- Life insurance premiums for people in their 20s are among the lowest possible.

- Buying a home or starting a family are two good reasons for a person in their 20s to invest in life insurance.

- Your life insurance coverage should at least be enough to pay off your debt, but also extend to income replacement.

For many young people in their 20s, fitting life insurance costs into their monthly budget is hardly a priority. And that’s understandable. In your 20s, you’re still figuring out what your life will look like—and how to pay rent in an ever-inflating economy. Plus, you probably don’t have dependents or many significant financial responsibilities yet.

But that doesn’t mean that you shouldn’t consider signing up for a life insurance policy. In fact, your 20s may be the best time to buy. Let’s take a closer look.

What is the average life insurance cost for a 20 year old?

The average cost for life insurance for a 20 year old is about $10-20 per month for $500,000 in coverage. In your twenties (especially your early twenties), age won’t be a factor in driving up premium costs. In fact, the cost difference between 20 and 29 is usually less than a dollar.

The exact cost will depend on factors like your specific health, gender, and lifestyle. Other factors, like your smoking status, having pre-existing health conditions, or participating in any extreme sports, can have an influence on your monthly cost of life insurance.

Take a look at the chart below to understand what the average premiums are for a term life insurance policy in your twenties.

Life Insurance Premiums – Male, 20-Year Term Life Insurance

| Age | $100K | $250K | $500k |

|---|---|---|---|

| 20 | $10.26 | $18.00 | $30.15 |

| 21 | $10.26 | $18.00 | $30.15 |

| 22 | $10.26 | $18.00 | $30.15 |

| 23 | $10.26 | $18.23 | $30.60 |

| 24 | $10.26 | $18.23 | $30.60 |

| 25 | $10.26 | $18.23 | $30.60 |

| 26 | $10.35 | $18.23 | $30.60 |

| 27 | $10.44 | $18.23 | $30.60 |

| 28 | $10.44 | $18.23 | $30.60 |

| 29 | $10.53 | $18.23 | $30.60 |

*Representative values, based on regular health

The cost for a 20-year term life insurance policy is the cheapest for women in their 20s. See the rates for life insurance for women in the chart below.

Life Insurance Premiums – Female, 20-Year Term Life Insurance

| Age | $100K | $250K | $500k |

|---|---|---|---|

| 20 | $8.55 | $13.73 | $20.70 |

| 21 | $8.55 | $13.73 | $21.15 |

| 22 | $8.64 | $13.73 | $21.15 |

| 23 | $8.64 | $13.95 | $21.60 |

| 24 | $8.73 | $13.95 | $21.60 |

| 25 | $8.73 | $13.95 | $22.05 |

| 26 | $8.82 | $14.18 | $22.05 |

| 27 | $8.91 | $14.40 | $22.50 |

| 28 | $8.91 | $14.63 | $22.50 |

| 29 | $9.00 | $14.85 | $22.95 |

*Representative values, based on regular health

Life insurance premiums are typically paid every month – like phone bills or mortgage payments – so you should ensure the payment fits into your monthly budget without too much trouble. That said, many insurance companies offer a policy discount if you opt to pay for your coverage annually.

To find out exactly how much life insurance will cost you in your 20s, check out our quoting tool below!

Is life insurance worth it in your 20s?

The short answer is yes! Life insurance is worth it in your 20s. You should get life insurance in your 20s, strictly because it’s the most inexpensive it will ever be for you. A 20-something who has children or a spouse, or who has a sizeable debt, like a mortgage, can benefit greatly from life insurance, which can support their loved ones financially in case of their death.

Here are some reasons you may need life insurance in your 20s:

- You have children of any age

- You have a mortgage or plan on buying soon

- You have other forms of debt such as credit card debt or a line of credit

- You are the main earner for your family, with dependents like your children, partner, or parents relying on your annual income

- You are continuing to accumulate assets that will someday be transferred to your beneficiaries

- You want to make sure your family can cover your final expenses, like funeral costs

That being said, not every person will be ready to purchase life insurance in their twenties. Students (as well as those entering the job market for the first time) may not have the budget for an added monthly or yearly expense of an insurance premium. Additionally, the death benefit from a life insurance policy may not yet be vital at this point in their financial life, especially if they are without dependents or major debt. The bottom line is: if you can’t afford the monthly premium, it’s not worth it.

How much life insurance does a 20-year-old need?

The amount of life insurance a person in their twenties needs varies greatly, depending on their financial situation, family, homeownership, and other factors. Common amounts of life insurance coverage are $100,000, $250,000, $500,000, and $1 million. As a general rule, your life insurance coverage should at least be about 10 times your income. Or it should be at least enough to pay off your debt (including any credit cards, car loans, mortgages, etc.) so that your family is not held liable to settle the debt should anything happen to you.

When you’re thinking about how much coverage you need, consider:

- Funeral expenses

- Your outstanding debts (student loan, car loan, mortgage, credit card)

- The cost of education for your children or dependents

- Your annual salary, and how long you want your beneficiaries to live off of it

You can calculate these costs manually, or head over to our life insurance calculator. You can enter simple information about your financial goals and we can tell you exactly how much coverage you will need to secure your family’s future.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

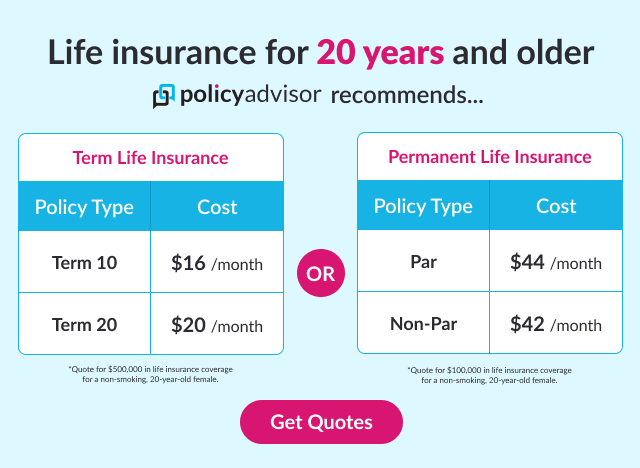

What life insurance is best in your 20s?

There are many options for life insurance when you’re in your 20s! When you’re young and (presumably) have a good medical history, most insurance options will be the cheapest you’ll ever get. Term life insurance may be best for most people in their 20s, but permanent coverage may be beneficial for you as well!

How do I buy life insurance in my twenties?

If you’re looking to secure a term or permanent life insurance policy in your twenties, look no further. The insurance experts at PolicyAdvisor are available to help you find the right policy for your needs and budget. We bring you instant, customized life insurance quotes from Canada’s top insurance providers, as well as any additional support you need.

Life insurance costs about $10-20 per month for a 20-year-old in Canada who is looking for $500,000 in coverage. Buying a life insurance policy in your 20s can give you access to some of the lowest life insurance rates on the market. Because of this, it can be beneficial to lock in a term life insurance policy with a fixed rate. Still, it is important that 20-year-olds evaluate whether it’s the right time for them to invest in life insurance.