- Whole life insurance and permanent life insurance both have lifelong coverage with an investment component

- Whole life offers more stable growth and less control over investments

- Universal life gives you more control over investments, but has a greater risk

Knowing the ins and outs of different life insurance policies is essential to choosing the right type of coverage for your needs. In this article, we compare whole life insurance vs universal life insurance: two common types of permanent insurance that give you coverage for life but also differ in important ways.

What do whole life and universal life have in common?

Whole life insurance and universal life insurance share some important key features. Namely, they both:

- Provide lifelong life insurance coverage as long as premiums are paid

- Come with an investment component and cash value component, which can be used as collateral for policy loans

- Pay a tax-free death benefit, just as term plans do

What is your Whole Life Insurance worth?

Get instant quotes from Canada's top life insurance providers and find the perfect coverage for your family.

Powered by

![]()

What is the difference between whole life and universal life insurance?

These two types of life insurance also have key differences in terms of premiums, death benefits, cash value, and dividends that set them apart. Let’s take a look:

Difference between whole life and universal life insurance

| Aspect | Whole Life Insurance | Universal Life Insurance |

| Premiums |

|

|

| Death benefit |

|

|

| Cash value |

|

|

| Dividends |

|

|

| Investments |

|

|

What is permanent life insurance?

Permanent life insurance lasts for your entire life. Unlike a term life insurance policy, which only covers a specific period of time, permanent plans cover the policyholder until they pass away.

As with all life insurance, permanent policies pay out a death benefit to your beneficiary. They’re best used for long-term needs, like taking care of estate taxes, caring for dependents, and paying for end-of-life expenses like funeral costs.

Additionally, unlike term insurance, most permanent life insurance policies have an investment component that accumulates a cash value. This is one of the most attractive features of permanent policies, in addition to the all-important death benefit options. Many Canadians use this investment component to supplement their retirement income.

Permanent life insurance usually comes with two investment options:

- Participating policies: These generate dividends that are paid out to you every year.

- Non-participating policies: There are no dividend payments but the cost of insurance is lower.

What is whole life insurance?

Whole life insurance (WL) is a type of permanent life insurance coverage that accumulates a cash value. As with all permanent life insurance plans, it provides lifelong coverage. As long as premium payments are made for the duration of the policy, beneficiaries are guaranteed to receive a tax-free death benefit when the insured dies.

With whole life policies, the cost of insurance is decided at the start of your contract and remains fixed for the policy’s duration. This means you are guaranteed to pay the same premium rate for the rest of your life, unlike with renewable term plans.

How does whole life insurance work?

When you apply for a whole life policy, premium rates are decided based on the amount of coverage and other factors like your age, health, and lifestyle. In some cases, you may be asked to take a medical exam.

Once your policy is approved, you are responsible for paying premiums either annually or monthly, depending on your agreement with the life insurance provider.

