- People who have experienced heart disease still have life insurance options

- Many people with health conditions can apply for no medical life insurance

- Heart disease is covered as “natural death” for most existing life insurance policies

Heart health is a big deal for Canadians. Many of us know someone who has experienced some form of heart disease. And, unfortunately, Statistics Canada shows that many of us are also expected to be affected by it during our lifetime. Heart disease is so common that every 7 minutes, one Canadian suffers from a heart attack or stroke (Government of Canada statistics). During the COVID-19 pandemic in 2020, Canada actually recorded more deaths related to heart disease than ever before.

Given how common it is, a lot of Canadians wonder if heart disease could prevent them from getting life insurance. And if their insurance company would still make a payout to their loved ones if they were to pass away from a cardiovascular disease like heart attack, cardiac arrest, or a similar type of heart condition.

The answers to those questions depend on a lot of different factors. So, in this article, we’ll look at:

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What is a heart attack?

A heart attack happens when someone’s heart suffers damage due to a lack of blood flow and, consequently, lack of oxygen. It’s also called a “myocardial infarction” and is often caused by a blood clot. How severe the heart attack is depends on how long the lack of blood flow lasts. In the worst-case scenario, a heart attack can lead to cardiac arrest and even death.

Heart attacks are often unexpected. But some factors can make people more likely to have heart problems, such as:

Sometimes, genes can make someone more likely to have heart problems. But lifestyle choices, like smoking, can also increase chances of having heart issues.

Can you get life insurance if you’ve had a heart attack?

Don’t worry, there’s a good chance you can still get term life insurance or permanent life insurance even after you’ve had a heart attack. The real question is what type of coverage you’re eligible for. And that can depend on factors like how severe your heart attack was, how long ago it happened, and how well you’ve been recovering.

When you apply for life insurance, the company will ask about your current health and your medical history. They will look at whether you have had heart disease before to decide if they will give you insurance. They’ll want to know things like:

- How old you were when you were diagnosed

- How long it has been since you were diagnosed

- If you’ve been hospitalized

- If you’ve received treatment or had surgery

- If you have a complicated health history that may make heart disease worse

Many heart attack survivors can get a type of life insurance called “no medical.” This type of coverage does not require a medical exam, so it can be a good option for people with heart conditions. Getting traditional life insurance may be difficult for people who have had a heart attack in the past. Some companies may not want to give insurance to someone who already had or currently has a serious health condition, also called a “pre-existing condition.” As a last resort, heart attack survivors can consider guaranteed acceptance life insurance. It all depends on the individual circumstances of the person applying.

We’ll take a look at each of these options below. Click here to skip to that section. Or read on to learn more details about what factors life insurance companies look at for heart attack survivors.

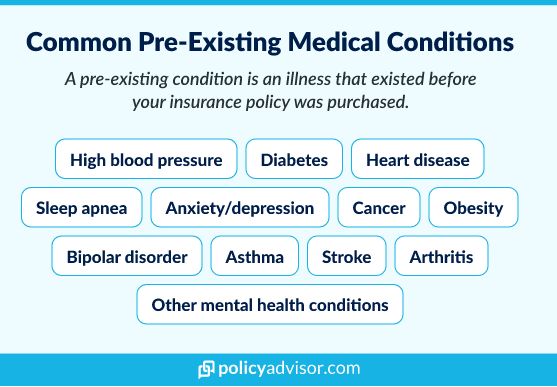

What is a pre-existing condition?

A pre-existing condition is an illness, health problem, or injury that someone had been diagnosed with before they applied for insurance. It can include serious illnesses, like heart disease, as well as illnesses considered mild, like sleep apnea. Even if someone has recovered from an illness, there is still a chance that it could be considered a pre-existing health condition.

Does a heart attack count as a pre-existing health condition?

Yes, if you’ve suffered from a heart-related illness like a heart attack before you applied for insurance, that is considered a pre-existing medical condition. Insurance companies pay close attention to this because it may mean the person applying could have more health problems in the future.

In Canada, the Heart & Stroke Foundation says there is a very high chance that someone who had heart disease will be affected by the same illness again. When someone who has had heart disease applies for insurance, the insurance company thinks about how likely it is that the person will have heart disease again. They know that the person is at a higher risk for it, and they may not want to take on that risk.

But keep in mind that just because someone may have a pre-existing condition, it doesn’t mean they cannot get life insurance. Even if someone is recovering from a severe illness, there are still options available.

