- Couples can save money on policy fees with joint coverage

- They can do this through joint first-to-die, joint last-to-die, or a combined life insurance policy

- Joint coverage is convertible to permanent coverage for a surviving spouse or partner

Nobody wants to think about their death, but the hard reality is that with ageing comes questions about those you may leave behind. This goes doubly so for couples. When you have a significant other, you both are invested in finding the best life insurance policy for couples. Finding coverage for the two of you provides peace of mind should anything happen to you both.

Life insurance is readily purchased by couples for various reasons: replacement for loss of income, mortgage protection, leaving behind an inheritance for future children and grandchildren, or any other need to alleviate the financial hardship their death can have on their partners or children. These scenarios require decision-making. Do you need term life insurance or whole life insurance? Should you add child life riders? How much life insurance do you need and for how long?

Married couples and common-law partners alike need to contemplate one more big life insurance decision. Should you apply together or get individual life insurance policies? Let’s dig into your choices when it comes to life insurance for couples and whether one should get a joint policy or apply buy individual coverage for each single person.

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

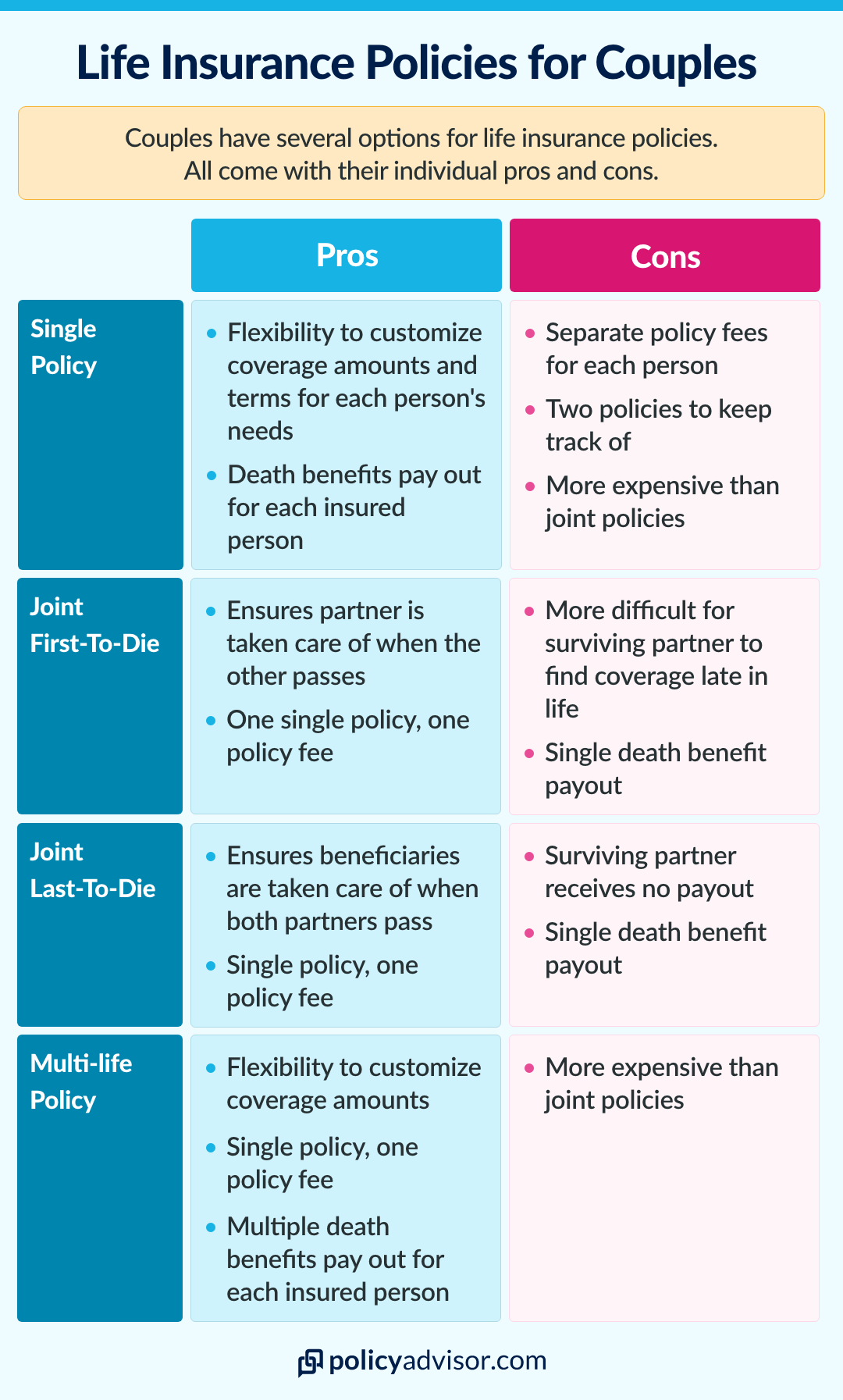

What are the different types of life insurance policies for couples?

