1-888-601-9980

1-888-601-9980

- Make sure your beneficiaries know they are named on the policy and have correct information and documentation (like the policy contract) so they can file their claim quickly

- There is a two-year contestability period where the insurance provider can void coverage if it discovers an error in a material fact in the application

- In case of fraudulent misrepresentation, the policy can be made void at any time by the insurance company

- Most claims are settled within 30 or 60 days, but some policies can take much longer

Many purchase life insurance for the protection it provides, but don’t put much thought into the process their beneficiaries will go through to get the life insurance payout. During this difficult time, beneficiaries may be unsure how to collect the financial security you have set up for them. Thankfully, claiming a life insurance benefit is a fairly quick and straightforward process in Canada.

Read on to find out exactly what you need to do to make a life insurance claim.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

How to file a life insurance claim

If you are the beneficiary on a life insurance policy, you will need to contact the insurance agent or the insurance company where the policy is from. They can then walk you through the process involved in receiving the insurance benefit. This is commonly called filing a claim.

The steps to file a claim are fairly similar among most Canadian life insurance companies.

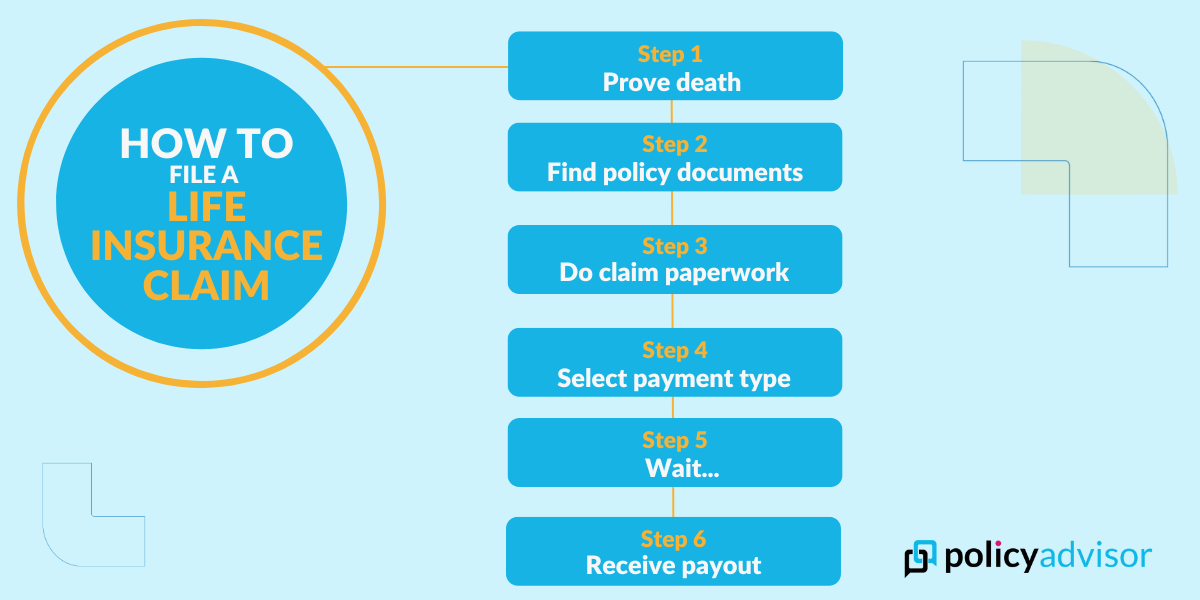

Step 1: Submit proof of death of the insured

Step 2: Submit the policy contract

Step 3: Fill out the death claim paperwork

Step 4: Tell them how you want to be paid

Step 5: Wait for the claim to be processed

Step 6: Get the payout

Step 1: Submit the proof of death

The claims process starts with submitting the proof of death of the person insured. All claims require the submission of at least one document. This is usually the death certificate. However, based on the dollar value of the death benefit payment, two separate documents may be required.

Documents that prove the death of the insured may include:

- the death certificate

- funeral director’s statement

- coroner’s report

- obituary

- funeral service program

- funeral home bill

- police reports

- medical records

Depending on the circumstances, the insurance company may request an attending physician’s statement (APS) to certify the cause of death and to verify the medical information that was used to underwrite the policy.

The claims packet sent to the beneficiary will usually specify exactly what documents are required to prove the death of the insured person.

Here are some other things to keep in mind when proving death for life insurance:

- Most insurance companies do not accept a death certificate where the cause of death is yet to be ascertained or is mentioned as “pending”.

- For foreign deaths, many companies require valid death certificates from the country where the death occurred.

- The certificate should be translated into English (or the main business language of the carrier).

Step 2: Submit the policy contract, if available

Along with the claim forms, the submission of the original policy document can help speed up the process. This is the original document that contains all the information relating to the policy for the insurer to cross-check when they first enact the policy. In case you have lost or misplaced the original policy, you should contact the company for a digital retrieval of the document.