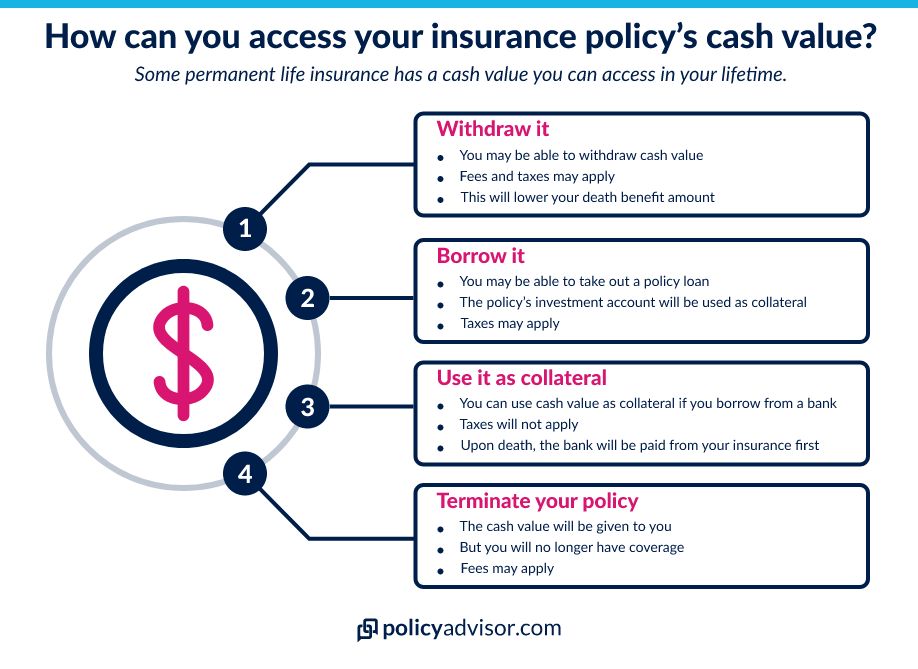

Every time you pay premiums, a portion of the money goes towards keeping the policy active and covering administration fees, while another portion is invested by your life insurance provider. This money is your policy’s cash value. It increases with a fixed interest rate and on a tax-deferred basis.

You also have access to cash value during your lifetime. Or, if you cancel the policy, you can walk away with a cash surrender value of whatever has accumulated minus applicable surrender charges. This can be accessed whether you have participating or non-participating whole life insurance.

When a whole life policyholder passes away, their beneficiary is guaranteed a death benefit. This is paid by the life insurance company as a one-time, tax-free payment. This money can be used as income replacement for family members, to cover final expenses, as an inheritance, or anything else the beneficiary chooses to use it for.

What are the pros and cons of whole life insurance?

Whole life insurance has several pros such as lifetime coverage, guaranteed death benefit, cash value accumulation and more. But there may be some disadvantages such as higher premiums, limited growth potential, making it complex to understand.

Pros

- Lifetime coverage: Whole life insurance provides coverage for your entire life, as long as premiums are paid

- Guaranteed death benefit: Beneficiaries receive a fixed payout regardless of when you pass away

- Cash value accumulation: A portion of your premiums builds cash value, which grows tax-deferred and can be borrowed or withdrawn

- Wealth transfer and estate planning: Whole life insurance is often used to pass on wealth efficiently or cover estate taxes

Cons

- Higher premiums: Whole life insurance is more expensive than term life insurance, making it less affordable for some

- Limited investment growth: The cash value growth is typically lower compared to other investment options

- Complexity: The combination of insurance and savings can make the policy harder to understand and manage

- Opportunity cost: Funds tied up in premiums may yield better returns if invested elsewhere

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What is universal life insurance?

Universal life insurance (UL) is also a type of permanent life policy that provides lifelong coverage and a tax-free death benefit when the policyholder dies.

But what stands out the most about this type of insurance is its flexible premiums, death benefits, and investment options. This is perhaps the biggest difference between universal and both whole and term policies.

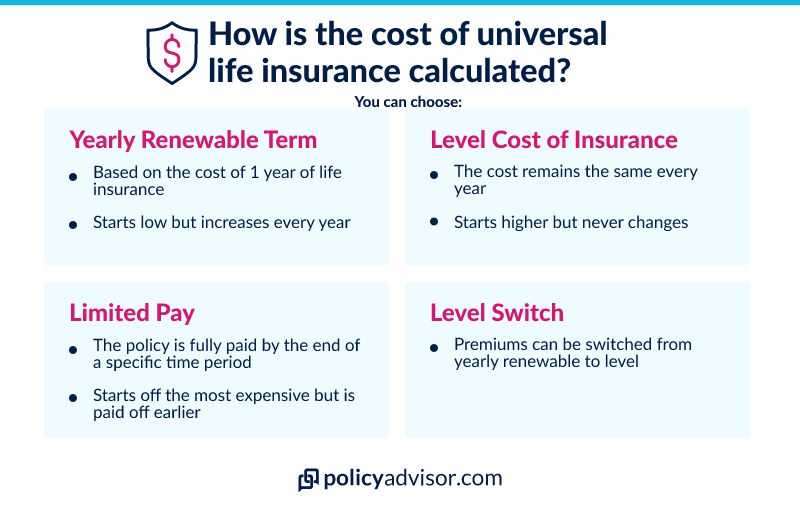

With a universal policy, you choose how much they want to pay in premiums. Of course, there is a minimum payment amount, which covers the cost of insuring the policyholder as well as administration fees.

