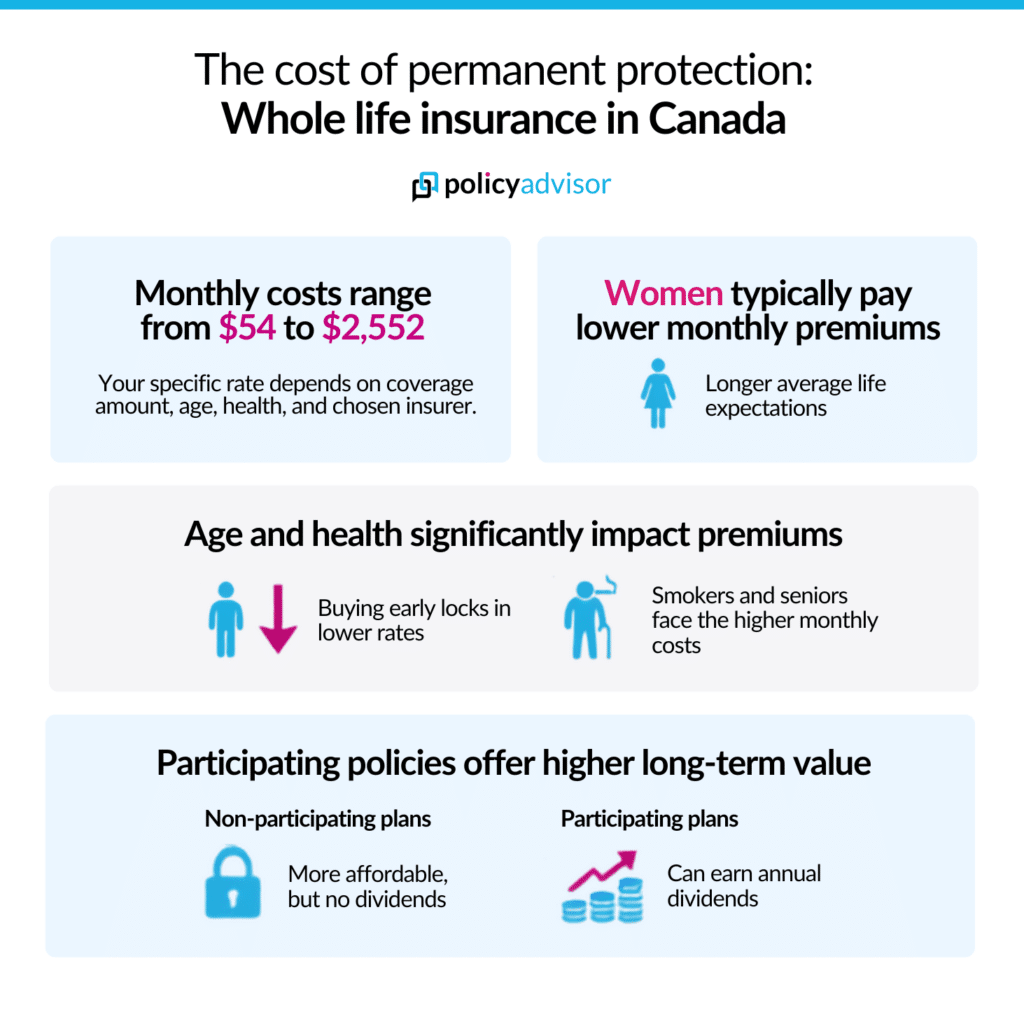

- Whole life insurance costs approximately $54 to $2,552 per month, but the exact cost depends on factors like the coverage amount, policyholder's age, health status, etc

- Non-participating whole life insurance is generally more affordable than participating whole life insurance, while participating policies offer the potential to earn annual dividends that can increase the policy’s long-term value

- A 30-year-old non-smoker can expect to pay about $100 per month for a $100,000 non-participating whole life insurance policy, although premiums vary by insurer and personal profile

- Whole life insurance costs more than term life insurance, but it provides lifelong coverage, guaranteed cash value growth based on the policy terms, level premiums, and a tax-free death benefit, making it a valuable long-term financial planning tool

The cost of whole life insurance typically ranges from $54 to $2,552 per month, depending on your age, health, coverage amount, premium payment option, and the insurer you choose. While whole life insurance costs more than term life insurance, the higher premiums provide benefits that last a lifetime, including permanent coverage, level premiums, and tax-advantaged cash value growth. Some policies, such as participating policies, may also earn annual dividends, depending on the insurer and policy type, further increasing their long-term value.

