Disability Insurance Quotes

Get instant quotes from 30+ insurers

Disability insurance quotes in Canada

Disability insurance provides monthly tax-free payments if you’re unable to work due to a covered illness or injury, helping you maintain your income and meet essential financial obligations during recovery. These benefits can be used however you choose, from paying your mortgage or rent and covering household bills to managing daily living expenses while you’re unable to earn an income.

With PolicyAdvisor, finding the right disability insurance is simple and convenient. Our platform lets you compare personalized quotes from Canada’s leading insurers in one place, making it easy to evaluate coverage options and premiums. By bringing everything together on a single platform, PolicyAdvisor helps you make an informed decision and choose a plan that matches your occupation, income, budget, and long-term financial security needs.

Sample disability insurance quotes in Canada

Disability insurance premiums vary based on income, occupation, age, and coverage structure. Here’s what typical monthly premiums can look like:

Monthly premiums for a male, non-smoker, in good health (90-day waiting period)

| Age | $5,000 monthly benefit (90-day waiting period) |

$10,000 monthly benefit (90-day waiting period) |

| 25 | $62.00 | $125.00 |

| 35 | $83.00 | $166.04 |

| 45 | $131.00 | $262.00 |

| 55 | $223.00 | $445.69 |

Is it better to get a disability insurance quote online?

Yes, getting a disability insurance quote online is one of the easiest ways to explore your coverage options. You can compare personalized quotes from multiple insurers, review monthly benefit amounts, waiting periods, and premiums, and evaluate different policy options without reaching out to each insurer individually.

