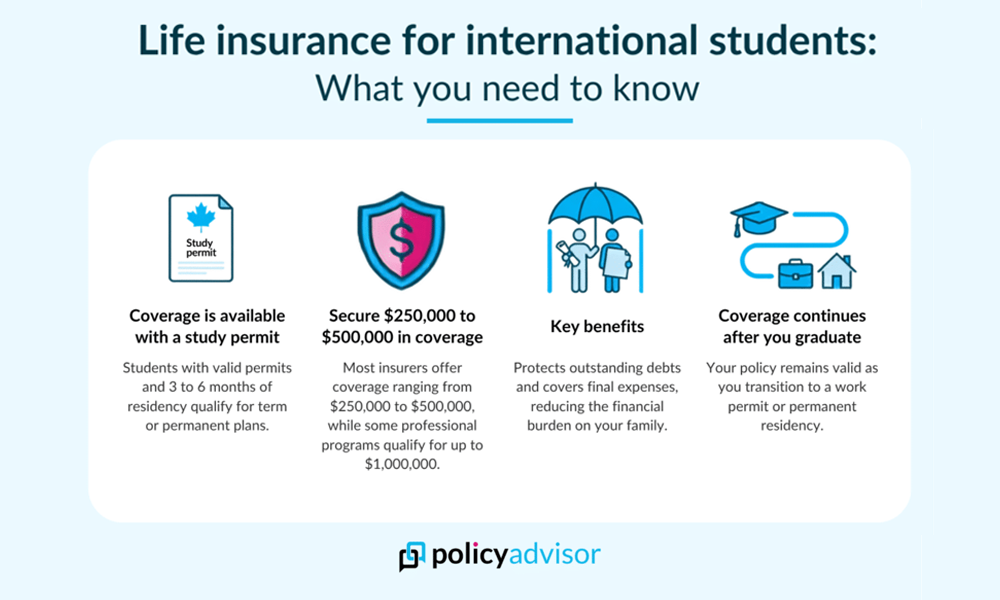

- International students can qualify for both term and permanent life insurance in Canada with a valid study permit and an eligible residency status

- Some of the top insurers offering life insurance for international students include Assumption Life, Beneva, Canada Life, Desjardins, Manulife, RBC Insurance, and others

- Most insurers offer coverage between $250K and $500K, while Equitable Life may offer up to $1M for students in eligible professional programs

- Coverage can usually continue after graduation, when transitioning to a PGWP, or after obtaining permanent residency, provided premiums are paid

International students in Canada can buy life insurance to protect their loved ones from financial hardship if something happens to them. Many top Canadian insurers, including Manulife, Sun Life, Empire Life, and others, offer life insurance to students with valid study permits. The exact coverage limits, eligibility requirements, and premiums, however, vary. Students can use life insurance to cover debts, protect co-signers, and secure affordable coverage while they are young and healthy.

Can international students get life insurance in Canada?

Yes, international students can get life insurance in Canada. Most Canadian life insurance companies offer coverage to temporary residents, including international students, provided they have a valid study permit, reside in Canada, and meet the insurer’s underwriting requirements.

International students can choose from term life insurance and permanent life insurance:

- Term life insurance: Term life insurance provides coverage for a specific period, such as 10, 20, or 30 years. It is generally the more affordable option. It is well-suited for students who want financial protection during their studies or while paying off debts and supporting family members

- Permanent insurance: Permanent life insurance includes options like whole life and universal life, both of which provide lifelong coverage as long as premiums are paid. Whole life insurance has become an increasingly popular choice, offering predictable premiums and steady cash value growth over time, making it a long-term financial planning tool for students who intend to remain in Canada after graduation or to pursue permanent residency

Why do international students need life insurance in Canada?

Health insurance is generally mandatory for international students, but life insurance isn’t, even though it covers something your health plan doesn’t: protecting the people who depend on you. Some of the common reasons to buy life insurance are as follows:

- Covering outstanding debts: Life insurance can help pay off student loans, private loans, credit card balances, or other debts that may otherwise burden family members

- Protecting a co-signer or guarantor: If a parent has co-signed a student loan, life insurance can help ensure the debt is repaid

- Planning for long-term settlement in Canada: Students who intend to stay in Canada after graduation may purchase life insurance early to lock in lower premiums while they are young and healthy

- Covering final expenses: A policy can help pay for funeral, burial, or repatriation costs, which can be expensive for families living abroad, if anything unforeseen happens to the student

What are the eligibility requirements for international students to get life insurance in Canada?