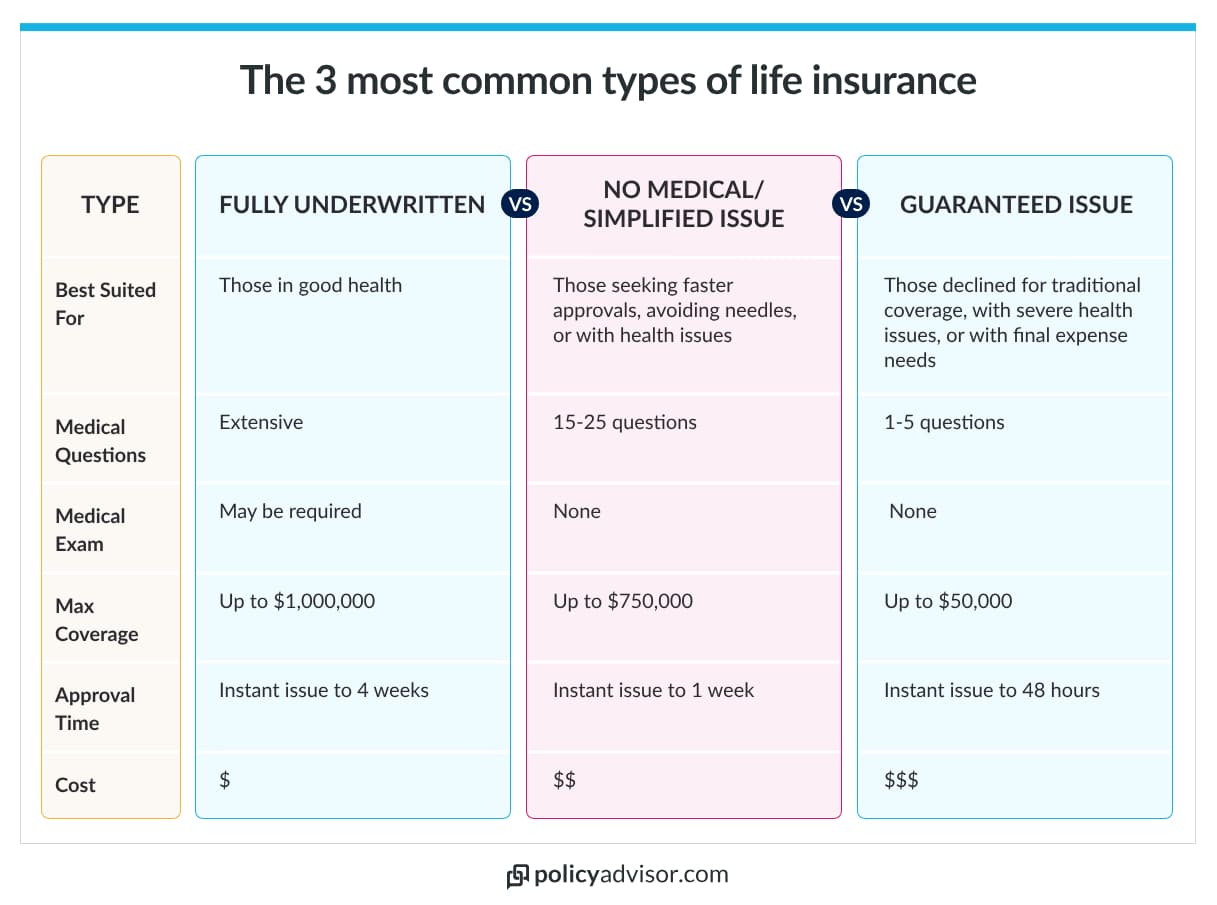

Which types of life insurance can you get after a heart attack?

Someone who’s had a heart attack may be able to get:

It just depends on each person’s unique circumstances. Let’s take a look at each of these common types of life insurance and which options may be possible for heart attack survivors or those who may have other heart issues.

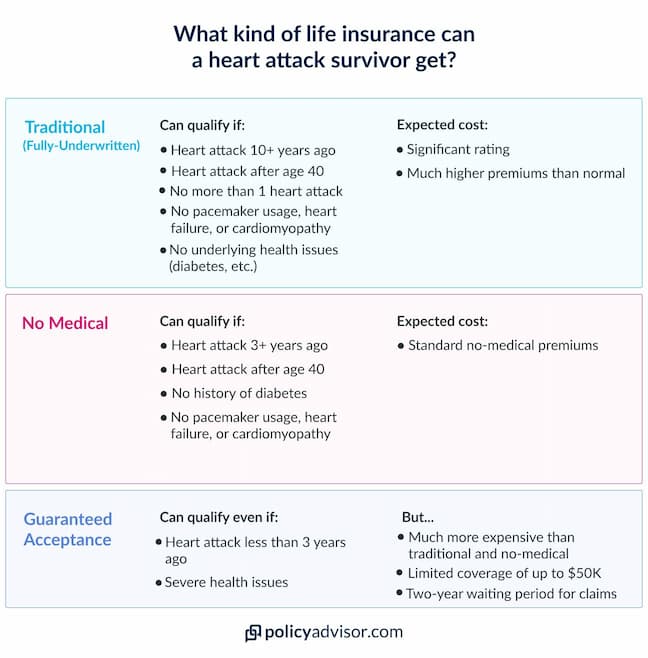

1. Traditional Life Insurance

Regular life insurance plans may not be a feasible choice for some heart disease patients and survivors. Heart disease is a serious illness that affects your life expectancy, and chances of the disease coming back can be high. This makes it more risky for traditional life insurance providers to give you insurance, so they may likely say no.

