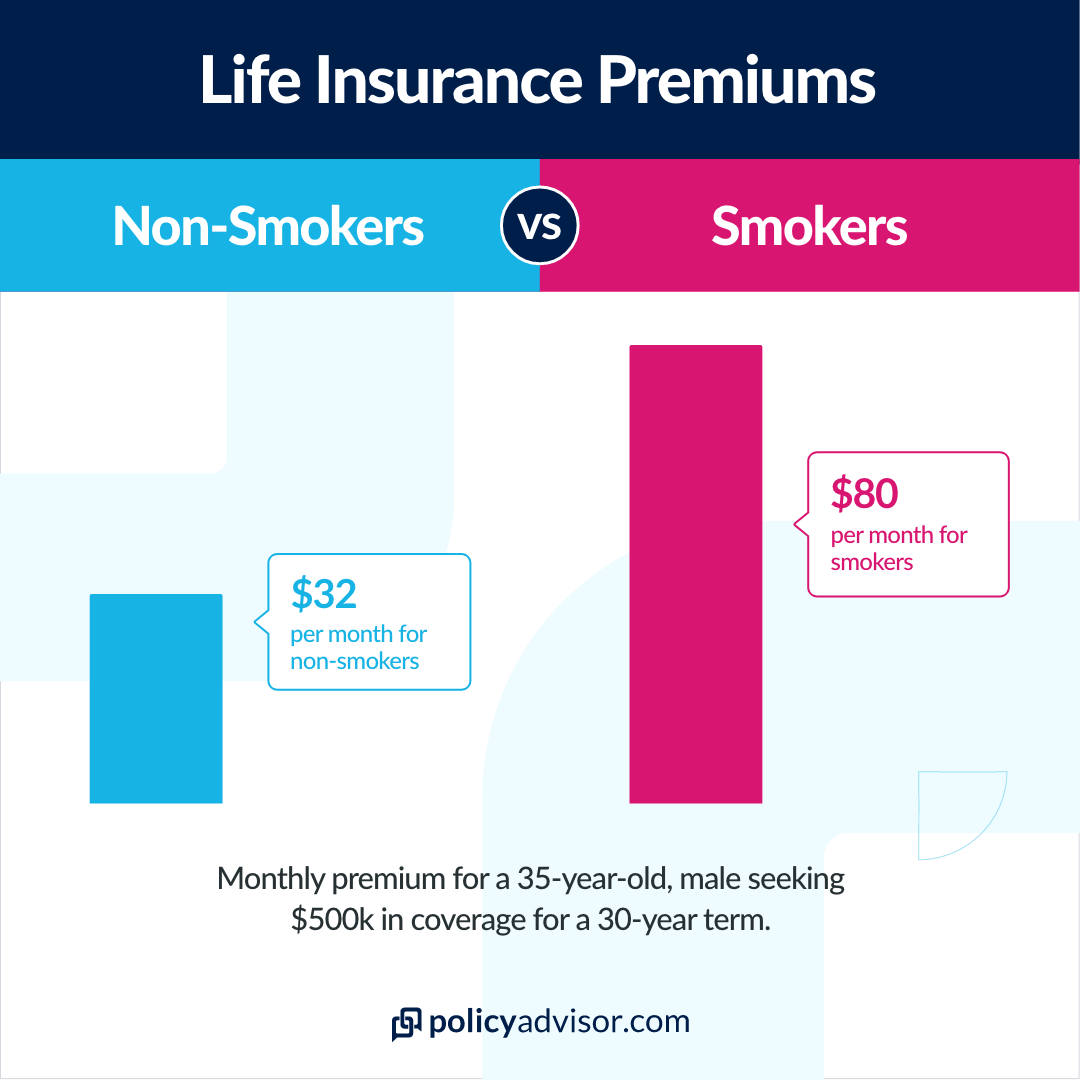

- Smokers are subject to higher life insurance premiums than non-smokers

- If you chew nicotine gum, you are considered a smoker in the eyes of most life insurance carriers

- You must have ceased smoking or using nicotine products for one year for most carriers to provide non-smoking rates

Life insurance premiums are based on a variety of factors such as your health and lifestyle choices. The healthier you are in the eyes of an insurance company, the lower your premiums will be. During the underwriting process, you will be asked a lot of questions about your lifestyle and health. Amongst other things such as medical history and exercise habits, you will be asked if you smoke.