The exact eligibility requirements to apply for life insurance in Canada vary by insurer and the type of policy you choose. However, most insurers require the following:

- Hold a valid study permit, along with a copy of it as supporting documentation. Beneva Insurance may also require a copy of your study permit

- Be enrolled full-time at a recognized Canadian college, university, or educational institution

- Have a permit that remains valid for at least 3 months beyond the application date

- Have lived in Canada for a minimum period of 3 to 6 months, depending on the insurer

- Insurers like Desjardins require an intention to remain in Canada, such as plans to apply for permanent residency (PR)

- Meet the insurer’s age, residency, and underwriting requirements

- Complete any required health questionnaire or medical underwriting

How much life insurance can an international student get in Canada?

International students can qualify for $250K to $500K in life insurance coverage in Canada. There are some insurers like Equitable Life that even offer up to $1M for students enrolled in certain professional programs like MBA, medicine, optometry, pharmacy, podiatry, teacher’s college, veterinary medicine; however, there are specific terms and conditions for the same. The maximum amount available depends on factors such as your residency status, length of stay in Canada, program of study, employment status, and the insurer’s underwriting guidelines.

Why are life insurance coverage limits lower for international students?

Life insurance coverage limits are often lower for international students because insurers consider temporary residents to be a higher underwriting risk. Some of the reasons why international students get lower coverage limits are as follows:

- Temporary residency status: Students may leave Canada after completing their studies. This increases risk for insurers, as they may have limited visibility into an applicant’s long-term plans, future residency status, and ongoing ties to Canada

- Limited Canadian financial history: Many international students have not lived in Canada long enough to build a credit history, stable income record, or other financial track record, making it harder for insurers to evaluate their risk and offer higher coverage

- Lower insurable income: Coverage amounts are often linked to income and financial obligations, which may be lower for full-time students who do not have a reliable source of income

- Country of origin considerations: International students may travel frequently between Canada and their home country during school breaks or vacations. Depending on the countries they visit and the amount of travel involved, insurers may view this as an additional risk when assessing coverage eligibility and limits

Which life insurance companies offer coverage to international students?

Several Canadian life insurance companies offer coverage to international students, although eligibility requirements and coverage limits vary. Below is a list of insurers, the maximum coverage they offer, and key eligibility requirements:

| Insurer name | Maximum coverage amount | Key eligibility requirements |

| Assumption Life | Up to $250,000 (under 18) / Up to $500,000 (18+) |

|

| Beneva | $250,000 |

|

| Canada Life | $250,000 |

|

| Desjardins | $250,000 |

|

| Empire Life | $250,000 |

|

| Equitable Life |

|

|

| iA Financial Group | $500,000 |

|

| Manulife | $250,000 |

|

| RBC Insurance | $500,000 |

|

| Sun Life | $250,000 |

|

Can international students get critical illness coverage in Canada?

Yes, international students can get critical illness insurance in Canada, although their options are more limited than those available to permanent residents and work permit holders. The coverage for critical illness is available through select insurers, with Assumption Life offering the broadest access, while Canada Life, Desjardins, and iA Financial provide coverage of up to $100,000.

Most insurers require proof of full-time enrollment at a Canadian college, university, or other eligible educational institution, along with a valid study permit and evidence that the student intends to remain in Canada. However, many major insurers, including Beneva, Empire Life, Equitable Life, Manulife, and Sun Life, do not currently offer critical illness insurance to international students.

How much does life insurance cost for international students?

The cost of life insurance for international students depends on factors such as age, health, smoking status, coverage amount, and the insurer’s underwriting requirements.

The table below shows sample monthly premiums for a 20-year-old non-smoking international student seeking $100,000 of 20-year term life insurance coverage (T20).

| Insurer name | Monthly premiums (Male) | Monthly premiums (Female) |

| Assumption Life | $12.24 | $10.44 |

| Beneva | $10.80 | $9.36 |

| Canada Life | $11.36 | $10.00 |

| Desjardins | $11.07 | $9.72 |

| Empire Life | $10.80 | $9.36 |

| Equitable Life | $10.61 | $9.35 |

| iA Financial Group | $11.34 | $9.81 |

| Manulife | $10.85 | $9.44 |

| RBC Insurance | $13.05 | $10.53 |

| Sun Life | $11.61 | $10.08 |

Disclaimer: These are representative value and the actual premiums may vary

How much does Life Insurance cost?