There are mainly three types of life insurance policies or contract choices for couples searching for the financial security insurance offers. They are single life insurance (also known as individual policies or separate policies), joint first-to-die insurance, and joint last-to-die insurance. There is also an option for a “combined life insurance policy.” Similar to a joint life policy, this is one policy issued for both lives insured with a few differences.

Single life insurance policy

With a single life insurance policy, only one person is insured. The death benefit is paid out to a chosen beneficiary upon the death of that person – the policy owner. It is not tied in any way to a person’s marital status.

Keep in mind, if it is a term life insurance policy, the payout will be made if the death occurs during the term of the policy, the period of time you choose as your coverage length. If it is a permanent life insurance policy, there is no term, and the payout will happen whenever the life insured dies, as long as the policy is in force.

Joint first-to-die life insurance policy

Joint first-to-die life insurance covers the lives of two or more people (usually two). Under this type of life insurance policy, a single amount of coverage is placed on two or more insured lives, and the death benefit is paid out upon death.

Joint last-to-die life insurance policy

Joint last-to-die life insurance policy

Joint last-to-die life insurance policy

Joint last-to-die life insurance policySimilar to a joint-first-to-die policy, joint last-to-die life insurance coverage is placed on two or more lives insured (typically two). The difference lies in the time of payout. For a joint- last-to-die policy, the death benefit is paid out upon the death of the last insured person to die.

Combined or Multi-life insurance policy

A combined life insurance policy covers two people, typically spouses or life partners. Both can choose separate coverage amounts or coverage terms under such a policy. An insurance company may also call it a multi-life policy. The advantage is one saves money by paying just a single policy fee. Thus you benefit from the flexibility and personalization of an individual life insurance coverage, while also obtaining a discount on the policy fee.

Both joint and combined life insurance policies for couples are good options for those with budgetary constraints or looking to cover a common need (such as mortgage debt). They can get the coverage they need to secure a debt or cover living expenses while only paying a single policy fee.

