- Smoking and tobacco consumption have a significant impact on life insurance premiums

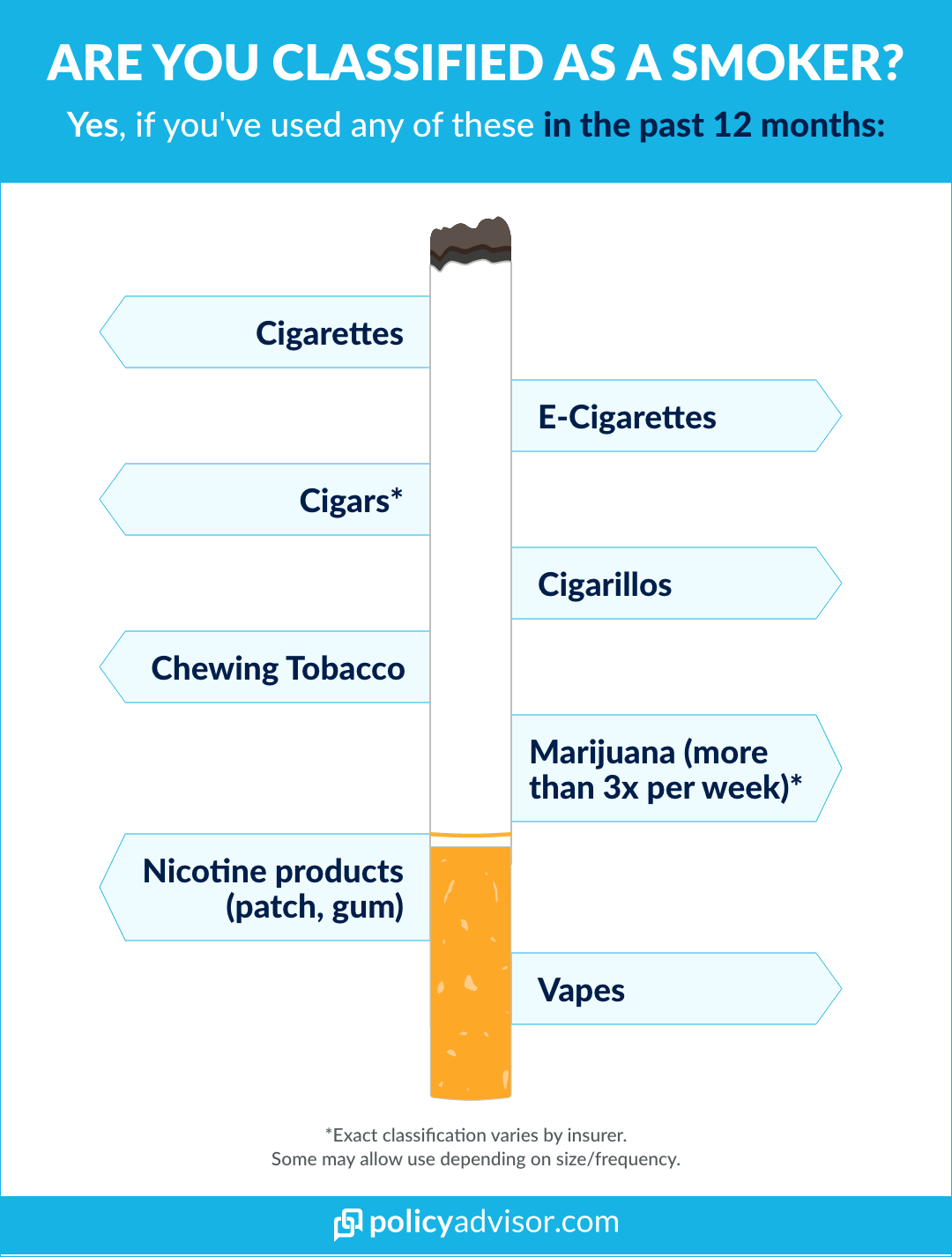

- Consumption of any form of tobacco, even a single cigarette or e-cigarette, in the last 12 months classifies you as a smoker, for life insurance purposes

- Some companies are more flexible with occasional cigar usage

- Life insurance premiums for smokers can cost as much as 50 to 100% more than those for non-smokers

- If you have quit smoking and have not used tobacco for 12 months, you can apply to have your rates reduced to non-smoker status

One of the biggest barriers for Canadians considering life insurance is what they perceive as the high price of insurance premiums. This is especially true for smokers. Those who are addicted to cigarettes often assume the price of life insurance premiums is so prohibitively high that they shouldn’t even attempt to apply.