Most traditional insurance providers will NOT approve your application if you meet any of the following criteria:

- Your heart attack or treatment happened less than 5 years ago

- You had a heart attack when you were under 35 years old

- You’ve had more than 1 heart attack

- You have a particularly concerning heart condition (congestive heart failure, cardiomyopathy, or systolic/diastolic heart failure)

- You have or had a pacemaker

- Your diagnosis was severe or you have other underlying health issues that could make heart disease worse (such as diabetes, obesity, or another comorbidity)

In the most optimistic cases, someone who had just one heart attack more than 10 years ago could try to apply for traditional life insurance if their treatment has gone well and the heart attack was not caused by underlying health issues. In this kind of scenario, they may be able to get traditional life insurance.

The caveat is that premium costs will be significantly higher than normal. This is called a “rating.” The insured person could end up paying twice the standard rates. However, they would get the benefit of the flexibility and multiple coverage options that traditional life insurance provides.

2. No-Medical Life Insurance

If someone with heart conditions is unable to get traditional life insurance, there’s still a good chance that they can get no-medical life insurance or simplified life insurance. These types of policies are a bit easier to get because they have fewer medical questions and usually do not require a medical exam. The kind of coverage non-medical life insurance provides is more limited than traditional life insurance, and it’s often more expensive. But many people with pre-existing health conditions, or those who just want to avoid doing a health test, opt for no medical coverage because they’re more likely to get approved.

However, keep in mind that no-medical and simplified coverage may still not work out for people with a history of heart issues. You will still ask a series of health questions, and your application could still be denied based on your health history. For example, if you meet any of the following criteria, you may be denied:

- Your heart attack was less than 3-5 years ago

- You had a heart attack when you were under 40 years old

- You have a particularly concerning heart condition

- You have or had a pacemaker

- You have other underlying health issues that could make heart disease worse

As you can see, the requirements aren’t as strict as traditional life policies. But, your approval will still depend on these factors and similar conditions.

3. Guaranteed Acceptance or Guaranteed Issue Life Insurance

The good news is that, if all else fails, people with heart conditions can still fall back on guaranteed acceptance life insurance as their final option. This type of insurance coverage does not require medical tests and does not ask health-related questions. If you apply for this type of policy, your acceptance is pretty much guaranteed once you meet basic requirements like age and citizenship/residency.

But there are several downsides to this type of coverage:

- Price: Guaranteed acceptance policies are way more expensive than both traditional and no-medical life insurance.

- Waiting period: If you’re approved for this type of policy, most providers will not cover death due to natural cause for at least 24 months after the plan starts. While they will still cover accidental death, they will not pay the death benefit to your loved ones if you were to pass away from a natural cause within that timeframe.

- Limitations: Guaranteed acceptance has the most limited options of the three types of life insurance we mentioned above, so you might only get the most basic coverage.

Because of these downsides, although guaranteed acceptance may be easy to acquire, it’s often only used as a last resort in the most dire circumstances. The silver lining is that it lets even people with severe health issues give their families some kind of financial protection. But unless your health situation is that severe (and we hope it’s not), no-medical coverage would likely be a better option.

The best way to find out what type of life insurance you’re eligible for is to speak with a licensed life insurance agent or advisor who can look at your personal circumstances one-on-one to help you decide. Schedule a call with one of our advisors today if you’re unsure or if you’d like more insight on which insurance option would best suit your needs.

Does life insurance pay out if someone dies from a heart attack?

In most cases, yes, standard life insurance policies will pay out if someone dies from a heart attack. This is because it usually counts as a natural cause along with other conditions like:

Which types of life insurance cover death from a heart attack?

As we noted, most types of life insurance cover heart attack. This includes:

- Traditional life insurance

- No medical life insurance / simplified life insurance

- Guaranteed acceptance life insurance

Generally, getting a death benefit payout isn’t the issue when it comes to heart attacks. If someone who already has insurance dies from a heart attack, their family probably won’t have an issue getting their insurance money. The issue may be setting up the insurance in the first place if that person has had a heart attack. It’s also why the expert advisors at PolicyAdvisor are here to help!

