- Insurance rates are based on complex actuarial tables

- A rating is applied after you are approved for coverage but can dramatically change your premiums

- A rating is not always permanent. A change in lifestyle and improving your overall health can help revise your rating and qualify for lower rates

- If you receive a high rating, going for a no-medical policy may be a better alternative

Most people want to ensure that their loved ones are taken care of long after they’ve passed. One of the best ways to do this is by purchasing life insurance. That way, in the case of death, your beneficiaries will receive a lump sum they can use to settle your estate, help clear the mortgage, pay for your childrens’ education costs, and more.

How much coverage you will qualify for, as well as how much you’ll spend each month on premiums, all depends on your insurance rating, also known as a risk classification.

Insurance rates are based on complex actuarial tables which consider a host of variables to predict the mortality rate of any given individual. This mortality rate is then combined with the length and type of the policy and a rate is defined for the individual applying for insurance.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

Thus, when someone applies for life insurance, there are four possible outcomes:

- A policy is issued at a standard or preferred rate

- A policy is “Rated” or the customer is given a “Rating” and the policy is issued at a higher premium

- The policy is deferred or postponed pending further information

- The policy is outright denied as the applicant is deemed uninsurable

This article focuses on the second outcome: insurance ratings. We explain what an insurance rating is (and in turn, a rated policy or a rate-up policy) and your options when faced with a rating.

What does it mean to be rated for life insurance?

As part of your application for life insurance, you’ll have to go through an underwriting process that may result in a rating. Underwriting is basically how an insurer determines your risk factor. Each of Canada’s biggest life insurance companies has its own underwriting guide, which is basically a manual describing how applicants are evaluated.

Medical underwriting is one part of the underwriting process; it looks at an applicant’s medical history and if there are any unusual events in the immediate family’s medical history. Depending on the amount of insurance, age and preliminary investigations, underwriters could request a more detailed evaluation. The evaluation could require blood samples, physical examinations, and doctor’s notes in addition to interviews, and written or digital questionnaires you complete with your insurance advisor or paramedical personnel.

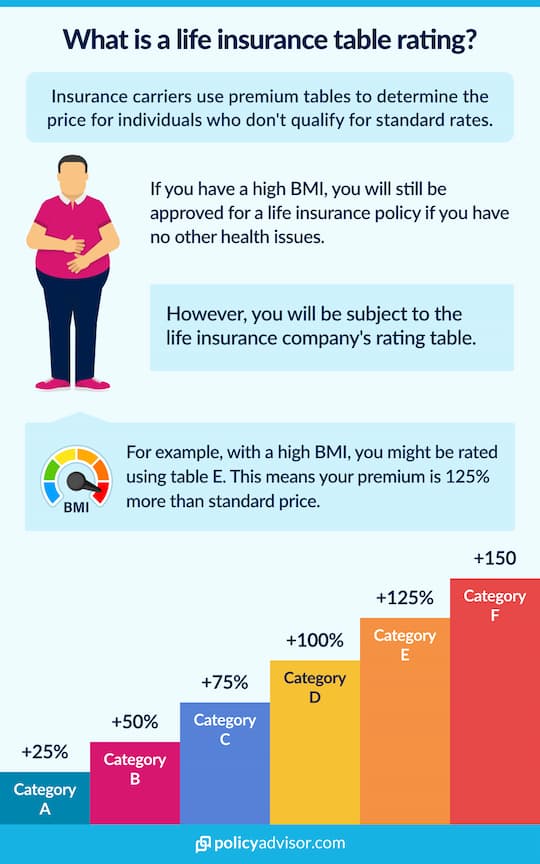

Based on this data, underwriters may assign the applicant their rating, impacting the premiums for the policy. If the underwriters determine the applicant is in substandard health, they are considered to be at an elevated risk level. However, there is a moderately broad range that qualifies as standard. If the applicant is in better health than standard they may receive a preferred (lower) rate; but, if they are on the other end of the health spectrum but still considered insurable, they may receive a rating.

What are the reasons you can get a rating?

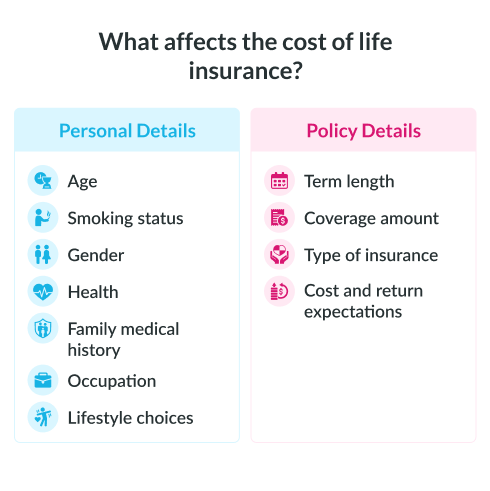

Insurers look at multiple criteria when determining your rating. Here are some of the items they consider:

- Health: Insurers are very concerned about the status of your health. They’ll want to know about any existing medical conditions, if you’re on medication, and how you’re treating any health issues. They’ll also want to know whether or not you’re a smoker.

