- Critical illness insurance and disability insurance are two different products that work differently, but complement each other well

- Where you need one over the other or both is determined by the policyholders specific needs

- CI pays a lump sum of money that you can use to pay for medical expenses, home modifications, or anything else as you recover

- DI pays regular monthly payments meant to pay for costs like your mortgage/rent and daily living expenses until you recover

Critical illnesses insurance vs disability insurance can be easy to mix up. They have a lot in common, and can both deal with your ability to earn a paycheque.

Sometimes, people who have insurance believe that because they have one type of policy, they’re covered for everything. But that’s not the case. In this article, we look at the difference between critical illness insurance and disability insurance.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What’s the difference between critical illness vs disability insurance?

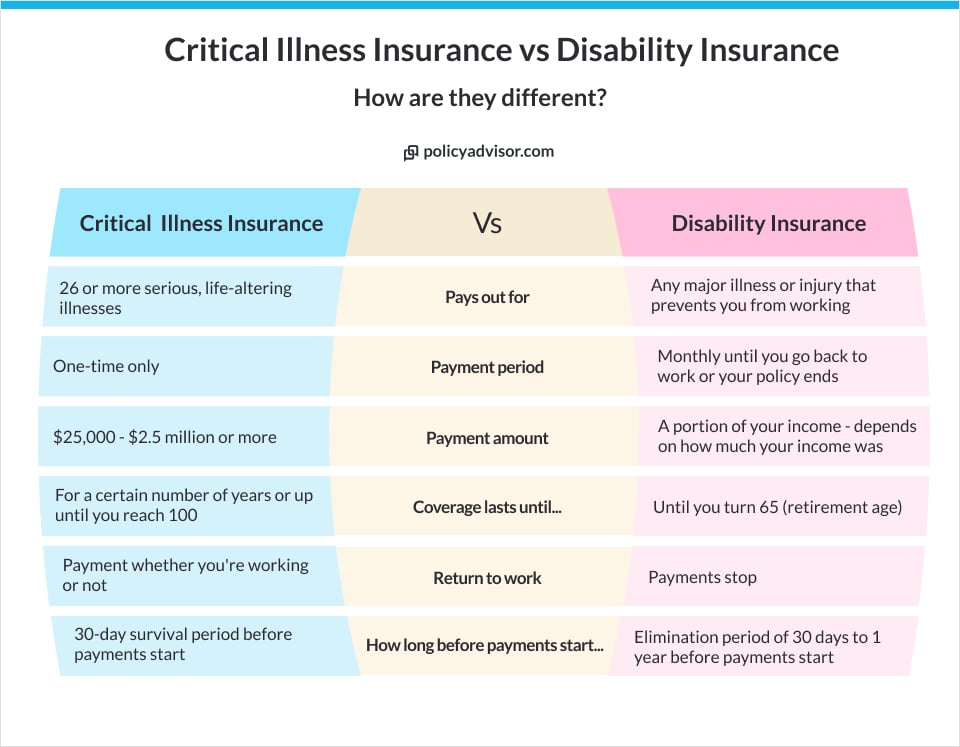

Disability insurance (DI) and critical illness insurance (CI) cover different things and give payouts in different ways. They both give you money if something happens to impact your health, and you are no longer able to work.

The primary difference is that critical illness insurance only pays out one time. Disability insurance gives you monthly payments until you get better and can return to work.

The chart below shows some of the main differences and similarities between DI and CI.

