- Past drug use can impact your eligibility for life insurance, with the type of substance, frequency of use, and time since last use all playing a role in determining coverage and premiums

- Applicants who have used drugs within the last year may be denied traditional life insurance, while those who have been sober for several years may qualify for standard policies at lower premiums

- Insurers also evaluate whether the applicant has undergone rehabilitation, received medical treatment, or is currently participating in recovery programs when determining eligibility

- No-medical-exam options, like simplified issue or guaranteed issue life insurance, are available for individuals who may not meet the criteria for traditional policies

- It’s essential to fully disclose any past drug use during the application process. Failing to do so could result in policy cancellations or claim denials later on

Past drug use can impact life insurance in Canada, but the effect depends on several factors, including the type of drug, frequency of use, time since last use, and any related health issues.

While occasional marijuana use may not significantly affect rates, past use of harder substances like cocaine, heroin, or fentanyl can lead to higher premiums or even the denial of your application.

The good news is that options still exist. Some insurers offer coverage for individuals in long-term recovery, though at higher rates, while no-medical-exam policies provide an alternative for those with a complicated history.

In this article, we’ll explore how different types of drug use affect life insurance, the potential cost implications, and the best options available for applicants with a history of substance use.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

Can I get life insurance if I’ve taken drugs in the past?

Yes, you may be able to get life insurance with a history of drug use but it can significantly impact your insurance application. Even if you’ve only used drugs once, insurers will ask about it during the underwriting process.

When applying for life insurance, you’ll be required to disclose any history of drug use, including:

- Marijuana

- Cocaine

- Methamphetamine

- Heroin

- Steroids

- Psychedelics (Mushrooms, LSD)

- Prescription drug misuse

However, past drug use doesn’t automatically mean you’ll be denied coverage or charged excessively high premiums. Insurers assess risk based on factors like:

- The type of drugs used

- How long ago they were used

- Whether you are still using drugs

- If you have sought treatment for substance use

If you are a recovering addict, you may qualify for standard policies after maintaining sobriety for 3-4 years. You can even get better rates after 6+ years of sobriety.

How do insurance companies assess drug use?

Insurers evaluate drug use because it increases the risk of health complications or premature death. Active users are typically classified as high-risk applicants, leading to policy denials or higher premiums through a process called “rating.”

Each insurer has different criteria, but most will ask about drug use over a set period. Here’s a general guideline on how past drug use affects eligibility for life insurance:

| Time since last use | Likely underwriting decision |

| Used within the last 12 months (even once) | Declined |

| Used over 3 years ago (one-time use) | Higher premium (rated) |

| Used over 5 years ago (one-time use) | Lower premium (mild rating) |

| Frequent or ongoing use | Declined |

If you’ve used drugs in the last year, traditional life insurance may not be an option. However, alternatives like simplified issue or guaranteed issue policies (which do not require medical underwriting) can provide coverage at a higher cost.