Quick summary of whole life insurance costs in Canada

| Cost category | Typical monthly premium range |

| By plan type |

|

| By coverage amount |

|

| By applicant category |

|

| Payment option |

|

| By insurers |

|

Disclaimer: The illustrative monthly premiums below are based on the examples used throughout this guide. Your actual premium will vary based on your personal profile, coverage needs, and the insurer you choose.

How much does whole life insurance cost?

Get instant quotes from Canada's top life insurance providers and find the perfect coverage for your family.

Powered by

![]()

What affects the cost of whole life insurance in Canada?

The whole life insurance cost depends on your personal profile, coverage needs, and the type of policy you choose. The following factors affect how the cost of your whole life insurance policy will be determined in Canada:

- Age: Age is one of the biggest factors affecting whole life insurance premiums. Buying a policy at a younger age typically results in significantly lower premiums because insurers view younger applicants as lower-risk

- Health: Your overall health, medical history, and any pre-existing conditions affect your premium. Applicants in good health typically qualify for lower whole life insurance rates

- Smoking status: Smokers usually pay considerably higher premiums than non-smokers due to the increased health risks associated with tobacco and nicotine use. Many insurers offer non-smoker rates after you have been tobacco-free for at least 12 months

- Gender: Women often pay lower premiums than men because, on average, they have a longer life expectancy

- Coverage amount: Choosing a higher death benefit increases your premium since the insurer assumes a larger future payout

- Policy type: Participating whole life insurance generally costs more than non-participating policies because it offers the potential to earn annual dividends, which may increase your policy’s cash value and death benefit over time

- Premium payment option: The payment schedule you choose also affects your monthly premium. Policies with a 10-pay or 20-pay option have higher premiums because the policy is paid off in fewer years, while life pay spreads payments over a longer period, resulting in lower monthly costs

- Insurance company: Premiums can vary between insurers because each company uses its own underwriting guidelines, dividend scale, and pricing structure. Comparing quotes from multiple insurers can help you find the best value for your needs

- Policy riders: Adding optional riders, such as a child rider, disability waiver of premium, or guaranteed insurability rider, increases the overall cost of your policy but provides additional protection and flexibility

Whole life insurance cost in Canada by plan type

Different types of whole life insurance come with different premium costs and long-term benefits. In Canada, you can choose between participating and non-participating whole life insurance. Participating policies generally have higher premiums because they may pay annual dividends, while non-participating policies offer lower premiums with guaranteed benefits but no dividend potential.

What is the cost of participating whole life insurance?

The cost of participating whole life insurance typically starts at $138.42 per month for a 20-year-old non-smoker with $100,000 in coverage under a 20-pay premium option. For a comparable female applicant, the premium starts at $118. Participating policies may be suitable for individuals seeking lifelong coverage, guaranteed cash value growth, and the potential to earn eligible annual dividends, which may increase the policy’s cash value and death benefit over time.

Cost of participating whole life insurance

| Age (in years) | Male (non-smoker) | Female (non-smoker) |

| 20 | $138.42 | $118.89 |

| 30 | $177.84 | $156.15 |

| 40 | $228.96 | $207.00 |

| 50 | $292.23 | $270.81 |

| 60 | $382.14 | $351.81 |

*Illustrative monthly premiums for non-smoking male and female of various age ranges seeking a participating whole life insurance policy with $100,000 in coverage for a 20-pay premium option

What is the cost of non-participating whole life insurance?

The cost of non-participating whole life insurance typically ranges from $57 to $319 per month. It is generally more affordable than participating whole life insurance and may be a good option for individuals looking for permanent coverage, guaranteed cash value, and predictable premiums without dividend participation.

Cost of non-participating whole life insurance

| Age (in years) | Male (non-smoker) | Female (non-smoker) |

| 20 | $70.74 | $57.24 |

| 30 | $100.35 | $88.74 |

| 40 | $141.66 | $127.53 |

| 50 | $223.83 | $181.71 |

| 60 | $319.41 | $277.92 |

*Illustrative costs for non-smoking male and female of various age ranges seeking a non-participating whole life insurance policy with $100,000 in coverage for a 20-pay premium option

Whole life insurance cost by coverage amount in Canada

The amount of coverage you choose directly affects the cost of your whole life insurance policy. In general, higher coverage amounts come with higher premiums because the insurer assumes a larger death benefit payout. For instance, the cost of whole life insurance with $100,000 in coverage will be lower than that of $250,000 in coverage because the insurer is assuming a smaller death benefit. The tables below show illustrative monthly premiums for different coverage amounts.