Get instant quotes from Canada's top life insurance providers and find the perfect coverage for your family.

Powered by

![]()

Factors to consider while buying life insurance for international students in Canada

Since insurers have different underwriting rules for temporary residents, choosing the right policy requires more than simply comparing premiums. Listed below are some of these factors:

- Study permit requirements: Most insurers require you to hold a valid study permit and be legally residing in Canada. Some companies also require your study permit to remain valid for a minimum period after you apply. For example, Equitable Life insurance requires a student visa that is valid for at least three months beyond the application date

- Coverage needs: Your coverage amount should reflect your financial responsibilities. If you have dependents, a co-signed loan, student debt, or family members who rely on your financial support, choose a coverage amount that can help cover those obligations. Choose Equitable Life, iA Financial Group, and RBC Insurance for higher coverage limits

- Intent to stay in Canada: Many insurers prefer applicants who intend to remain in Canada after graduation. If you plan to apply for permanent residency, you may qualify for more insurers, higher coverage limits, and a wider range of policy options

- Life insurance type: Term life insurance is usually more affordable and suitable for temporary financial needs, while permanent life insurance provides lifelong coverage and may build cash value over time. Choose the one that best fits your needs and budget

- Coverage after graduation: If you plan to work or settle in Canada after completing your studies, consider whether the policy can remain in force after your residency status changes. Many policies continue as long as premiums are paid, regardless of whether you later obtain a work permit or permanent residency

Can you keep your life insurance policy after you graduate, move to a PGWP, or get PR?

Yes, you can keep your life insurance policy after graduation, when transitioning to a Post-Graduation Work Permit (PGWP), or after becoming a permanent resident. As long as you continue paying your premiums, your coverage typically remains in force. However, if you permanently leave Canada, some insurers may have restrictions or additional requirements. It is important to notify your insurer whenever your residency or immigration status changes, so that your beneficiaries face no issue with future claims.

How to choose the best life insurance policy as an international student with PolicyAdvisor?

Planning to buy a life insurance policy as an international student? Don’t worry! At PolicyAdvisor, our experienced advisors can help you identify the insurers you are eligible for and compare the best available options. Here are the steps you need to follow:

- Assess your coverage needs: Speak with our licensed advisors to determine how much coverage you need based on your financial obligations, dependents, and plans in Canada

- Compare quotes from multiple insurers: Our advisors will help you compare life insurance options from Canada’s leading insurers that cover international students.

- Review your eligibility: We will help you understand residency requirements, coverage limits, and any underwriting conditions that may apply to your situation

- Complete your application: Submit your documents, such as your passport, study permit, and proof of enrolment, and complete any required health questionnaires

- Review and complete the policy payment: Once approved, review your policy details, beneficiaries, exclusions, and coverage amounts before activating your coverage. Our advisors will help you complete the payment and finish the application process

If you still have any questions about life insurance, schedule a call now with our advisors and get the required assistance. Schedule a call now!

Frequently Asked Questions

Can international students buy term life insurance in Canada?

Yes, international students can buy term life insurance in Canada. Most insurers offer term life insurance to eligible international students with a valid study permit. Term life insurance provides coverage for a fixed period, such as 10, 20, or 30 years, and is usually the most affordable option.

Can international students name beneficiaries outside Canada?

Yes, international students can name beneficiaries outside Canada. However, it is important to provide accurate beneficiary information when applying for coverage. Life insurance companies do not restrict beneficiaries by the country of their residence.

What happens to my life insurance if I leave Canada permanently?

Many life insurance policies remain in force after you leave Canada, provided premiums continue to be paid. However, some insurers may impose residency-related conditions, so it is important to review your policy terms and notify your insurer before relocating.

How much life insurance coverage do international students need?

The right coverage amount depends on your financial obligations, including student loans, co-signed debts, dependents, and final expenses. Many international students choose coverage between $100,000 and $500,000, depending on their needs.

What are the eligibility requirements for international students to get life insurance in Canada?

International students can qualify for life insurance in Canada if they meet an insurer’s residency, study permit, and underwriting requirements. While eligibility criteria vary by provider, most insurers require applicants to be legally studying and residing in Canada. Few insurers have rigid residency requirements; for example, Empire Life requires that the international student must have spent a minimum of 3 months in Canada.

Life insurance is available to eligible international students in Canada through insurers including Canada Life, Manulife, Equitable Life, RBC Insurance, iA, and others. Students can choose between term and permanent life insurance, with coverage amounts based on their residency status, program of study, and financial needs.