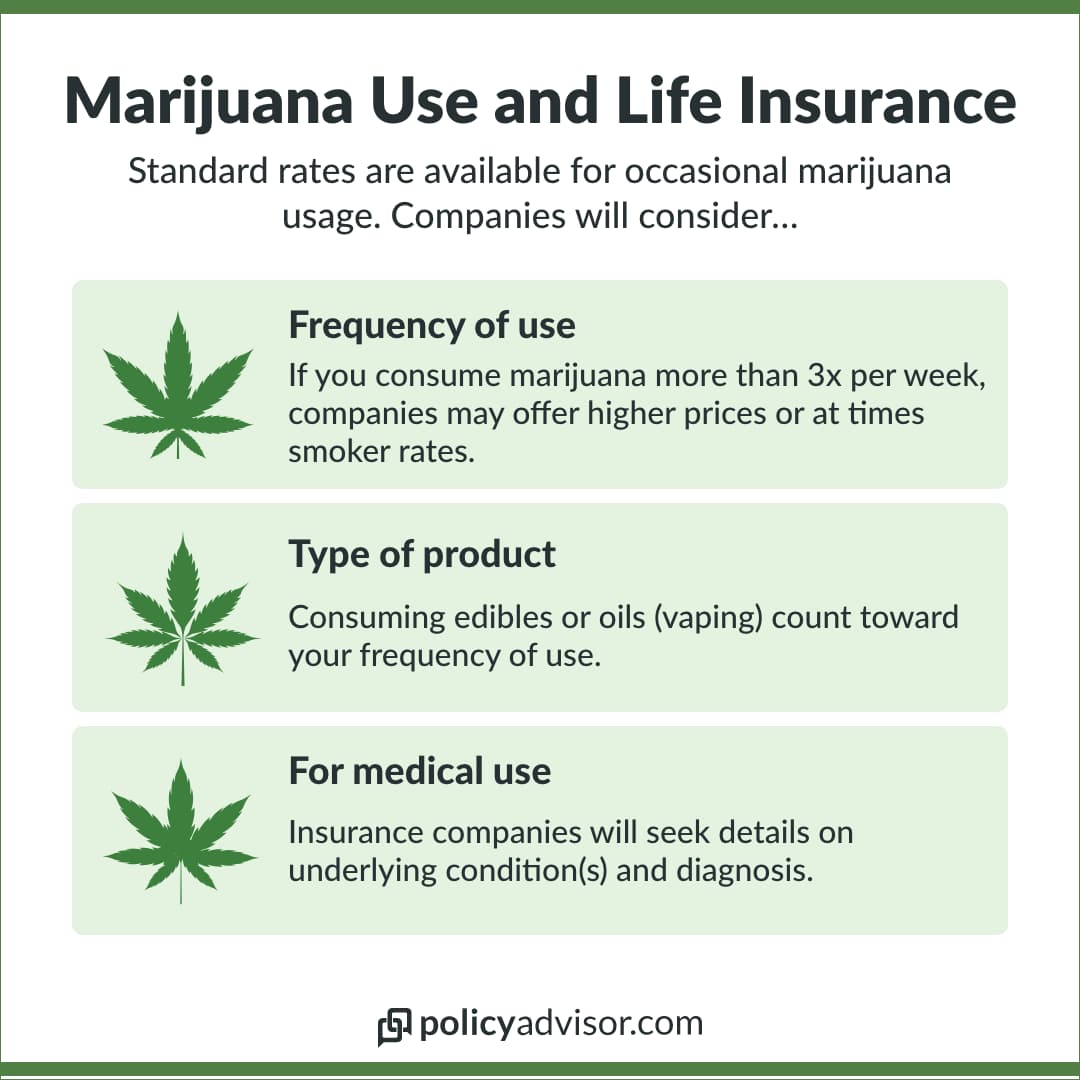

Can I get life insurance if I smoke marijuana?

Yes, you can get life insurance if you smoke marijuana. However, regular marijuana use can lead to higher premiums. If you use marijuana more than three times a week, you’ll likely face rates that are higher than non-smokers, as insurers classify regular cannabis use similarly to tobacco smoking.

Even if you only consume marijuana occasionally, any use in the current month could trigger smoker’s rates. If you’re a daily marijuana user, obtaining traditional life insurance may be challenging, as insurers may view the risk as higher.

In such cases, non-medical life insurance, which doesn’t require a full medical exam, might be an option. However, keep in mind that premiums for these policies can be significantly higher than for fully underwritten policies.

Can you get life insurance if you take methadone?

Yes, you can get life insurance if you’re on methadone for opioid addiction recovery. Insurers typically require at least two years of stable treatment and proof of sobriety from illicit drugs.

For instance, a 40-year-old on methadone for three years with clean urine tests might qualify for coverage, though premiums would be higher than someone with no addiction history.

Does depression medication affect life insurance?

Yes, taking depression medication can affect life insurance premiums. For example, someone with well-managed depression (no hospitalizations) may face a small increase in premiums, compared to someone without a history of mental health issues. The longer the condition remains stable without relapse, the less impact it will have on premiums.

Do insurance companies do drug testing?

Yes, insurance companies require drug testing for medically underwritten policies. Blood and urine tests are used to screen for illicit drugs, including cocaine, meth, opioids, and THC. Some provinces may also verify prescriptions through databases like PharmaNet.

If you disclose drug use, premiums will reflect the associated risk. However, undeclared use may lead to your policy being cancelled if drugs are detected during testing.

Can I get life insurance if I’ve been to rehab?