Key differences between critical illness insurance vs disability insurance

| Aspects | Disability Insurance | Critical Illness Insurance |

| Claim event(s) | Any illness or injury that leads to a loss of income | Diagnosis of a covered life-threatening illness or condition (severe disability may be included) |

| Covered conditions |

Any medical condition that would prevent you from working, including:

|

26+ common conditions, including:

|

| Benefit amount (how much your payout would be) | Replaces a part of your monthly income | $25K – $2.5M+ depending on your policy |

| Payment frequency | Monthly payments | One or more lump-sum payment(s) |

| Benefit duration | Until you recover or your policy lapses (can last until you reach 65 or older) | One time only |

| Coverage term | Most policies end when you turn 65 | You can get coverage up to age 100 |

| Return to work | Monthly payments stop once you return to work (although partial payments may be available) | Payout is not tied to work — you are paid out whether you are working or not |

| Period before benefits begin | Waiting period (or elimination period) of 30 days to 1 year | Survival period of 30 days |

| Income replacement | Meant for ongoing income replacement | Not meant as income replacement, but can help |

Do I need disability insurance if I have critical illness insurance?

It depends. Both policies can help protect your income and savings if something serious happens to health and stops you from working. But they work best in different situations.

Whether you need just one or the other, or both, depends on your needs, age, and other factors. The policies do complement each other very nicely and give you a well-rounded way to protect your income.

The best way to figure out which one you need is to speak with our licensed insurance agents. We’re friendly and experienced, so we are happy to help you assess your needs.

What is a critical illness insurance policy?

Critical illness insurance is a type of insurance that gives you a tax-free, lump sum of money if you become sick with a certain illness or need serious medical treatment.

It gives you the peace of mind to focus on recovering without worrying about how you’re going to afford the things you need.

You can use a critical illness insurance payment for anything you need. But most people use it to pay for costs while they recover. That can include out-of-pocket medical treatment, house cleaning, or even a gift basket for your neighbours if they watered the plants while you were in the hospital – the choice is yours.

Key features of critical illness insurance are as follows:

- Benefit amount: $25,000 to $2.5 million or more — decided by you and your insurance provider when you buy the policy

- Payment: One-time tax-free lump sum (some companies will pay out on more than one occasion, ex. if you get the same serious illness twice after a period of time)

- Beneficiary: The insured person (you)

- Requirements: 30-day survival period — you must survive for at least 30 days after diagnosis for the insurance company to pay you

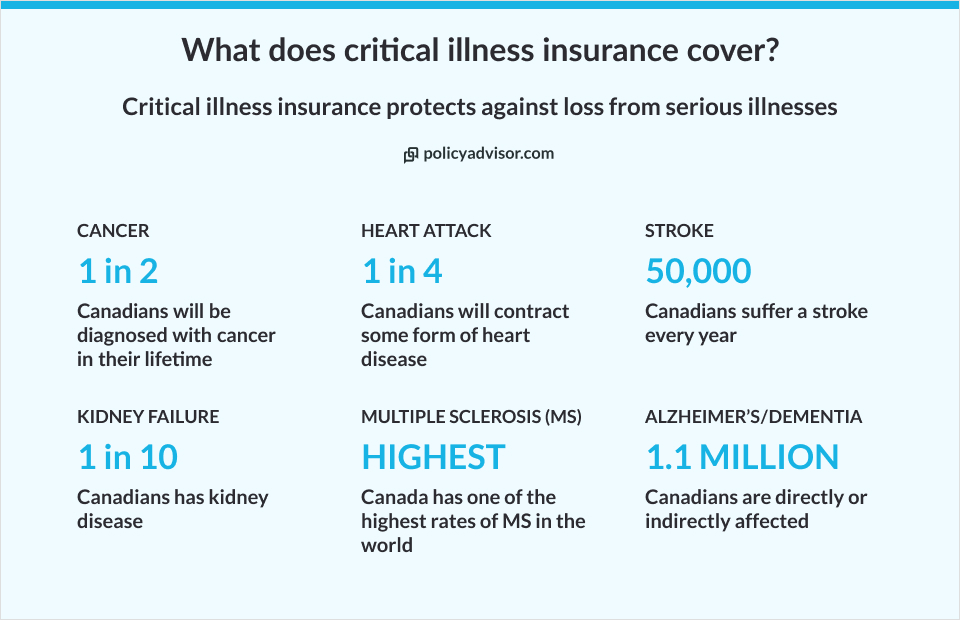

What does critical illness insurance cover?