The truth about term life insurance for smokers lies somewhere in the middle. While there are situations where the price of life insurance for a smoker can give one pause for thought, there are alternatives. This guide will shed light on how smoking affects life insurance premiums and what a smoker can expect when searching and applying for life insurance.

Can you get life insurance if you smoke in Canada?

Yes, you can get life insurance if you smoke or consume tobacco. The idea that smokers do not qualify for life insurance is incorrect. This assumption stems from the fact that coverage for term life insurance is much more expensive for those who smoke than for those who do not.

Types of life insurance for smokers

Smoking is a known risk factor for many health conditions, leading to higher premiums. However, several types of life insurance policies are available to smokers, each with distinct features, pros, and cons.

| Type of insurance | Features | Pros | Cons | Cash value |

| Term life insurance | Coverage for a specific period (10-30 years). Affordable premiums for a set term. | Lower premiums, straightforward coverage | No cash value, higher premiums for smokers | None |

| Whole life insurance | Lifelong coverage with a cash value component that grows over time. | Lifelong coverage, cash value can be borrowed or withdrawn | Higher premiums, fixed cost | Builds over time |

| Universal life insurance | Flexible premiums and coverage amounts, combining death benefit with a savings component. | Flexible payments, interest-earning cash value | Complex policy structure, higher premiums for smokers | Builds over time, earns interest |

| Guaranteed issue insurance | No medical exam, limited questions; accessible to those with health issues due to smoking. | Easy to obtain, no medical exam | Lower coverage amounts, higher premiums | None |

How does smoking affect life insurance?

The stress that cigarette smoking inflicts on one’s body has lasting, detrimental health effects. Tobacco consumers are much more likely to have a health condition later in life, such as cancer, heart disease, and stroke.

While there are many more repercussions to smoking, it is these deadly medical conditions that make a smoker’s life riskier to insure. Thus, life insurance for smokers, especially those past the age of 40, is more expensive than that for non-smokers due to these health risks.

What counts as smoking by life insurance providers?

Insurer definitions vary. Many classify any nicotine use within 12 months as a “smoker.” Some distinguish limited cigar use or non‑nicotine cannabis separately. Always verify definitions in the specific insurer’s underwriting guide.

There are also other tobacco and nicotine products that will affect your life insurance premiums. The use of cigars, cigarillos, chewing tobacco, nicotine gum, and a nicotine patch can all be considered the same as smoking by some Canadian insurance companies.

There is some leeway for a tobacco user who smokes cigars or cigarillos. The classification depends on how many you consume. An occasional cigar or cigarillo may be classified as a non-smoker as long as it averages out to one a month or less.

As advisors, we have observed more flexibility on cigar usage by insurance providers than any other form of tobacco consumption when it comes to determining smoking status. If you enjoy the occasional cigar, you can still get affordable life insurance.

Will I have to take a medical exam to test for tobacco or nicotine?

In your application for life insurance, you will be asked if you smoke. You must answer this honestly. Depending on your age and the amount of insurance you are seeking, insurance companies may require you to take a medical exam (which requires urine and blood tests). Among other things, the blood test will also help them determine your smoking habits.

Even without a medical exam, it is extremely important that you do not lie in your life insurance application. Insurance policies have a “contestability period.” This is basically a two-year period in which a provider can rescind your life insurance policy and refund the premiums if there is a material misrepresentation during the application process.

This period begins from the time your policy goes into effect. If you die within this period and the insurance company finds out that you lied about your tobacco usage, they have the right to rescind the policy and/or deny the death benefit to your beneficiary.