Yes, you can get life insurance if you’ve been to rehab. While it can be more challenging, insurers assess your drug use history when determining risk. They consider factors such as when you started using drugs, how long you’ve used them, and whether you’re still using drugs.

Many insurers require a medical exam or additional information about your drug use before offering coverage. Depending on the type of drug and how long it’s been since you last used it, the insurer may offer coverage at higher premiums or deny your application.

If you’re currently in rehab, getting life insurance may be tougher. Insurers typically want to see that you’ve completed treatment and maintained sobriety for a period of time. They might advise waiting until you finish treatment, or you could explore guaranteed acceptance or no-medical-exam options.

Life insurance for drug users in Canada

If you have a history of drug use, you may still be eligible for standard term or permanent life insurance, depending on your health and the specifics of your drug use.

However, if your relationship with drugs is more complex than occasional use, you might want to explore other types of life insurance policies that bypass extensive medical questionnaires, exams, or drug tests.

No-medical life insurance

No-medical life insurance is an option for those who prefer to avoid detailed medical assessments. With this type of coverage, you may only need to answer a few basic medical questions or sometimes none at all, depending on the policy type.

These policies come in two main forms: simplified issue and guaranteed issue. However, since the insurer is assuming more risk by not conducting a thorough underwriting review or asking about your full medical history, the premiums for no-medical life insurance tend to be higher than for medically underwritten policies.

Simplified issue life insurance

Simplified issue life insurance requires you to answer a few questions about your medical history instead of undergoing a complete physical exam. While some companies may still request certain medical tests, the overall application process is less invasive.

For those with a history of drug use, simplified issue policies tend to have more lenient requirements regarding how long it’s been since your last instance of drug use, compared to traditional medically underwritten policies. This makes it a viable option for those with a past of occasional or past drug use who are seeking quicker, more accessible coverage.

In Canada, these options can be particularly useful for individuals who may have struggled with addiction or used drugs in the past but have since maintained sobriety.

While premiums may be higher, the flexibility of no-medical life insurance policies provides an opportunity for those with a complex history to obtain coverage.

Guaranteed life insurance

Guaranteed issue life insurance is another option for individuals with a history of drug use, as it requires no medical questions or medical underwriting.

Regardless of your health status, you will qualify for coverage, making it an appealing choice for those with an extensive history of drug use, drug-related health issues, or anyone looking to avoid urine or blood tests and medical exams.

However, while guaranteed issue policies offer broad access to coverage, they are typically the most expensive type of term life insurance. Additionally, the coverage amounts tend to be lower compared to traditional policies.

This type of policy is often best suited for those who have difficulty qualifying for other types of insurance due to health concerns or past drug use but still want to secure a basic level of life insurance.

Which insurance companies offer life insurance for past drug users?

Canadian insurers such as Assumption Life, iA, UV Insurance and a few others offer life insurance for past drug users.

Insurers you can consider as someone with a history of drug use

Can I get life insurance as an active drug user?

Yes, it is possible to get life insurance as an active drug user, but it can be challenging. If you’ve used any drugs (other than marijuana) in the last 12 months, traditional policies will likely be unavailable to you.

However, you may still qualify for simplified life insurance options, although the coverage will be more limited. For example, instead of qualifying for up to $5 million in coverage with a standard policy, you may only be eligible for coverage of up to $50,000 with a simplified policy.

Should I disclose drug use on a life insurance application?

Yes, you must disclose any drug use, even if it was just one time. If the insurer later discovers that you withheld this information, they may deny your application or refuse to pay out a claim when your family files it.

Insurance companies have a two-year window, known as the contestability period, after issuing a policy to void coverage or adjust premiums if they find any errors or omissions in the application.

Does life insurance cover overdose death?

In most cases, life insurance policies do cover overdose deaths, provided the policy is in good standing. If the policyholder dies from an accidental overdose, the beneficiaries are typically entitled to the death benefit.

However, if the death is ruled as a suicide, particularly within the first two years of the policy, it will not be covered. In Canada, most insurers do pay out for suicides within the first two years of coverage, but after that period, suicide is generally covered.

Does alcohol impact life insurance?

Like drug use, excessive alcohol consumption raises the risk of premature death, which life insurers consider when assessing risk. Insurers typically ask about alcohol consumption habits, including frequency and quantity.