A critical illness plan will typically cover 26 or more types of diseases in Canada, like cancer, heart attack, kidney failure, and more.

Sometimes, a disability may count as a critical illness. For example, blindness and paralysis are disabilities that are also critical illnesses.

What is a disability insurance policy?

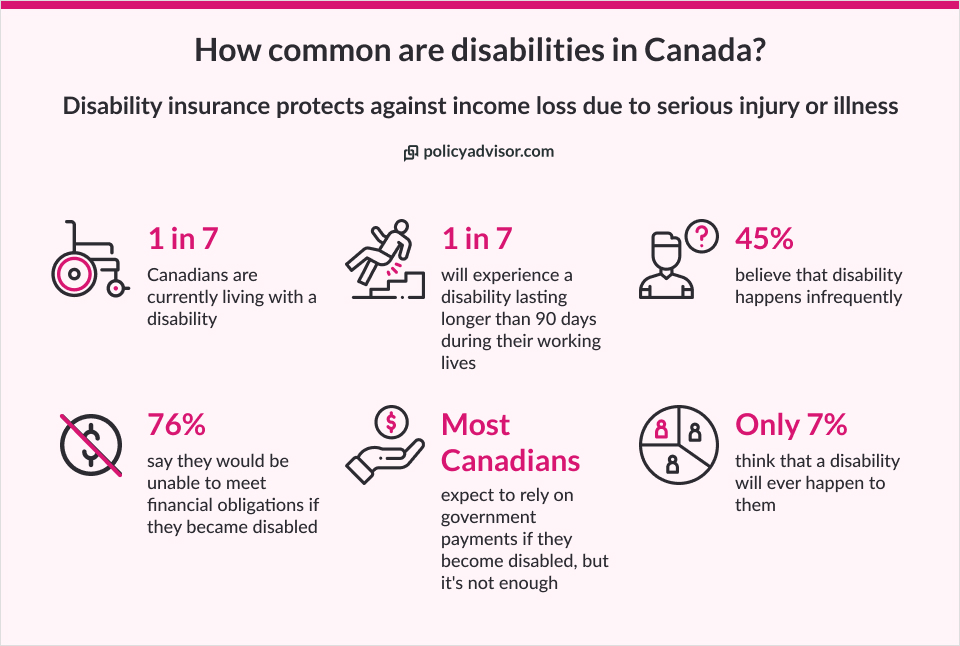

Disability insurance is a type of insurance that gives you monthly payments if an injury or illness affects your ability to work. It’s meant to replace the income you lose while you’re recovering. You may also see it called disability income insurance.

There are two different types of disability insurance coverage: short-term or long-term. Long-term disability usually kicks in if your disability lasts longer than the short-term disability insurance period.

The amount of money you get from disability payments depends on how much your regular income is. It’s also a regular, ongoing payment, unlike CI insurance that gives you the payout all at once.

DI payments are meant to be used to cover your mortgage payments or rent and pay for your normal daily expenses while you’re not working and recovering. But you can use it any way you like. Payments continue until you get better enough to go back to work, or until your coverage ends.

Key features of disability insurance include:

- Benefit amount: Depends on your monthly income (avg. $2,000+)

- Payment: Monthly until you recover and return to work, or until your coverage period ends — whichever comes first

- Beneficiary: The insured person (you)

- Requirements: elimination period of waiting period of 30 days to 1 year or more — your disability must last longer than this period before your insurance payments can begin

What can disability insurance cover?

A disability policy will cover any injury or illness that prevents you from working. This includes mental health concerns.

Most people only think of physical, visual injuries as disabilities — like if you fall at work and break a bone or if you suffer a severe burn. Those count as covered conditions for sure. But the 3 most common disability insurance claims in Canada are for:

- Mental illness

- Musculoskeletal issues

- Injury or poisoning

Is critical illness insurance covered in health insurance?

No, critical illness insurance is not included in these plans and must be purchased separately. Standard health insurance in Canada covers medical treatments, prescriptions, and routine care. Critical illness covers costs not typically addressed by health insurance, such as loss of income, home modifications, or experimental treatments.