After two years, a policy is generally incontestable except in cases of fraud (and certain limited exceptions like misstatement of age). A non‑fraudulent misrepresentation about smoking normally cannot be used to deny a claim after the incontestability period.

What challenges do smokers face with life insurance?

Due to the health risks associated with smoking, insurers often impose higher premiums and stricter conditions. Here are some of the key challenges smokers face:

Higher premiums

One of the most significant challenges for smokers is the increased cost of premiums. Smoking is linked to numerous health issues, such as heart disease, lung cancer, and respiratory illnesses, which increase the likelihood of claims. As a result, insurers charge smokers higher premiums to offset the risk.

Limited policy options

Smokers may find fewer policy options available to them. Some insurers may be reluctant to offer coverage or may exclude certain benefits. Available policies often come with higher costs and more stringent terms.

Stricter underwriting

The underwriting process in a life insurance policy for smokers is typically more rigorous. Insurers may require detailed medical examinations and health questionnaires to assess the extent of smoking-related health risks. This can lead to delays in obtaining coverage and sometimes even denials.

Lower coverage amounts

In some cases, smokers might be offered lower coverage amounts compared to non-smokers. This is because the increased risk associated with smoking makes it less attractive for insurers to provide large sums of coverage without charging prohibitively high premiums.

Impact on existing policies

Smokers who start smoking after obtaining a life insurance policy may face challenges if their smoking status changes. While most policies are based on the applicant’s status at the time of application, any changes in health or lifestyle can still impact the policy’s terms, potentially leading to claim denials.

How much does life insurance cost for smokers?

The cost of life insurance for tobacco users varies based on factors such as age, health, and the type of policy. Generally, smokers pay significantly higher premiums compared to non-smokers.

Let us understand this with an example:

If you are a 35-year-old female in Ontario and a non-smoker, here’s how much you pay for a 20-year term policy for $500,000 coverage:

- Monthly premium: $25.17

- Annual premium: $279.72

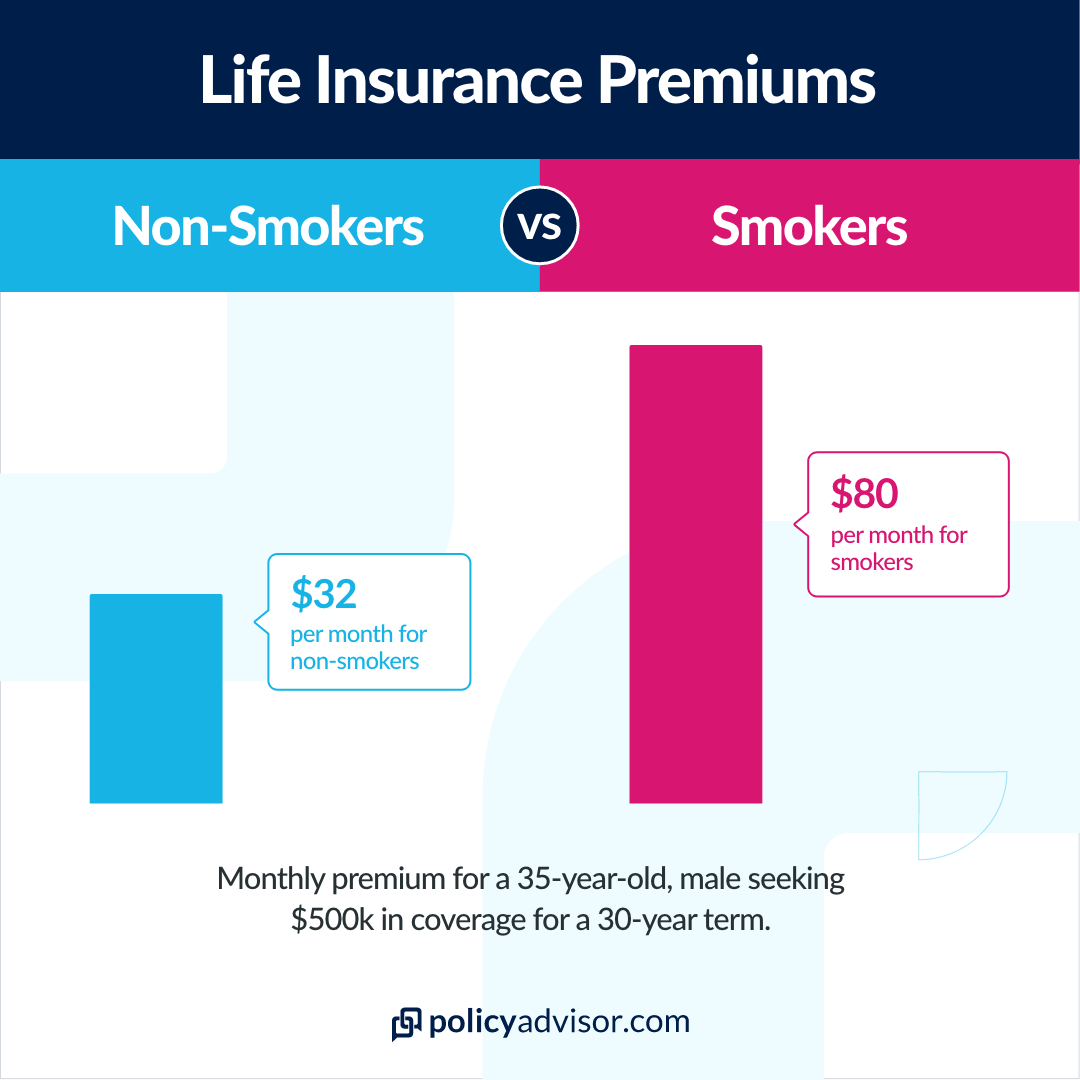

Now, let’s assume you are a 35-year-old female in Ontario, and you smoke. Here’s how much you pay for a 20-year term policy for $500,000 coverage:

- Monthly premium: $61.43

- Annual premium: $682.50

How much more will it cost to insure me if I smoke?

Canadian insurance companies offer rates on most of their term life insurance products specifically for smokers. These rates may have a smaller difference between those for smokers and non-smokers at early ages, but the difference is substantial as applicants age. Depending on the age of the applicant and the amount of coverage applied for, the cost of life insurance for smokers can be higher by 50 to 100% compared to that for non-smokers.

| Age | Male smoker | Male non-smoker | Female smoker | Female non-smoker |

| 30 | $58.41 | $30.60 | $40.05 | $22.50 |

| 35 | $80.86 | $32.85 | $61.65 | $25.65 |

| 40 | $126.45 | $47.58 | $88.65 | $35.10 |

| 45 | $205.09 | $74.35 | $138.15 | $53.55 |

| 50 | $323.95 | $123.29 | $215.10 | $85.95 |

| 55 | $535.24 | $222.98 | $331.17 | $154.43 |

| 60 | $832.22 | $392.76 | $522.00 | $283.36 |

| 65 | $1,347.30 | $681.75 | $875.70 | $479.25 |

* Illustrative monthly premiums for a 20-year term life insurance policy with a death benefit of $500,000

How to find an affordable life insurance policy as a smoker?

Life insurance and smoking don’t go too well together. While it can be challenging to find a policy that meets your needs as a smoker, here are some strategies to help you secure affordable coverage:

Consider quitting

One of the most effective ways to reduce your life insurance premiums is to quit smoking. Many insurers offer lower rates to individuals who have been smoke-free for at least 12 months.

Choose a shorter term length

Opting for a shorter term length can help reduce your premiums. While a 20-year or 30-year term policy provides longer coverage, a 10- or 15-year term can be more affordable. This approach is particularly useful if you plan to quit smoking soon and can reapply for a new policy as a non-smoker after quitting.

Be honest about your smoking status

Honesty is crucial when applying for life insurance for tobacco users. Failing to disclose your smoking habits can lead to policy cancellation or denial of claims. Insurers typically verify your health status through medical exams and health records, so it’s best to be upfront about your smoking to avoid complications later.

Consider no-exam plans

No-exam life insurance policies can be a good option for smokers who prefer a simpler application process. These policies do not require a medical exam, which can expedite approval. However, premiums for no-exam policies might be higher, and coverage amounts might be lower compared to traditional policies.