How much is a $100,000 whole life insurance policy?

The cost of a $100,000 whole life insurance policy typically ranges from $57.24 to $382.14 per month for non-smokers. This coverage amount is well suited for covering final expenses, leaving a modest inheritance, or supplementing an existing life insurance policy. It also provides lifelong protection while building guaranteed cash value over time.

Cost of a $100,000 whole life insurance policy

| Age (in years) | Male (Non-participating) | Male (Participating) | Female (Non-participating) | Female (Participating) |

| 20 | $70.74 | $138.42 | $57.24 | $118.89 |

| 30 | $100.35 | $177.84 | $88.74 | $156.15 |

| 40 | $141.66 | $228.96 | $127.53 | $207.00 |

| 50 | $223.83 | $292.23 | $181.71 | $270.81 |

| 60 | $319.41 | $382.14 | $277.92 | $351.81 |

*Illustrative monthly premiums for non-smoking males and females of various age ranges seeking a whole life insurance policy with $100,000 in coverage for a 20-pay premium option

How much is a $250,000 whole life insurance policy?

The cost of a $250,000 whole life insurance policy ranges from $132 to $914 per month for non-smoking applicants, depending on age, gender, and whether you choose a participating or non-participating policy. This coverage amount may be suitable for individuals or families looking to replace a portion of their income, pay off outstanding debts, or help cover future financial obligations.

Cost of a $250,000 whole life insurance policy

| Age (in years) | Male (Non-participating) | Male (Participating) | Female (Non-participating) | Female (Participating) |

| 20 | $156.38 | $323.10 | $132.30 | $285.98 |

| 30 | $225.45 | $415.58 | $204.75 | $377.55 |

| 40 | $328.05 | $540.22 | $298.35 | $495.00 |

| 50 | $521.55 | $697.28 | $427.95 | $644.40 |

| 60 | $765.45 | $914.40 | $649.80 | $842.40 |

*Illustrative monthly premiums for non-smoking males and females of various age ranges seeking a whole life insurance policy with $250,000 in coverage for a 20-pay premium option

How much is a $750,000 whole life insurance policy?

The cost of a $750,000 whole life insurance policy typically ranges from $350 to $2,552 per month for non-smokers, male and female. This higher coverage amount is designed for individuals with more complex financial needs, such as protecting a family’s lifestyle, supporting estate planning goals, or preserving wealth for future generations.

Premiums are higher for $750,000 in coverage because the insurer guarantees a larger death benefit. Like all other whole life insurance policies, it also offers lifelong coverage and guaranteed cash value growth according to the policy terms. Participating policies may also be eligible to earn annual dividends.

Cost of a $750,000 whole life insurance policy

| Age (in years) | Male (Non-participating) | Male (Participating) | Female (Non-participating) | Female (Participating) |

| 20 | $450.00 | $892.35 | $350.77 | $801.90 |

| 30 | $666.00 | $1,162.35 | $581.62 | $1,059.07 |

| 40 | $980.55 | $1,522.12 | $881.77 | $1,401.30 |

| 50 | $1,523.25 | $1,966.95 | $1,241.10 | $1,829.93 |

| 60 | $2,167.65 | $2,552.18 | $1,891.12 | $2,382.75 |

*Illustrative monthly premiums for non-smoking males and females of various age ranges seeking a whole life insurance policy with $750,000 in coverage for a 20-pay premium option

Whole life insurance cost by applicant type in Canada

The cost of whole life insurance varies from one applicant to another because insurers assess each person’s level of risk before determining their premium. In general, younger applicants, women, and non-smokers tend to pay lower premiums, while older applicants and smokers typically pay more due to the higher likelihood of future insurance claims. The tables below show how whole life insurance premiums vary across common applicant types.

Cost of whole life insurance based on gender

The cost of whole life insurance for non-smokers typically ranges from $70.74 to $319.41 per month for males and $57.24 to $277.92 per month for females, depending on age. The cost of whole life insurance is generally lower for women, and they pay lower premiums than men. This is because females have a longer average life expectancy, resulting in a lower mortality risk for insurers over the lifetime of the policy.