Step 3: Filling out the death claim paperwork

This is where you need to provide all relevant information pertaining to your claim. This includes

- the policy number

- the cause of death

- the relationship of the beneficiary or claimant to the life insured

- funeral home information

- any other pertinent information about the death of the insured

Step 4: Specify how you want the amount to be paid

Once you submit the required documentation, the insurance company will cross-check the information and fact-check the claim. As the beneficiary, you can opt for:

- One lump-sum payment: receive the entire death benefit at once.

- An annuity*: the death benefit amount is invested and paid out in the form of a yearly payment. You can receive these payments for life or for a predetermined number of years, depending on the policy.

*not all policies allow for annuity payments.

Step 5: Wait for the claim to be processed

It takes time for the insurance company to process the claim before one receives the death benefit payment. However, insurance companies want to pay out the death benefit as quickly. Paying in a short time frame helps them avoid interest charges that accumulate on unpaid death benefits. Depending on your policy, and if the claim is not subject to any investigation, the processing of the claim may take anywhere between a few days to as long as 30 to 60 business days.

Step 6: Get the life insurance payout

Once the processing is done, you, the beneficiary, will receive the benefit in the payment method requested (lump sum or annuity).

Life Insurance Claims Frequently Asked Questions

Can a life insurance claim be denied?

Yes. There are multiple circumstances under which life insurance companies may choose to deny a life insurance claim. These reasons could be a discovery of false or fraudulent information during or after the contestability period, exclusions on the policy, a lapse of the policy, or more.

Two-year contestability period

The contestability period of an insurance policy lasts two years from the date the policyholder was approved for coverage. This means an insurance company has two years after it issues the policy to void the coverage or adjust the premiums if it discovers an error in a material fact in the application.

A material fact is any piece of information that influences an insurance company’s decision about providing insurance coverage (such as smoking status, known health issues, age, etc) during the underwriting process. Once the two-year contestability period passes, the policy is incontestable. An insurance company can only void or cancel the policy if it can prove the policyholder committed fraud when applying for the policy or in the case of missed premiums.

For example, if, at the time of claim, an insurance company determines the deceased person had misstated their age on the application, it can void the policy and deny the claim only if it can prove that the misstatement of age was fraudulent. If it was an honest mistake (the misstatement was not fraudulent) then the insurance company will pay the death benefit. However, it will adjust the amount of the death benefit to correlate with how much coverage the applicant would have been able to purchase with the premium they paid had the correct age been known.

If the policyholder passes away during the contestability period and any instances of fraud or misrepresentation come to light, the insurer may choose to cancel the policy, refuse to pay the benefit, or subtract money from the death benefit.

False or Fraudulent Information

False or fraudulent information can also result in a denial of a claim. Hiding smoking or drinking habits, or misrepresenting details like age, height, and weight could create problems when a claim is made.