Lock in rates early

The younger you are when you purchase life insurance, the lower your premiums will be. Even as a smoker, securing a policy early can result in more affordable rates compared to waiting until you are older when age-related health issues may further increase premiums.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

Top life insurance companies for smokers in Canada

The top life insurance companies for smokers in Canada are:

Best for lowest rates: Industrial Alliance (iA)

Industrial Alliance offers the most competitive rates for smokers in Canada across all age groups. Their rates are among the lowest in the market for smokers, making them an attractive option for individuals seeking affordable life insurance coverage despite their smoking status.

Their Pick-A-Term life insurance policy allows smokers to select any term between 10 to 40 years and customize the plan according to their needs.

Best for smokers who plan to quit: Foresters Financial

Foresters Financial offers a unique plan called the Quit Smoking Incentive Plan that provides lower rates to smokers for the first two years of their certificate. If they quit smoking within this period, they can continue to qualify for the lower premiums, incentivizing them to stop smoking and potentially save thousands of dollars.

Best for cigar smokers: Canada Life

Canada Life offers life insurance options for smokers, although premiums may be higher than for non-smokers. They consider someone a smoker if they have smoked within the last 12 months, including cigarettes, cigars, e-cigarettes, chewing tobacco, pipes, and other tobacco and nicotine products.

Best for smokers committed to quitting: Manulife

For smokers who are committed to quitting, Manulife offers a policy where they can pay non-smoker premiums for the first 3 years. If the insured quits smoking and passes a nicotine test within this period, they can maintain non-smoker rates for the remainder of their policy.

If you have been tobacco-free for 12 months, you can submit a non-smoker application. If approved, your reduced non-smoker rates start on the 1st of the month following the approval of your application.

Can I get preferred rates as a smoker?

There is some silver lining for the smokers among us. Most life insurance providers offer preferred rates, or better than regular health rates, to individuals who demonstrate better than standard health. These more affordable rates are available to smokers as well as non-smokers.

As you would expect, non-smoking preferred rates are substantially better than preferred rates for smokers. Nonetheless, if you are able to get preferred pricing while being a smoker, it will save you a lot of money over the term of your life insurance.

Preferred rate standards for smokers vary by company. Some companies may have easier norms for blood pressure, cholesterol, or even driving habits than others.

Some of the Canadian life insurance companies may not offer preferred pricing to those who smoke cigarettes. Instead, they are only able to offer better pricing to cigar consumers. At PolicyAdvisor, we work with the best life insurance companies in Canada and can guide you to make the right choice.

How to apply for life insurance as a smoker?

Here are 5 quick steps to apply for life insurance as a smoker:

- Decide on the coverage amount and policy type

- Prepare details about your smoking history and health

- Speak to our licensed advisors and compare policies (consider a no-exam policy)

- Fill out the insurer’s form accurately and honestly (some policies require a health checkup)

- Check your policy’s terms before submitting your application and wait for approval to begin coverage

Frequently asked questions

How much more do smokers pay for life insurance in Canada?

Smokers typically pay 50% to 100% more in premiums compared to non-smokers. The exact amount varies by insurer, age, and health status.

Can quitting smoking lower my life insurance premiums in Canada?

Yes, quitting smoking can lead to lower premiums. Many insurers offer reduced rates to those who quit and remain smoke-free for a specified period.

Do life insurance companies test for smoking in Canada?

Yes, insurers may conduct nicotine tests, such as blood or urine tests, as part of the underwriting process to verify smoking status.

Is cannabis use classified as smoking by insurance companies?

If you vape cannabis or marijuana, insurance companies generally consider you a smoker. However, if you only use cannabis in other forms, such as edibles or tinctures, you are typically not classified as a smoker.

A major factor that influences your insurance premiums is tobacco use. Tobacco consumption is verified through your insurance application where you are asked if you are a smoker. In some circumstances, you are required to take a medical exam that collects both urine and blood samples. You are classified as a smoker if you consume tobacco in any form in the past 12 months. Smoking can increase your insurance premiums from 50-100% more than those for non-smokers.