- The cost of life insurance increases with age, so getting a life insurance policy in your 30s can benefit your wallet.

- Term life insurance provides flexibility for people in their 30s, with low premiums and the potential for conversion to whole life insurance.

- Having a mortgage or dependents—or planning to have them in the near future—are two good reasons to think about life insurance in your 30s.

Aside from the cost of life insurance in your 30s, you might be wondering if you need it at all. It’s a fair question—at 30 you have so much life ahead of you!

The truth is, even if you have little liabilities and you’re just starting out, you should buy life insurance in your 30s. Depending on the type of policy you choose, you can use life insurance to meet your financial goals now and set up financial security for your family’s future.

Read on to find out the benefits of buying life insurance at a young age and how to get the best deal on life insurance in your 30s.

How much is life insurance in your 30s in Canada?

Term life insurance costs about $25-$30 per month for $500,000 in coverage when you’re in your 30s and a non-smoker.

Your insurance premium depends on various factors including your age, gender, smoking status, lifestyle, and overall health. Smoking almost doubles your life insurance rates in your early years, and then almost triples it by the end of your 30s.

You can read more about what affects the price of life insurance here.

Monthly cost of life insurance by age

To give you a ballpark idea of how much life insurance might cost in your 30s, we’ve crunched the numbers from 30 different Canadian insurance companies to give you a chart with the average cost of life insurance on a 20-year term, divided by gender and smoking status.

Term Life Insurance Cost in 30s – Male, 20-Year Term

| Age | $250K | $500K | $1MM |

|---|---|---|---|

| 30 | $19 | $31 | $58 |

| 31 | $19 | $32 | $58 |

| 32 | $20 | $32 | $59 |

| 33 | $20 | $32 | $60 |

| 34 | $21 | $33 | $59 |

| 35 | $21 | $33 | $59 |

| 36 | $23 | $36 | $64 |

| 37 | $24 | $39 | $70 |

| 38 | $26 | $42 | $77 |

| 39 | $27 | $45 | $82 |

*Representative values, based on regular health

The story is similar for women, though initial life insurance rates are lower at this age, with smoking continuing to have a meaningful impact on your costs. Here are some average life insurance rates for females looking for a 20-year term policy.

Term Life Insurance Cost in 30s – Female, 20-Year Term

| Age | $250K | $500K | $1MM |

|---|---|---|---|

| 30 | $15 | $23 | $41 |

| 31 | $16 | $23 | $41 |

| 32 | $16 | $24 | $42 |

| 33 | $16 | $25 | $43 |

| 34 | $17 | $26 | $45 |

| 35 | $17 | $26 | $45 |

| 36 | $18 | $28 | $49 |

| 37 | $19 | $30 | $52 |

| 38 | $20 | $32 | $57 |

| 39 | $21 | $34 | $61 |

*Representative values, based on regular health

Those are the average prices for term life insurance in your 30s, but you may be looking quotes for other types of policies. The cost of whole life insurance at age 30 is still affordable, but will be more expensive than term life.

Looking for a more exact monthly rate? Get a quote in seconds from some of the best life insurance companies in Canada. Get the lowest rates on the market by shopping over 30 insurance providers in seconds! Fill out the quote form below!

Should I get life insurance in my 30s?

Yes! The price of life insurance is way cheaper in your early years. Because of your youth and health, you can lock into lower rates. In your 30s, you have a much longer life expectancy, so the company is less likely to have to pay out a death benefit within the term you apply for.

Life insurance provides you peace of mind that your future loved ones will have financial security. Even if you don’t have a partner or children yet, you may within your 10, 20, or 30-year term.

Life insurance can be used in your future for…

- Your (future) child’s college education cost

- Outstanding debts

- Mortgage debts

- Income replacement if you are a primary breadwinner

- End-of-life costs (funeral expenses)

- To borrow against while you’re still living

You can get all of that for around $25-30/month now. The best part is, if you lock in your rates now, you keep them for your entire term. Or if you get permanent coverage, you lock in rates for life. There’s no better time to buy life insurance than right now!

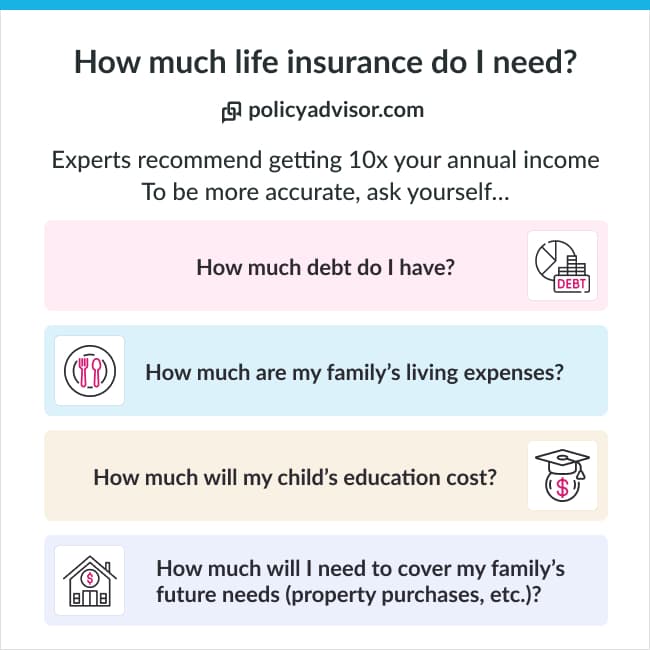

How much life insurance does a 30-year-old need?

A young Canadian in their thirties, with a new mortgage, young children, and a partner who also earns an income would need at least $500,000 in coverage to cover their remaining house payments and child-rearing expenses and cost of living for the next 20 years. You may very well need even more than that.

But how much life insurance you need at 30 years old depends entirely on your own personal situation – it’s even possible that you need no term life policy at this point in your life. If you are backpacking through Europe and paying for pints by washing dishes at your hostel, we agree, that now might not be the time.

To find out exactly how much coverage you’ll need, use our life insurance needs calculator. By filling out some simple information, we can tell you how much coverage you’ll need to meet your financial goals in your 30s and beyond.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What life insurance is best in your 30s?

There are many options for life insurance when you’re in your 30s!

How do I buy life insurance in my 30s?

Your 30s are an exciting time! You may be hitting many major life events like getting married, buying a house, or starting a family. All of those milestones come with financial responsibilities that you need to protect. To get a better idea of which policy is best for your goals in your 30s, get customized term life insurance quotes in minutes.

Still not sure how much life insurance you need? We’re always happy to chat.

The cost of life insurance for a 30-year-old is about $30 per month for about $500,000 in coverage. The exact cost depends on age, medical history, policy information, and more. People in their 30s, especially those with dependents and mortgages, should get life insurance. Locking in rates at a young age ensures lower premiums and long-term financial security for your loved ones.