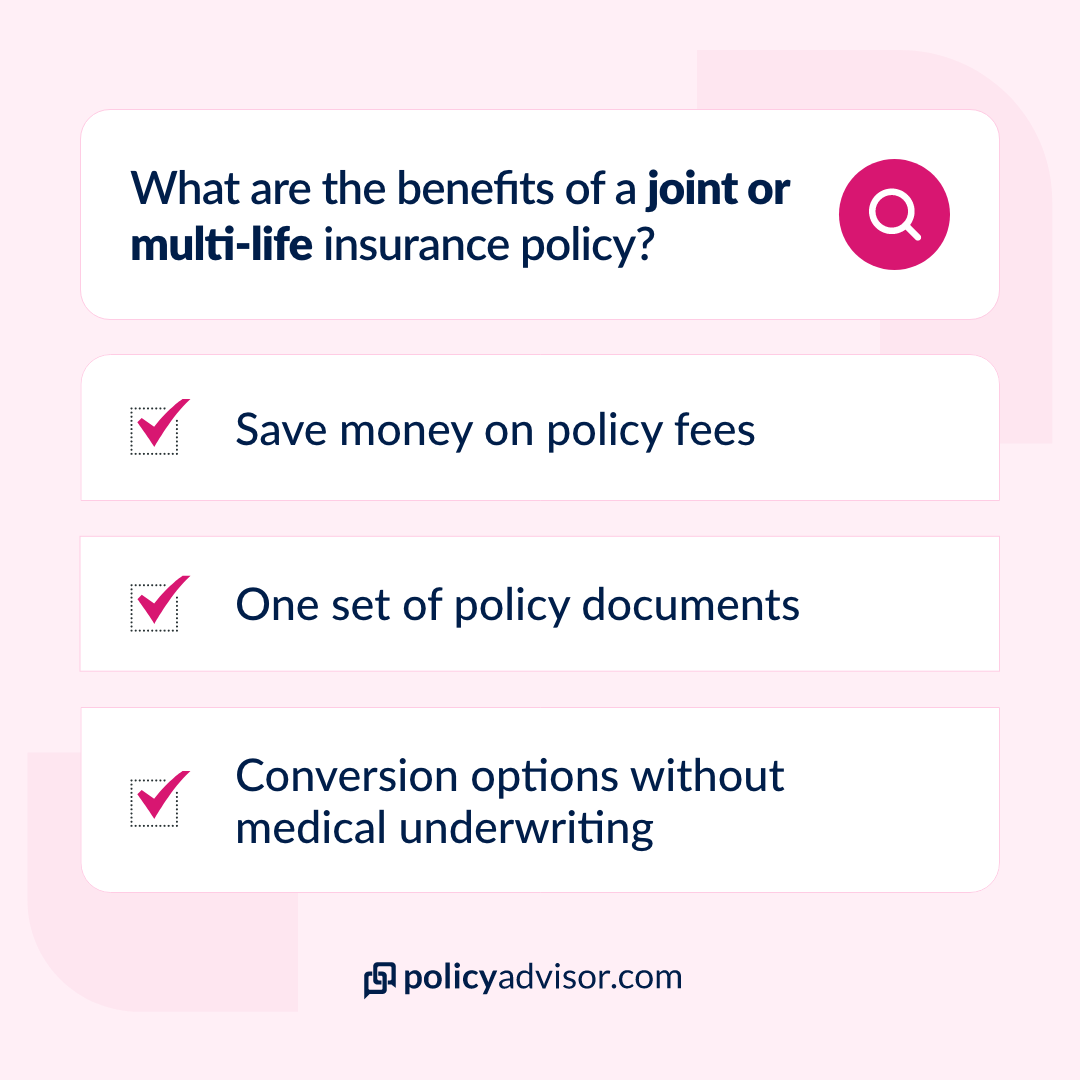

What are the benefits of taking one life insurance policy for couples?

Lower policy fees

As discussed above, combined and joint-life insurance policies allow a couple to take coverage under a single policy, which is a less expensive way of seeking life insurance as you pay a single policy fee.

For example: you and your partner recently bought a home and have taken out a joint mortgage to cover the cost. You secure your mortgage by taking a joint-first-to-die policy and avoid paying the two policy fees.

The joint coverage includes a single coverage amount; you both can decide this amount based on the outstanding mortgage and its amortization period. The benefit is paid out upon the death of the first insured person. The survivor can then use the money to pay off the mortgage loan.

A penny saved is a penny earned; why not save the extra policy fee while comfortably getting the protection you need? While the amount may seem nominal month-to-month, it can add up to hundreds, if not thousands of dollars saved over the course of the coverage period.

And, as mentioned earlier, you can determine separate coverage amounts and terms for each insured life with a combined policy. In this case, you can also ensure that coverage continues for the surviving spouse or partner if one passes away.

One contract to manage

Keeping track of paperwork and physical contracts on top of regular financial responsibilities can be a pain. With a single policy for a couple, only one contract is issued. You have the ease of reading, managing, and storing just one policy instead of two.

Conversion to permanent insurance

Typically, joint life insurance policies let the survivor convert their term policy into a permanent policy without medical underwriting upon the death of the other life insured as long as they are within the policy term. While not strictly necessary, it gives the surviving partner the option to cover themselves for their entire life. In the case of a multi-life policy, the conversion option is available on both the coverages within the unified contract.

What are the negatives of applying for life insurance as a couple?

We would be remiss to not mention the few disadvantages to life insurance for couples.

Joint policies do not have an option for splitting the coverage in two for any unforeseen reason. While we hope that every relationship lasts, the reality is that is not always the case. In the event you decide to end your marriage or relationship, you will not be able to split your joint policy. In such a case, you may likely have to cancel the joint policy, and both you and your partner will have to purchase new policies.

That said, most joint policies allow you to take individual life insurance coverage without undergoing medical underwriting upon divorce or dissolution. We cover the subject of joint versus single life insurance coverage in depth here if you are searching for more information about this particular situation.

Read more about life insurance and divorce.

Lastly, joint policies include only one death benefit and thus only pays out once. With a joint first-to-die insurance policy, if the survivor wishes to obtain new coverage it may not be easy to qualify later in life. And, if you do qualify, coverage will be more expensive in your later years.

When is the best time to apply for life insurance as a couple?

The best time to get a life insurance quote is always as soon as possible, as your rates will generally be less expensive in your earlier years. However, this is the easy answer. Couples have many trigger points that ad urgency to their life insurance needs. These can include moving in together, getting married, buying a home, getting a pet, or having children just to name a few.

Where can you get life insurance for couples?

While every couple’s situation and needs may vary, joint and combined policies are an excellent fit for those looking to save on money whilst getting the protection they require for their common needs.

Most of Canada’s best insurance companies offer various options for couples’ life insurance. Speak to our advisor today; they can discuss all the options at your disposal and help you choose the right policy and life insurance company for you and your partner’s needs.

Finding the right life insurance coverage for couples has a number of benefits, including the potential to save money on policy fees and the simplicity of managing a single policy. There are a few life insurance policy options that couples can choose from, such as joint first-to-die life insurance, joint last-to-die insurance, and combined or multi-life insurance.