Whole life insurance costs: Male vs female

| Age (in years) | Male | Female |

| 20 | $70.74 | $57.24 |

| 30 | $100.35 | $88.74 |

| 40 | $141.66 | $127.53 |

| 50 | $223.83 | $181.71 |

| 60 | $319.41 | $277.92 |

*Illustrative monthly premiums for non-smoking males and females of various age ranges seeking a non-participating whole life insurance policy with $100,000 in coverage for a 20-pay premium option

Cost of whole life insurance based on smoking status

The cost of whole life insurance for smokers typically ranges from $84.60 to $413.34 per month, compared to $57.24 to $319.41 per month for non-smokers. Smokers pay higher premiums because tobacco and nicotine use increase the risk of serious health conditions and reduce life expectancy, increasing the likelihood of future claims.

Whole life insurance cost for a smoker vs. a non-smoker

| Age (in years) | Male (Non-smoker) | Male (Smoker) | Female (Non-smoker) | Female (Smoker) |

| 20 | $70.74 | $100.08 | $57.24 | $84.60 |

| 30 | $100.35 | $139.14 | $88.74 | $118.53 |

| 40 | $141.66 | $205.07 | $127.53 | $177.17 |

| 50 | $223.83 | $289.29 | $181.71 | $246.55 |

| 60 | $319.41 | $413.34 | $277.92 | $349.26 |

*Illustrative monthly premiums for smoking and non-smoking males and females of various age ranges seeking a non-participating whole life insurance policy with $100,000 in coverage for a 20-pay premium option

Cost of whole life insurance for children

The cost of whole life insurance for children can start from $100 per month for a 20-pay participating whole life policy. Purchasing whole life insurance for a child at a young age allows parents or grandparents to lock in lower lifetime premiums while providing lifelong coverage and guaranteed cash value growth. Over time, eligible dividends may increase the policy’s cash value and death benefit, depending on the policy and dividend option selected.

Cost of life insurance for a male child

| Age | Monthly premiums | Accumulated cash value | Death benefit |

| 5 years | $100/month | $0 | $159,200 |

| 20 years | $100/month | $17,000 | $159,200 |

| 35 years | No payment of premiums after the first 20 years | $50,000 | $218,000 |

| 50 years | $129,000 | $347,000 | |

| 70 years | $401,000 | $634,000 |

*Illustrative accumulated cash value and death benefit for a $100/month, 20-pay participating whole life insurance policy issued to a healthy 5-year-old boy. Projected cash values and death benefits assume current dividend scales and are not guaranteed; the actual policy values may vary

Cost of whole life insurance for seniors

The cost of whole life insurance for seniors typically ranges from $277.92 to $960.57 per month for seniors aged 60 to 80 with $100,000 in coverage under a 20-pay option. Premiums are generally higher for seniors because the likelihood of future insurance claims increases with age. Despite the higher cost, whole life insurance can help cover final expenses, leave a tax-efficient inheritance, and support estate-planning goals for seniors’ beneficiaries.

Whole life insurance costs for seniors

| Age (in years) | Male (Non-participating) | Male (Participating) | Female (Non-participating) | Female (Participating) |

| 60 | $319.41 | $382.14 | $277.92 | $351.81 |

| 65 | $409.14 | $445.77 | $345.06 | $404.64 |

| 70 | $544.95 | $485.41 | $441.54 | $468.81 |

| 75 | $782.37 | $671.04 | $607.05 | $569.07 |

| 80 | $960.57 | $904.77 | $745.38 | $750.87 |

*Illustrative monthly premiums for non-smoking males and females of various age ranges seeking a whole life insurance policy with $100,000 in coverage for a 20-pay premium option

Whole life insurance costs by premium payment option

The cost of whole life insurance ranges between $38 and $323, depending on your age and the payment option you choose. Your premium payment option determines how long you will pay for your whole life insurance policy and how much you will pay each month. Shorter payment periods generally have higher monthly premiums because the policy is paid off sooner, while longer payment periods spread the cost over more years.