However policyholders can decide how much more they want to contribute to their policy’s cash value portion. The minimum premium cost can also vary over the course of the policy, depending on whether the size of the death benefit changes.

In addition to flexible premiums, this type of policy can give you a greater say in how your cash value is invested. You can choose between three different investment options, which vary in terms of interest rate and risk:

-

Daily Interest Account (DIA)

Interest is calculated and credited every day. The interest rate is set by the insurer and may fluctuate.

-

Guaranteed Interest Account (GIA)

Guaranteed interest rates for a specific period of time, such as 1, 5, or 10 years.

-

Variable Interest Options (VIO)

Interest depends on index performance, mutual funds, or other managed portfolios. Potentially bigger returns but also higher risk.

How does universal life insurance work?

Applying for a universal life insurance policy looks similar to other permanent life insurance policies: your minimum premium rate is decided by the life insurance provider based on amounts of coverage, as well as age, health, and lifestyle.

To keep the policy active, you must ensure that your policy’s premiums are paid as agreed with your insurer. When you pass away, your beneficiaries will be entitled to a one-time, tax-free death benefit.

But unlike with whole life insurance, you can decide how much money you want to pay into a UL policy’s cash value. Because of this, people may often consider universal life when they’re looking for an investment strategy.

For instance, they may treat their universal life policy as an investment account where they deposit money to be invested. The cost of the life insurance policy is deducted by the insurer, and the remaining balance can then be invested and generate tax-deferred interest.

Is universal life insurance risky?

Universal life coverage is considered risky compared to whole life insurance. Whereas whole life insurance offers many guarantees (fixed premiums, death benefit, policy dividend options), universal life insurance offers flexibility and a wider range of investment options. Naturally, this comes with greater risk.

That being said, the level of risk associated with a universal life insurance plan depends on the type of investments chosen. Universal life policyholders should always keep in mind that their cash value depends on their rate of return.

The greatest risk is if you rely on your policy’s cash value to pay your premiums. If your investments underperform and you do not have enough money in your cash value account to cover premiums, your policy can lapse. This could leave you without the crucial death benefit options that life insurance is meant to provide in the first place. It is therefore important to keep a close eye on the investment portion of your universal plan.

Whether this form of life insurance is the right choice for you depends on your appetite for risk. Even if you’re just thinking over permanent life insurance options, you should speak with a licensed life insurance expert like the ones at PolicyAdvisor.com before you make your choice.

What are the pros and cons of universal life insurance?

Universal life insurance has certain advantages such as flexible coverage, tax advantages, varied investment options, and access to withdraw or loan from the cash value. However, there are some disadvantages such as higher premium costs, risk on investment of cash value and surrender charges.

Pros

- Adjustable coverage: You can modify the death benefit amount to align with changing financial needs

- Tax-advantaged growth: The cash value grows tax-deferred, which can be beneficial for long-term wealth accumulation

- Investment options: Many policies allow you to choose investment portfolios, potentially earning higher returns

- Loan or withdrawal access: The cash value can be accessed for loans or withdrawals, providing liquidity for emergencies or opportunities

Cons

- Complexity: The combination of insurance and investment makes the policy harder to understand and manage

- Higher costs: Fees and administrative charges can reduce returns, especially in the early years

- Investment risk: Returns on the cash value are tied to market performance, which could lead to losses or reduced growth

- Surrender charges: Early termination of the policy may result in significant fees, reducing the cash value

Is universal life insurance cheaper than whole life insurance?

Universal life insurance can be much cheaper than whole life insurance, for a few different reasons.

With whole life insurance, you pay higher premium rates over the course of the policy to ensure a guaranteed premium rate, death benefit, and cash value.

With a universal life insurance product, on the other hand, you can choose to decrease your policy’s death benefit and premium payments based on your needs. Universal life insurance is also less expensive because the policyholder takes on more risk by generating cash value through investments rather than a fixed interest rate.

How much does whole life insurance vs. universal life insurance cost?

Life insurance premiums can depend on factors like age, sex, health, and lifestyle.