Your smoking habits are a huge factor in determining premiums. This is because smoking has been linked to many health risks and medical conditions that impact your life expectancy such as:

- heart disease

- lung disease

- high blood pressure

- cancer

- stroke

As a smoker, you can expect the cost of life insurance to be much more expensive than it would be for a non-smoker. Premiums for smokers can be anywhere from 50-100% higher than non-smoker rates. If you smoke, vape, or consume any nicotine product, life insurers will consider you a smoker. This includes nicotine gum.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

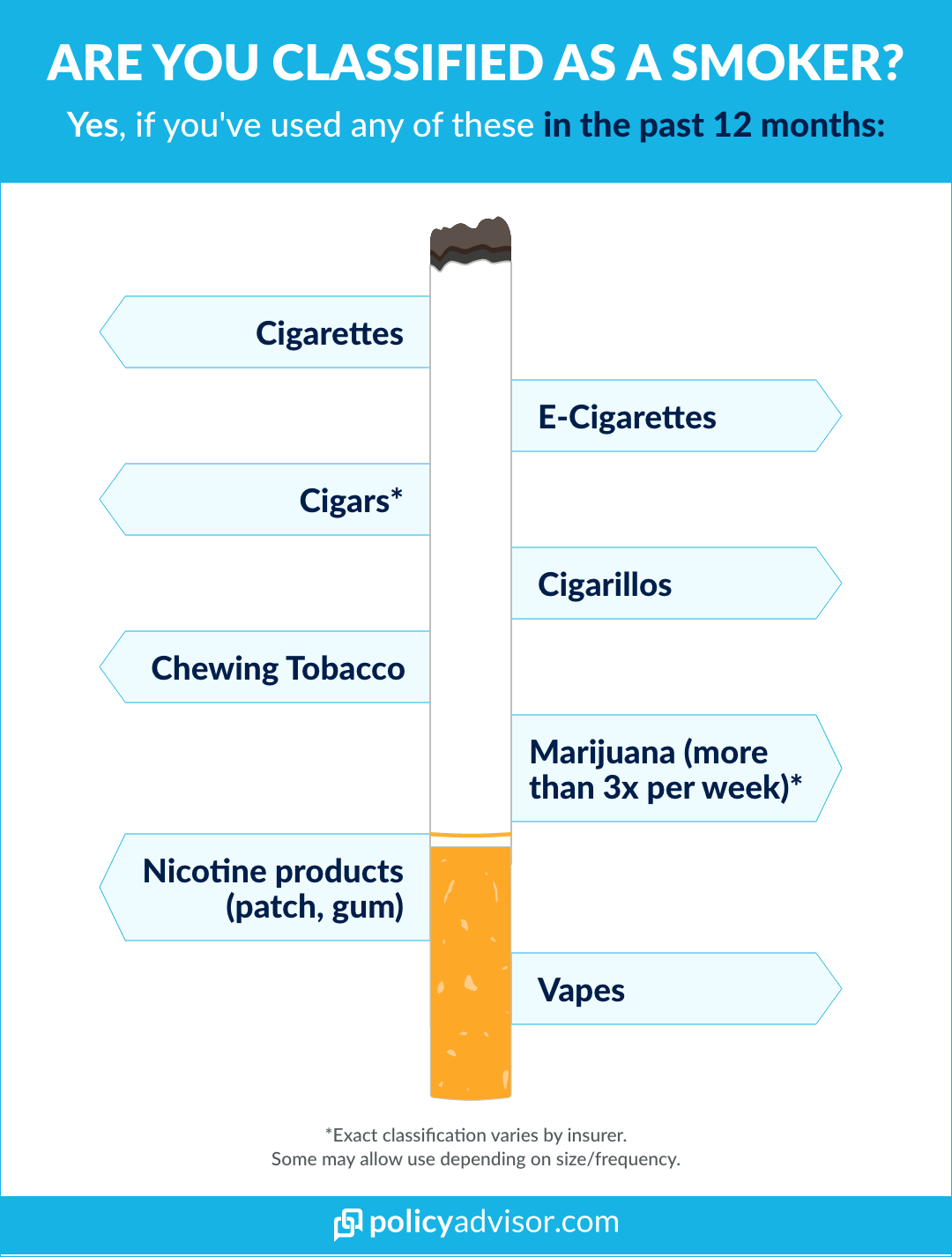

How do life insurance companies classify smokers?

You will be considered a smoker if you have consumed or used any of the following in the past 12 months:

- cigarettes

- chewing tobacco

- nicotine patches

- nicotine pouches

- nicotine gum

- hookahs

- electronic cigarettes

- vapes

In general, life insurance providers will not differentiate rates between heavy smokers or occasional smokers. Because of the health issues associated with smoking, you either are a smoker or you’re not.