A history of excessive drinking or treatment for alcoholism may lead to higher premiums or make it more difficult to obtain coverage. According to the Canadian Centre for Substance Use and Addiction, here are some guidelines:

- 0 drinks per week – Not drinking offers various health benefits, including improved sleep and better overall health

- 2 drinks or less per week – This is generally considered a safe level, with minimal risk for alcohol-related consequences

- 3-6 drinks per week – At this level, the risk of certain cancers, such as breast and colon cancer, increases

- 7 or more drinks per week – This level significantly increases the risk of heart disease and stroke

Does smoking affect life insurance?

Yes, due to the higher health risks associated with smoking, life insurance premiums for smokers are typically 50-100% higher than for non-smokers. Smokers are considered to be at greater risk, and this is reflected in the cost of their insurance.

You are classified as a smoker if you’ve used or consumed any of the following in the past 12 months:

- Cigarettes

- E-cigarettes

- Cigars

- Cigarillos

- Chewing tobacco

- Recreational marijuana (more than 3 times a week)

- Nicotine products

- Vapes

How can I apply for life insurance as a drug user?

If you’re a drug user and looking to apply for life insurance, it’s important to understand that while it may come with challenges, it’s still possible to get coverage.

Life insurance providers typically assess your health history, including any drug use, to determine eligibility and premiums.

After honestly disclosing your drug use, you can consider insurers who specialize in policies for high-risk individuals. Here’s how you should approach the process of applying for life insurance as a drug user:

- Full disclosure: We recommend you to be transparent about your drug use. Failing to disclose this information can result in the denial of coverage or claims being rejected in the future

- Health assessments: Many insurers require a medical examination. Be prepared for tests that may assess your general health, including the effects of drug use on your body. Some insurers may request additional information from your doctor

- Consider the type of drug use: The impact on your application will vary depending on the type of drug use (prescribed medication vs. recreational use), frequency, and duration. Some companies may offer policies to people who have used substances in the past but have since quit

- Look for specialized insurers: Some insurance companies specialize in offering policies to individuals with higher health risks, including those with a history of drug use. These companies may charge higher premiums but can provide coverage

- Higher premiums or exclusions: If your application is approved, you must be aware that you may face higher premiums or policy exclusions related to conditions caused by drug use

- Term vs. permanent coverage: You may have more success applying for term life insurance, as it is generally less expensive and might be more flexible for individuals with a history of substance use

Frequently asked questions

Do I need to take a drug test to get life insurance?

Yes, with traditional life insurance, you will be required to undergo a medical test that includes a blood and urine sample. These tests are designed to assess your overall health, such as kidney function, blood sugar levels, cholesterol, and liver function, and will also detect substances like tobacco, alcohol, and drugs in your system. While insurers don’t specifically test for drugs, any drug in your system will be identified through the blood or urine test.

Can I buy life insurance as a recovering addict?

Yes, it’s possible to buy life insurance as a recovering addict. However, the process may be more complex, and you may be asked to provide additional details about your recovery. Insurers will want to know the length of your sobriety, the type of treatment you received, and whether you are involved in ongoing support or therapy.

If you’ve used substances in the last 12 months, you may be denied traditional life insurance. However, simplified issue life insurance or guaranteed life insurance could be alternatives, even if you’re in recovery.

Can you get life insurance if you take steroids?

Yes, you can get life insurance if you take steroids, but it may affect your premiums. Anabolic steroids, which are used for muscle growth and athletic performance, carry health risks such as liver damage and cardiovascular disease. Due to these risks, insurance companies may increase your premiums to reflect the potential impact on your health.

Can I get life insurance with mental health issues?

Yes, you can get life insurance if you have mental health issues. Your eligibility will depend on the nature of your condition, its severity, and how well it’s managed. Conditions like depression, anxiety, or bipolar disorder won’t automatically disqualify you from coverage, but insurers will evaluate your treatment plan and overall stability to assess any associated risks.

Drug use can have a significant impact on life insurance eligibility and premiums in Canada. Insurers evaluate factors such as the type of drug used, the frequency of use, and the time since last use to assess the level of risk. While individuals with a history of substance use may face higher premiums or potential application denials, those in long-term recovery may still qualify for coverage. Alternative options, such as simplified issue and guaranteed issue life insurance, are available for those who do not meet the requirements of traditional underwriting.