Is critical illness insurance worth it in Canada?

Yes, critical illness insurance is worth it in Canada because provincial healthcare only covers basic medical needs, such as hospital stays and essential treatments. It doesn’t cover lost income, specialized treatments, or private care, leaving gaps that can cause financial strain during a serious illness.

Critical illness insurance helps fill these gaps through a lump-sum payout. Given the high prevalence of serious illnesses like cancer, heart attacks, and strokes, critical illness insurance ensures that if you’re diagnosed with a life-threatening illness, you won’t have to bear the financial burden alone.

Are critical illness and disability insurance offered as a part of group benefit?

Yes, critical illness insurance and disability insurance are offered as an optional or add-on benefit by some Canadian employers. However, when compared with personal critical illness and disability insurance plans, group policies have lower coverages. There is a lack of flexibility with group plans while personal critical illness and disability plans are customized for every individual.

Where can I compare critical illness versus disability insurance quotes in Canada?

You can shop and compare instant quotes from leading insurance companies on PolicyAdvisor.com. Get personalized quotes for critical illness or disability insurance in minutes on our website. Just click the button below to get started.

As Canada’s best insurance broker, we’re also happy to do the legwork for you if you want! Click here to book a free consultation call with our licensed advisors and let them weigh the pros and cons for you personally. Our team can give you advice tailor-made for your circumstances, so you can make the best decision.

Frequently asked questions

Is it better to get disability or critical illness insurance?

It really depends on your needs. Both types of insurance policy serve different needs in different ways, so there is no answer as to which one is “better” to get.

People working high-risk jobs may find it more useful to get disability coverage. Or, if they find they have a good disability plan through their work or union benefits, they may find it better to buy their own critical illness plan to cover them

Meanwhile, self-employed people may choose to get both. They may not have the benefit of a group plan through their work, so may want to get both for maximum coverage.

Does a critical illness policy cover disability and vice versa?

Sometimes there can be overlap between critical illness coverage and disability insurance. Some critical illnesses are disabilities (such as blindness and paralysis). What counts as a disability for insurance purposes can vary a lot, so it’s more difficult to say.

In our experience, there can be overlap between the two. But it’s very case-by-case and depends a lot on the individual diagnosis.

Can I claim for both critical illness insurance and disability insurance in Canada?

Yes. If you have both types of coverage and something serious happens to your health to stop you from working, you can submit a claim for both policies.

Your CI provider will give you a one-time lump sum payment. And your disability coverage will start giving you monthly payments until you recover. You will get both payments.

Which is cheaper — disability coverage or critical illness coverage?

It depends. How much your premiums will cost for either types of these insurance policies depends on things like:

- Age

- Health

- Occupation

- Policy details

- Coverage extent

- Add-on riders

- And more

Remember — these policies serve different needs. Yes, they work together very well to help protect your wallet if something unexpected happens. But they can be like comparing apples and oranges.

If you’re on a tight budget and worried about whether you can afford both, give us a call at 1-888-601-9980. Everyone’s situation is different, so our agents can help you figure out your best move.

Do Canadians ever need both CI and DI insurance?

Yes. Many Canadians can benefit from having both critical illness and disability insurance coverage.

Critical illnesses in particular are very common in Canada. Disability insurance is also more common than most people realize.

Having insurance gives you peace of mind, especially if your family relies on the money you earn. If something unexpected happens and you can’t work, insurance lets you still be able to pay bills and keep up with your everyday expenses.

A lot of Canadians expect to rely on the government to take care of their expenses if they become seriously ill. But we do not recommend this because the amount you receive is often not enough to cover your normal day-to-day needs.

People can confuse critical illness insurance with disability insurance. But they’re different products that do different things. Critical illness insurance gives you a one-time sum of money if you’re diagnosed with a severe illness. On the other hand, disability insurance gives you regular payments to replace a part of your income if you become injured or ill to the point where you can’t work.