Exclusions

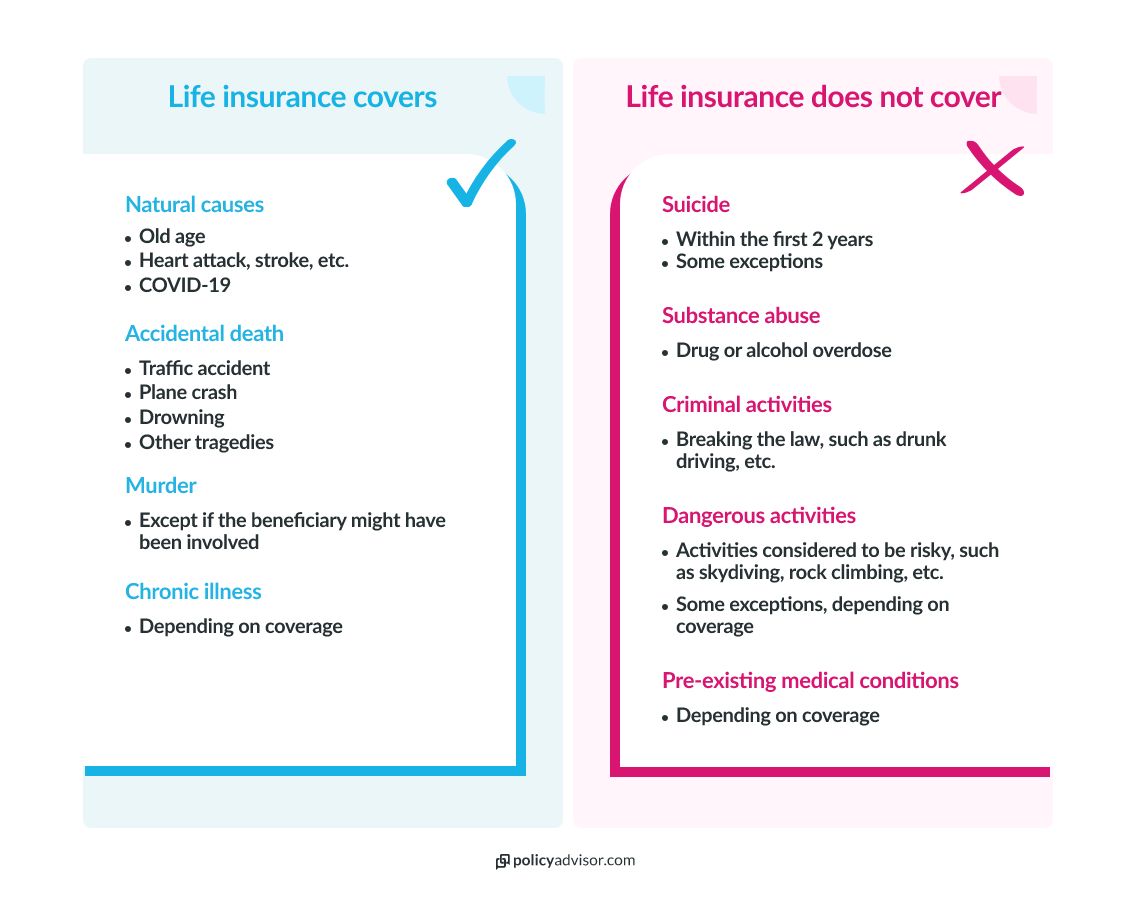

The provider may deny the claim if the type of death was not included in the policy. Death due to suicide in the first 2 years of coverage, homicide*, or death due to engagement in illegal activities, drug abuse, dangerous activities, or the acts of war are some common exclusions.

Note: typically if you are murdered it will still pay out, but if murdered by the beneficiary it will still pay out but to the estate.

Read more about life insurance coverage and death by suicide.

Lapse of Policy

Missing a life insurance premium payment may lead to the cancellation of the policy. If you miss paying your premium on the specified date, take care to inform your insurance provider as quickly as possible. Usually, insurance companies grant a grace period of 30 days and one should settle all your pending payments within that time to ensure there is no lapse in their coverage. Otherwise, all the premiums you paid up to that point may go to waste, and it could prove costly to get coverage again at this later date.

What happens if a life insurance claim is denied?

If an insurance provider has denied your claim, it will generally provide a written explanation detailing the reason(s) the claim has been denied. Once the reason is known and the life insurance beneficiaries can effectively prove that the carrier’s decision to deny the claim is not justified or warranted, the issue could be cleared up.

This can be accomplished by writing an appeal letter for the denial or speaking with a designated representative of the company. If the carrier still denies the claim, at this point the claimant could consider legal recourse.

Can a life insurance claim be delayed?

Yes. A claim may get delayed if they are investigating false or fraudulent information, which could lead to the denial of a claim. Providing incorrect information, death during the contestability period, a delay in filing, and not making proper disclosures about other policies are all valid reasons for a delay of a claim. Additionally, there are some other reasons which can play a role in delaying claims:

- A minor beneficiary, without any trustee designated to their name, may witness delays in getting the proceeds of an insurance policy.

- If the policyholder mentions no beneficiary, the claim goes to the insured’s estate through probate.

- If the policyholder named their ex-spouse in the policy as the beneficiary and they did not update the policy the claim may get delayed

Read more about life insurance and divorce settlements

How long does it take to process a life insurance claim?

Processing a claim may take anywhere between a few days to as long as 60 days or more. For example, if the insurance company suspects that the death happened due to suicide and the policy falls within the two-year suicide exclusion period, it may want to investigate the death more thoroughly and this could take time. However, if there are no issues or cause to suspect the claim, they usually get processed within 30 to 60 days.

Is there a timeline for filing a claim?

Sometimes. Some policies may state that you must file before 90 days to 12 months, others may not. In any case, it is always good to file a life insurance claim as early as possible. If the policy is active at the time of the life insured’s death, all premiums are paid on time, and there are no grounds for the provider to deny the claim, the beneficiary will get the death benefit they are owed in a timely fashion.

How can I use the proceeds from life insurance?

There are no rules about how the life insurance payout can be used. While many policyholders get coverage to soften the financial hardship their death may have on those they leave behind, those receiving the benefit from a life insurance payout can use the proceeds in any way they see fit. Many choose to use it to pay off mortgages, fund education, or for down payments on other properties.

Is interest paid on the proceeds of a life insurance death benefit?

An insurance provider is required to pay interest for the period it takes to process a life insurance claim. However, this may be subject to certain conditions. This period is generally the interval between the date of death of the policyholder and the date of payment.

Are life insurance proceeds taxable?

Usually, the proceeds of a life insurance death benefit are not taxable. However, any excess interest earned on the death benefit while the insurance company held the funds would be taxable. This can happen if there are any delays in a claim being settled (especially after the receipt of all required documents), or if an insurance provider was directed by the policyholder to hold the proceeds for a period before transferring it to the beneficiary.

If the policyholder has made an estate the beneficiary of their policy, the estate’s heirs might need to pay estate taxes

Read more about life insurance and taxes.

In order to access the death benefit of a life insurance policy, the beneficiary must file a life insurance claim. Fortunately, in Canada releasing the death benefit is fairly straightforward, with most benefits being issued to beneficiaries within 30-60 days. The first step is contacting the insurance company to start the claims process. The next set of steps will be proving the death of the insured, specifying how you want to be paid, and waiting for the payout.