However, there is some flexibility regarding cigar smoking. Some providers will allow you to smoke a celebratory cigar or two and still classify as a non-smoker as long as your average is less than one a month. Though, this does depend on the size and type of cigar or cigarillo.

Frequent consumption of marijuana, such as edibles or cannabis products, can also classify you as a smoker. This includes adding cannabis oil to a vape pen. However, rules around marijuana consumption will vary depending on your insurance provider.

Is nicotine gum considered a tobacco product for life insurance?

Yes, if you use nicotine gum or other smoking cessation products, the life insurance company will classify you as a smoker. Often people will start to use nicotine gum as a stop smoking aid to help reduce their craving for cigarettes. However, in the eyes of the insurance company, you have not fully quit smoking until you are no longer dependent on nicotine products.

Once you have been nicotine free for 12 months, you will be able to qualify for non-smoker rates on your life insurance.

What happens if you lie about smoking or using nicotine gum on a life insurance application?

On your life insurance application, you will be asked if you are a smoker—and you will be expected to answer honestly. Some insurance companies will require you to complete a medical exam as part of your underwriting process. Often this exam will include a urine sample, saliva, blood, or nicotine test. If any levels of nicotine are detected in your system at the time of application, you will be given smoker’s premiums.

How do life insurance companies check if you smoke?

Life insurance companies have many ways of checking your smoking history and status before, during, and after the life insurance application process.

Life insurance nicotine test

Life insurance companies will not just look for traces of tobacco or nicotine in your system during your medical exams. They will also look for an alkaloid called cotinine. Cotinine is found in the body after nicotine has been metabolized. So, even if you wait 3-4 days after using nicotine or other tobacco products, your test results will still give away your cigarette or nicotine gum use.

Life insurance contestability period

Even after the life insurance medical exam and application process is complete, your life insurance policy will have something called a contestability period. Generally, this will span the first two years of your policy.

If during this time it is found that you have lied about your smoking status or anything else on your application, the insurance company can retract coverage and cancel your policy.

On your application, it is always best to be honest even if it results in higher premiums. You don’t want your beneficiaries to be left without a death benefit in the event of your passing.

Checking your death certificate

If you are not required to submit a urine, blood, saliva sample, or nicotine test your insurance company may not know immediately that you are a smoker. But that doesn’t mean you’ve necessarily gotten away with it. If a claim is made on your policy after you pass away and it is discovered that you were a smoker at the time of application, the claim can be denied. This means that your beneficiaries will not receive your death benefit.

Does your doctor tell your insurance company if you smoke or use nicotine gum?

Your insurance company may require medical records or a report from your doctor, known as an Attending Physician’s Statement (APS). This APS would include your smoking status and smoking history.

Some types of life insurance, such as no-medical life insurance, do not require you to go through any medical exam or APS reports. If you did not have to submit medical records for your application, or your status as a smoker is not on your medical records, your doctor is not required to inform your insurance company of your status. In fact, as a medical professional, your doctor is legally required to keep your medical status confidential unless you consent to its release or your doctor is required by law to disclose it.

So, your doctor can’t tattle on you, per se—but if the insurance company wants to know your smoking status and you refuse to provide that information, they may decline your application.

How long after quitting smoking can you get life insurance?

You can get life insurance now, regardless of your smoking status. However, once you have been free of nicotine or tobacco products for 12 months, you will no longer be considered a smoker and receive non-smoker rates.

Life insurance providers require you that you have quit smoking and the use of other forms of nicotine replacement products for this period of time as your risk of smoking-related health issues reduces, meaning you are less of a liability for them to payout.

If you quit smoking and the use of all nicotine products for over 12 months, but you’ve already set up your policy, you can update your smoking status and apply for a lower life insurance premium. In this case, you will be required to submit a new medical report from a doctor confirming your non-smoker status.

Trying to quit smoking and looking for life insurance?

Even if you haven’t hit that 12-month-smoke-free milestone yet, we can still help you get affordable life insurance rates for smokers. To learn more about life insurance for smokers and your expected premiums, get a free life insurance quote or schedule a call with an expert insurance advisor.

One major price factor for life insurance is your smoking status—if you’re a smoker, you’re subject to higher rates. If you smoke cigarettes, vape, or consume any nicotine products like nicotine gum, you are considered a smoker. It usually takes a waiting period of one year after you quit smoking to get non-smokers rates.