Frequently Asked Questions

Does life insurance cover other types of heart conditions?

As we’ve seen in this article, the answer to this question depends. But if you do not have a life insurance policy already, your likely best option would be no-medical coverage if you’ve suffered from cardiovascular conditions like:

- Cardiomyopathy

- Coronary disease

- Heart murmur

- Heart failure (systolic, diastolic, or congestive)

- Heart attack

- Congenital heart defects

- Cardiac ischemia

- Heart surgeries (open-heart surgery, triple-bypass surgery, heart transplant, etc.)

Death caused by these types of illnesses count as a “natural death” for most existing life insurance policies. So, if someone already has a policy, they don’t have to worry — their loved ones will probably still get the insurance money even if they pass away from a serious heart health event.

How much does life insurance cost after a heart attack?

The exact cost of life insurance depends on factors like age, gender, type of policy, amount of coverage, and more. Traditional life policies typically have the most affordable rates, but the insurance company could assign a rating that makes premiums much higher. No-medical and simplified life insurance have higher rates than standard life insurance policies. And guaranteed acceptance life insurance is usually the most expensive.

You can easily compare instant quotes for traditional life insurance and no-medical or simplified life coverage on PolicyAdvisor through our online tools. We work with more than 30 of Canada’s best life insurance companies to provide you with competitive quotes that you can browse at the click of a button. Or you can contact us if you’d prefer to have an expert help you along!

How long after a heart attack can you apply for life insurance?

How soon you can apply for life insurance after surviving a heart attack depends on what type of plan you want to apply for. Here’s how long you should wait to increase your chances of being approved:

- Traditional Life Insurance: at least 5-10+ years

- No Medical Life Insurance: 3-5 years, depending on the provider

- Guaranteed Acceptance Life Insurance: you can apply right away

Note: Even if you wait to apply, your application could still be denied based on other factors like the severity of your condition.

Is a heart attack considered a critical illness?

Yes, a heart attack is considered a critical illness. But critical illness insurance and life insurance are different types of policies that cover different things.

Critical illness insurance is a living benefit that’s meant to help replace lost income if someone is recovering from a life-threatening illness. Life insurance only provides a death benefit to someone’s loved ones if/when they pass away.

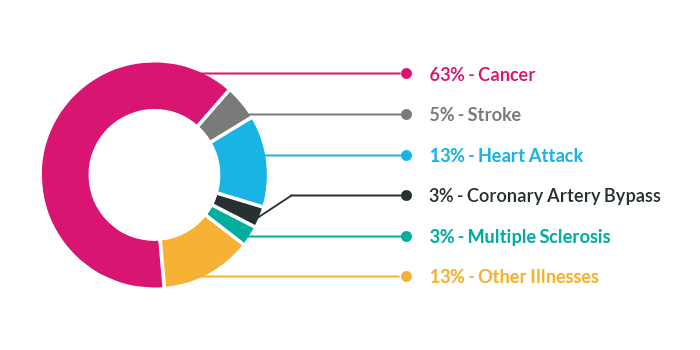

Critical illness insurance absolutely covers heart attack. And, it’s one of the reasons why we recommend this kind of coverage so strongly. Heart disease is the second leading cause of death in Canada, just behind cancer (source: Statistics Canada). With such high chances that you could be diagnosed with one of these illnesses, having financial coverage in place can give you peace of mind just in case the worst happens.

Just as with life insurance, though, it may be difficult to get critical illness coverage after you already had a heart attack. In this case, guaranteed acceptance critical illness insurance may be the only option available.

Read the full list of health conditions covered by critical illness insurance.

Is heart attack covered under accidental death insurance?

No, heart attacks are not covered under accidental death insurance or AD&D insurance (accidental death & dismemberment). This kind of insurance pays out either to the insured person or to their loved ones if a serious accident happens that causes death or a serious injury, like losing a limb, becoming paralyzed, loss of sight, etc.

AD&D coverage is important because accidental death is the leading cause of death for Canadians under age 45 (Statistics Canada). But, this kind of insurance does not cover life-threatening illnesses — that’s what critical illness insurance policies are for. So, even though heart attacks can be thought of as accidental (surely, no one plans to have one!) they’re not covered under accidental death insurance.

Get help with finding the right policy

Each situation is unique, so the best way to find the best life insurance for someone who’s had a heart attack is to speak with our insurance agents for expert guidance. They can assess your needs and help you find the most affordable life insurance options that would work for you and your family.

Heart disease is common in Canada, but there’s a lot of uncertainty about whether heart attack survivors can be insured. Or whether the insurance company would pay out for a heart attack. The good news is there are many life insurance options for someone who has survived a heart attack, and most life insurance companies will pay out for related death.