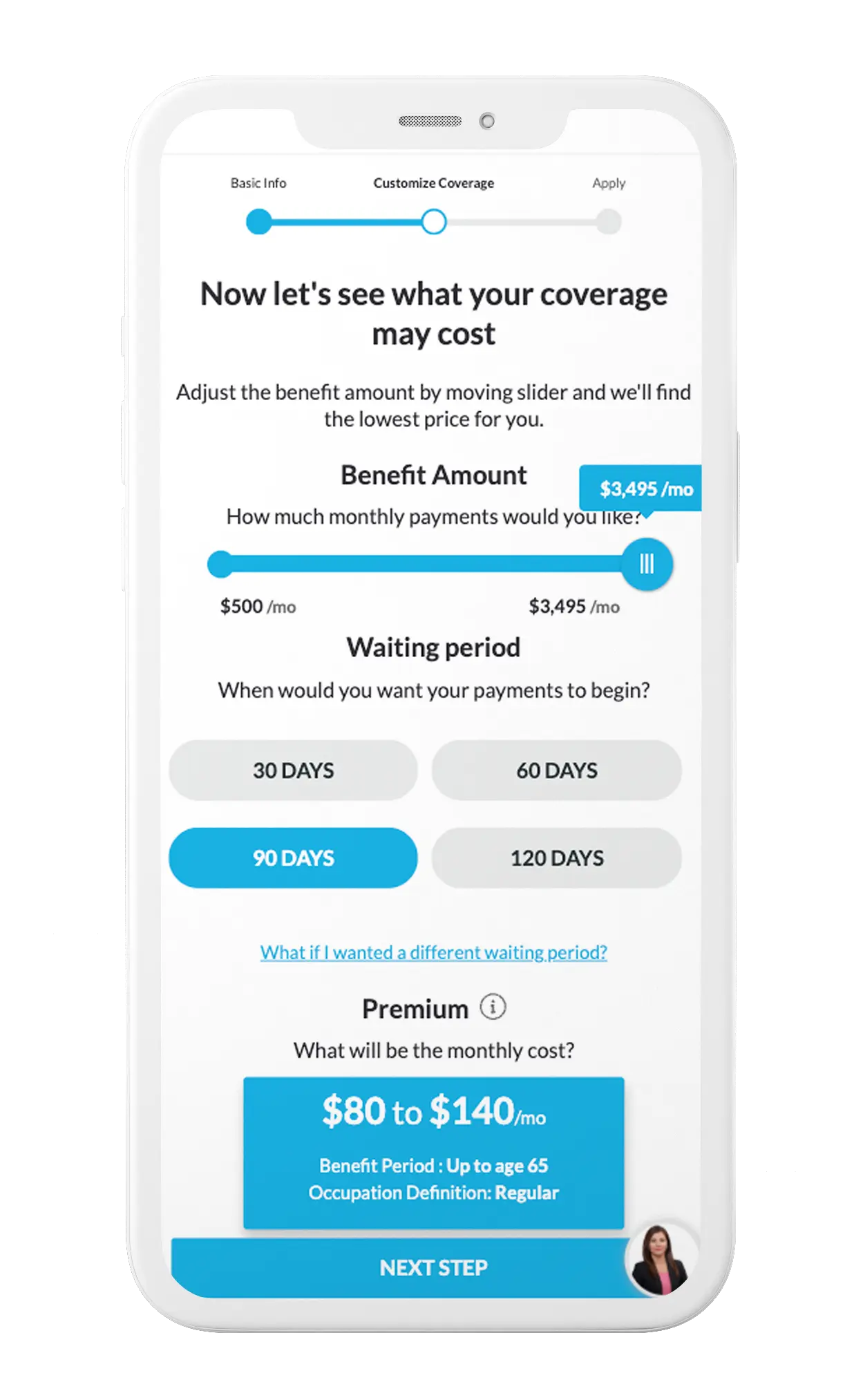

With PolicyAdvisor, you can compare disability insurance quotes, adjust your coverage to suit your income and occupation, and access expert advice from licensed advisors whenever you need assistance. This makes it easier to find the best disability insurance policy. Use the tool below to get your personalized quotes today!

Get a personalized quote in seconds

Powered by

![]()

How to get disability insurance quotes online in Canada

Here are the steps you need to follow to get disability insurance quotes in Canada:

Provide basic details

Provide age, income, occupation, and basic health information

Customize your coverage

Choose your monthly benefit amount, waiting period (when benefits start), and benefit period (how long they last)

Compare quotes instantly

Review plans from multiple insurers and select the coverage that fits your needs

Why choose PolicyAdvisor for a disability insurance quote in Canada

Getting a disability insurance quote shouldn't feel complicated. Here's why Canadians choose PolicyAdvisor:

No waiting for callbacks. No hidden pricing. Compare personalized insurance quotes upfront.

View multiple options side-by-side and find the best, most affordable option for your financial safety.

Your premiums stay fair and clear.

Explore your options without any pressure to buy.

Start your quote online in minutes and complete your application seamlessly.

Have questions? Speak to a licensed advisor for guidance anytime you need it.

Still not sure where to start with your disability insurance quote?

Check out this video and let our licensed advisors help give you an idea!

How can I get the lowest disability insurance quotes in Canada?

Disability insurance quotes are heavily influenced by how your policy is structured. Adjusting a few key elements can significantly reduce your premium.

To find lowest rates, simply compare the best disability insurance quotes online using PolicyAdvisor’s easy tools. Or, you can simply talk to one of our licensed insurance advisors. We can help assess your unique situation and find the best-priced insurance policy.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them.

Short-term vs long-term disability insurance quotes

Whether you need short-term or long-term disability insurance depends on how long you want your income protected if you are unable to work. Here’s how the two types of coverage compare:

| Feature | Short-Term Disability (STD) | Long-Term Disability (LTD) |

|---|---|---|

| Coverage duration | Typically up to 17, 26, or 52 weeks | 2 years, 5 years, or up to age 65 |

| Purpose | Covers temporary inability to work | Covers long-term or permanent disability |

| Income benefit | Weekly income replacement | Monthly income replacement |

| Waiting period | 1 to 14 days before benefits begin | Begins after STD or a longer waiting period (e.g., 90+ days) |

| How it’s offered | Often provided through employers | Commonly purchased individually or as a supplement |

| Common use cases | Injuries, infections, short-term recovery | Chronic conditions, serious injuries, long-term disabilities |

Customize your disability insurance coverage

No two disability insurance policies are the same, which is why it’s important to choose coverage that matches your income, lifestyle, and financial responsibilities. With PolicyAdvisor’s quote tool, you can customize key policy features such as your monthly benefit amount and waiting period, then instantly see how those choices affect your estimated premium.

Whether you are looking for affordable income protection or more comprehensive coverage, our platform helps you compare personalized disability insurance quotes from Canada’s leading insurers in one place.

Which companies provide disability insurance quotes on PolicyAdvisor?

We show you quotes from the best disability insurance companies in Canada. This includes some of the most trusted insurance providers, such as:

Frequently Asked Questions

How much income does disability insurance replace?

Most disability insurance plans replace 60% to 85% of your income, depending on the insurer and policy structure.

What is the difference between life insurance and disability insurance?

Life insurance pays a tax-free death benefit to your beneficiaries after you pass away. Disability insurance, on the other hand, pays a monthly benefit if you become unable to work because of a covered illness or injury. While life insurance protects your loved ones, disability insurance protects your income during your lifetime.

What is the difference between “own occupation” and “any occupation”?

“Own occupation” means you receive benefits if you can’t perform your specific job, while “any occupation” requires you to be unable to work in any job suited to your skills and experience.

When do disability insurance benefits start?

Benefits begin after the waiting period (elimination period), which can range from a few days to several months depending on your policy.

Can I get disability insurance if I’m self-employed?

Yes, disability insurance is especially important for self-employed individuals, as it provides income protection without employer coverage.

What conditions qualify for disability insurance?

Disability insurance covers illnesses or injuries that prevent you from working, including both physical and mental health conditions, depending on the policy.

Can I have both short-term and long-term disability insurance?

Yes, many people use short-term disability for immediate coverage and long-term disability for extended income protection.