- BMI: Insurers will ask for your height and weight so they can calculate your Body Mass Index (BMI) measurement. If by that standard, you’re considered underweight or overweight, you may be given a higher insurance premium.

- Family health history: Aside from asking about your own health, insurers will want to know about your family’s health history. So, if your mother has been diagnosed with diabetes or your father suffered from heart disease, unfortunately, that could be a strike against you in terms of your insurance rating.

- Alcohol and drug use: A casual drink with friends is not going to raise your insurance rates. But, if you have a history of abusing drugs and alcohol, this can give you a higher risk classification. In the past, people who smoked marijuana were rated higher because they were considered smokers. Now that cannabis has been legalized, light marijuana use will not affect your premium. However, regular cannabis consumption will be treated the same as smoking in most instances. Read more about marijuana and life insurance.

- Lifestyle: The kind of life you lead also impacts your premiums. If you’re a daredevil into skydiving or other hazardous activities, that can increase your rates. The same applies if you participate in a lot of international travel. If you travel fairly often to a country deemed as unsafe, insurers may raise your rating because you’re exposed to a higher risk of death.

Does an insurance rating affect your future insurability

If an insurer feels like they’re taking on too much risk to cover the risk of insuring your life, they can deny you coverage. However, all is not lost. You can always try applying through another company that may assess ratings differently, or offer insurance to a wider spectrum of applicants.

It is important to note: insurance companies share information through an organization named the Medical Information Bureau (MIB).

North American insurance companies share limited information regarding insurability of an applicant through the MIB. They do this to enhance transparency and consistency of information between the companies. In rare cases, the information the MIB provides prevents applicants from holding too many policies simultaneously or providing false information to get insured by one company after getting declined by another.

Thus, if you are a heavy smoker and are declined for coverage by one company you cannot go to another claiming non-smoker status.

You can also gauge your no-medical life insurance options. Instead of taking health tests and exams, you simply answer a medical questionnaire with your life insurance advisor. This can be helpful for those who have greater health struggles or other factors that may affect their insurance rating.

The downside, however, is that the insurance premiums could be significantly higher than a standard rated fully underwritten life insurance policy. But, if an applicant has health concerns that may lead to a rating, no-medical life insurance provides an option that can result in lower premium than the rated one.

Can you change your insurance rating?

If you are able to make changes to your health and lifestyle, it is possible to change your insurance rating over time. It will require drastic measures, though, such as quitting smoking, losing weight, dropping your cholesterol and/or reducing your blood pressure, and sustaining these changes for a period of time – typically two years. Typically, if there is potential for reconsideration of one’s rating, an insurance company will specify what steps should be taken or timelines to follow (such as: “”reconsideration after a weight loss of 35lbs or more maintained for 1 year“).

Since insurance premiums increase over the years, it may not be your best bet to hold off buying life insurance until your health has improved. What you think you’ll be saving may be offset by how much premiums increase as you age.

The safer bet is to secure the coverage you can now and apply again for reconsideration or a new policy once your health factors improve – it’s perfectly normal to hold more than one life insurance policy while you decide which coverage you should keep, should you qualify for more down the line.

What are your options if you have been rated?

So, you’ve been given a rating and your insurance options aren’t looking too good. What now? Well, there are a couple of different strategies you can try as mentioned above.

First, you can apply for insurance with another insurance provider. Every insurance company differs in terms of how they conduct their ratings, how their premiums reflect those ratings, and how much insurance coverage they will offer for certain rating classes.

Secondly, if your premium is beyond what you can reasonably budget for, consider lowering your coverage if that’s an option so you can pay less each month.

Lastly, explore your guaranteed insurance options (simplified, guaranteed, no medical life insurance). The premiums may be higher than fully medically underwritten, but a simplified medical questionnaire may not touch on the specific issue that produced your insurance rating. Insurance companies like Canada Protection Plan, Empire Life, Industrial Alliance, and Humania offer simplified coverage options.

To learn more about insurance ratings, how they may affect you, and explore your options when it comes to coverage, speak to one of our experienced advisors.

An insurance rating is a part of the underwriting process where you may be assigned a rating, an insurance rating determines your insurance premiums of your policy.