- 20 Pay: Pay premiums for 20 years, after which your policy remains fully paid up for life while your lifelong coverage and cash value continue to grow

- T65: Pay premiums until age 65, making it a popular option for those who want to complete payments before retirement while keeping lifelong coverage

- Life Pay: Pay premiums until age 100, resulting in the lowest monthly premiums by spreading the cost over the longest payment period

Whole life insurance cost by payment option

| Age (in years) | 20 Pay | T65 | Life Pay |

| 20 | $70.74 | $54.81 | $38.97 |

| 30 | $100.35 | $74.34 | $52.65 |

| 40 | $141.66 | $128.70 | $82.89 |

| 50 | $223.83 | $322.83 | $131.76 |

| 60 | $319.41 | – | $209.16 |

*Illustrative monthly premiums for a male non-smoker of various age ranges seeking a non-participating whole life insurance policy with $100,000 in coverage

Cost of whole life insurance by insurer in Canada

The cost of whole life insurance can vary noticeably between insurers, even for applicants with the same age, gender, coverage amount, and policy type. For example, a 20-year-old non-smoking male pays $70.74 per month with Foresters Life, compared to $113.49 per month with Canada Protection Plan for the same $100,000 of coverage. Differences in underwriting, pricing, and product design mean that the same applicant may receive different premiums from different insurers. Hence, comparing quotes from best whole life insurance companies helps you find the perfect combination of premium, policy features, and long-term value.

Whole life insurance cost by insurer

| Age (in years) | Foresters Life | Desjardins | Sun Life | iA Financial Group | Canada Protection Plan |

| 20 years | Male: $70.74

Female: $57.24 |

Male: $78.21

Female: $69.66 |

Male: $91.17

Female: $80.46 |

Male: $94.68

Female: $81.90 |

Male: $113.49

Female: $102.96 |

| 30 years | Male: $100.35

Female: $88.74 |

Male: $105.66

Female: $95.13 |

Male: $114.21

Female: $102.42 |

Male: $114.03

Female: $104.13 |

Male: $131.49

Female: $121.50 |

| 40 years | Male: $141.66

Female: $127.53 |

Male: $151.29

Female: $134.01 |

Male: $166.23

Female: $150.93 |

Male: $177.03

Female: $147.96 |

Male: $171.81

Female: $160.56 |

| 50 years | Male: $223.83

Female: $181.71 |

Male: $235.26

Female: $191.70 |

Male: $267

Female: $222.03 |

Male: $251.73

Female: $210.15 |

Male: $237.69

Female: $221.13 |

| 60 years | Male: $319.41

Female: $277.92 |

Male: $333.72

Female: $294.48 |

Male: $346.41

Female: $306.90 |

Male: $366.75

Female: $303.75 |

Male: $355.32

Female: $317.25 |

*Illustrative monthly premiums for non-smoking males and females of various age ranges seeking a non-participating whole life insurance policy with $100,000 in coverage for a 20-pay premium option

Is whole life insurance worth the cost?

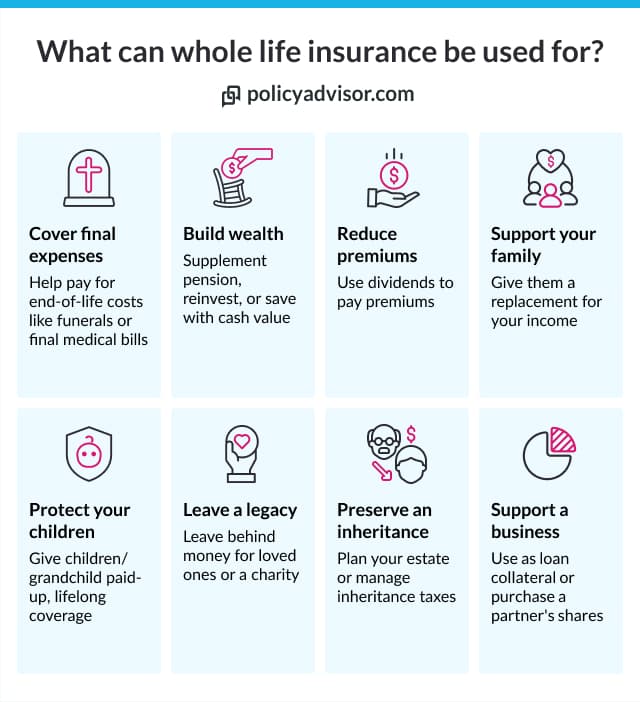

Yes, whole life insurance can be worth the cost if you are looking for lifelong financial protection and long-term wealth-building benefits. Whole life insurance typically costs more than a comparable term life insurance policy, but the higher premiums provide lifelong financial benefits, including:

- Lifetime coverage that never expires as long as premiums are paid

- Guaranteed cash value growth that accumulates over time

- Level premiums that remain unchanged throughout the life of the policy

- Tax-advantaged cash value growth while the policy remains in force

- Support for estate planning and wealth transfer through a generally tax-free death benefit paid to beneficiaries

- Potential annual dividends on participating whole life policies, which may increase the policy’s cash value and death benefit over time

How does the cost of whole life insurance compare to term life insurance?