But, to give you an idea, a non-smoking male in his mid-30s can expect to pay roughly $160 per month for a whole life insurance policy worth $250,000.

The same man can expect to pay about $120 per month for universal life insurance. But, remember, the cost of universal life insurance varies: you can choose to pay more to increase your universal life cash value.

Read more about how much life insurance costs in Canada.

Whole life vs. universal life insurance: Which is better?

The choice between whole life and universal life insurance depends on your financial goals and priorities. Whole life insurance offers stability with fixed premiums, a guaranteed death benefit, and predictable cash value growth, making it ideal for those who value simplicity and lifelong coverage.

In contrast, universal life insurance provides flexibility, allowing you to adjust premiums and death benefits while offering investment options for potentially higher cash value growth. However, it requires more active management and comes with investment risks.

If you prefer a straightforward, reliable policy, whole life insurance may be better. If flexibility and growth potential align with your needs, universal life insurance could be the smarter choice.

Key factors to consider when choosing between whole life and universal life insurance

When considering choosing between whole life and universal life insurance, factors such as financial goals, risk tolerance, budget, and long-term goals come into mind. Here’s a comparison:

Factors to consider when choosing between whole life and universal life insurance

| Factors to consider | Whole life insurance | Universal life insurance |

| Financial goals | Offers stability with guaranteed benefits and cash value growth | Provides flexibility with adjustable premiums and death benefits |

| Risk tolerance | Suits those preferring predictable growth without market exposure | Appeals to individuals comfortable with market-linked returns |

| Budget | Requires higher, fixed premiums for lifetime coverage | Allows adjustable premiums based on financial circumstances |

| Long-term goals | Ideal for estate planning or wealth transfer | Suitable for retirement funding or flexible financial planning |

Frequently asked questions

Which is more flexible: whole or universal life insurance?

When it comes to flexibility, universal life insurance is the clear winner.

Whole life insurance is known for its consistency. It has guaranteed premium rates, death benefits, and cash value growth.

But universal life policies let you decide how much you want to invest in the policy’s cash value component. And this type of policy gives you more control over investments, letting you decide on the level of risk to potentially maximize gains. The death benefit is also flexible; you can choose to decrease or increase the size of the benefit depending on your changing needs.

Which gives a greater cash value?

It really depends. Universal policies may have a greater potential for growth, but also greater risk. On the other hand, cash accumulation is more steady in whole life policies over time.

Whole life insurance has guaranteed and more or less predictable cash value growth. Every time you pay your monthly or annual premiums, a portion is added to your cash value, which grows based on a fixed interest rate. Universal life cash value accumulation depends on factors like your premium payments.

In a strong market, universal life insurance can have much higher returns than whole life insurance policies. In a weak market, however, returns are not guaranteed. This is why it’s important not to get dazzled by the potential growth alone.

Which builds cash value quicker?

Universal life insurance has the potential to grow cash value more quickly if you invest in your policy early on and investments perform well.

With whole life insurance, the portion of premiums that goes towards cash value decreases over time — as the cost to insure you goes up. This means that the cash value grows at a more rapid rate in the early years of the policy, but then begins to slow.

Is universal life insurance better than whole life insurance?

When it comes down to it, no type of policy is “better” than another. The best policy is determined based on your needs.

If a stable and easy-to-manage policy is what you want, then whole life insurance will be better than universal life. Of the two, it’s the lowest-risk option for policyholders.

If you want flexibility and a greater say in how your money is invested, then universal life insurance will be the best choice.

Can you convert universal life to whole life or vice versa?

No, it is not possible to convert whole life insurance to universal life insurance or vice versa. So, choose wisely before you decide to buy!

We know that with permanent coverage, there are so many diverse options and combinations that it can be tricky to plan your best move. But that’s why the PolicyAdvisor experts are here to guide you and help if you’re looking for alternative options for an existing policy. Give us a call today or schedule one in the future so we can review the best options for you and your family’s financial security.

The two major types of permanent life insurance are whole life and universal life. They both offer similar benefits, but stand on opposite sides of the scale when it comes to investments. The question of which one is right for you depends on your long-term goals, and how much risk you want to take.