Whole life insurance generally costs more than term life insurance for the same coverage amount because it provides lifelong coverage and accumulates cash value over time. For example, a $100,000 whole life insurance policy costs approximately $57 to $382 per month, while a $100,000 term life insurance policy costs around $7 to $44 per month, making term life insurance the more affordable option for short-term coverage needs.

If you only need life insurance for a specific period, such as while paying off a mortgage or supporting your family, term life insurance may be the more cost-effective option. If you need lifelong coverage or want to build cash value over time, whole life insurance may be worth considering.

How to reduce the cost of whole life insurance

Although whole life insurance generally costs more than term life insurance, there are several ways to make coverage more affordable, such as buying early, choosing the right coverage amount, comparing quotes, and more. Here are some of the ways in which you can reduce the cost and get the cheapest whole life insurance:

- Buy coverage early: Purchasing whole life insurance at a younger age helps you lock in lower premiums for life

- Choose the right coverage amount: Choose a coverage amount that aligns with your financial needs without paying for more coverage than necessary

- Maintain a healthy lifestyle: Good overall health and remaining tobacco-free can help you qualify for lower premiums

- Consider a non-participating policy: If dividend potential isn’t important to you, a non-participating policy can provide permanent coverage at a lower cost

- Select a longer premium payment period: Options such as Life Pay generally have lower monthly premiums than shorter payment schedules like 20 Pay because premium payments are spread over the entire policy period

- Compare quotes from multiple insurers: Premiums can vary significantly between insurance companies for the same coverage. Comparing quotes through PolicyAdvisor lets you evaluate plans from Canada’s leading insurers and find the best value based on your budget and financial goals. Schedule a call now to get instant whole life insurance quotes!

Frequently asked questions

Why is whole life insurance more expensive than term life insurance?

Whole life insurance costs more because it provides lifelong coverage, guaranteed cash value accumulation, and a guaranteed death benefit. Participating policies may also be eligible to earn annual dividends, adding further long-term value. Term life insurance only covers you for a fixed period and does not build cash value, making it a more affordable option.

How does adding riders affect whole life insurance premiums?

Adding optional riders, such as critical illness coverage, accidental death benefits, or disability waiver of premium, increases whole life insurance premiums. Riders provide additional benefits tailored to individual needs but come at an added cost. For example, a critical illness rider might add 10-20% to the base premium.

Can I lower my whole life insurance premiums after buying a policy?

In most cases, your premiums are fixed when you purchase the policy and cannot be reduced later. However, you may be able to lower your overall costs by choosing a different payment option, reducing your coverage amount, or selecting a non-participating policy.

Can I switch from term life insurance to whole life insurance?

Yes, many term life insurance policies include a conversion option that allows you to convert some or all of your coverage to whole life insurance without completing a new medical exam. The conversion must usually be completed before a specified age or policy anniversary, depending on your insurer.

How much does a $250,000 whole life insurance policy cost?

The cost of a $250,000 whole life insurance policy ranges from $132-$914. The actual costs may vary based on your age, gender, health, smoking status, policy type, and insurer. In general, premiums are higher for $250,000 than for $100,000 in coverage.

Which premium payment option has the lowest monthly cost?

Life Pay typically offers the lowest monthly premiums because the cost of the policy is spread over the longest payment period. In contrast, 20 Pay policies have higher monthly premiums but are fully paid up sooner.

How can I reduce the cost of whole life insurance?

You can lower your whole life insurance premiums by purchasing coverage at a younger age, choosing an appropriate coverage amount, maintaining good health, selecting a non-participating policy, opting for a longer premium payment period, and comparing quotes from multiple insurers.

Whole life insurance can cost anywhere from $54-$2,552 per month, depending on your personal profile and the type of coverage you need. Whole life insurance costs more than term life insurance because it provides lifelong coverage, guaranteed cash value accumulation, and a guaranteed death benefit whenever the insured passes away. Whole life insurance is worth the price if you want cash value accumulation opportunities, stable premiums, and lifetime coverage.