- Annuities provide guaranteed income by converting a lump sum into regular payments, ensuring financial stability for a set period or for life

- There are different types of annuities, including immediate, deferred, fixed, and variable, each offering unique payment structures and risk levels to suit various financial needs

- The tax treatment of annuities depends on their type, with registered annuities being fully taxable, while non-registered annuities offer tax-efficient income options

- Annuities are best suited for risk-averse retirees seeking financial security, but they may not be ideal for those who require liquidity or higher investment growth

An annuity is a financial product that provides a steady stream of income, typically used for retirement planning. In Canada, annuities are offered by insurance companies and are designed to convert a lump sum of money into regular payments for a specified period or for life.

In this guide, we’ll take you through how annuities work, their types, benefits, tax implications, and more.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What exactly is an annuity and how does it work?

An annuity is a contract between an individual and a life insurance company that provides regular payments either immediately or in the future. You can purchase an annuity with a lump sum or make payments over time.

Annuity payments come from interest, your original investment, and shared funds from those who pass away earlier than expected. Unlike life insurance, which pays a benefit after death, an annuity provides steady income while you are alive.

An annuity works by exchanging a lump sum or a series of payments for a guaranteed income stream. It has two key phases: accumulation and annuitization.

- Accumulation: You contribute funds through premiums or a lump-sum payment

- Annuitization: The insurance company begins making regular payments to you, which can be monthly, quarterly, semi-annually, or annually

Annuities can be classified into immediate and deferred annuities based on when payments begin:

- Immediate annuity: Payments start right after the purchase

- Deferred annuity: Payments begin at a future date, allowing the invested amount to grow over time

Additionally, annuities can be fixed or variable, affecting the predictability of returns:

- Fixed annuity: The insurance company guarantees a set rate of return, ensuring predictable monthly payments. These can last for 5, 7, or even 30 years, or provide lifetime income

- Variable annuity: Returns fluctuate based on investment performance, offering potential for higher gains but also carrying investment risk

Lastly, you will also come across different payout options for annuities:

- Single-life payout: Payments continue only for the annuitant’s lifetime

- Joint-life payout: Payments continue to a second person, usually a spouse, even after the annuitant passes away

What are the different types of annuities in Canada?

Annuities come in several types to meet different financial needs, such as life annuities, life annuities without a guaranteed period, term-certain annuities, and life annuities with return of purchase price.

- Life annuity: Provides guaranteed income for the rest of your life

- Life annuity without a guaranteed period: Payments stop at the annuitant’s death

- Term certain annuity: Pays a fixed income for a set period. If the annuitant passes away before the term ends, the remaining payments go to the beneficiary

- Life annuity with return of purchase price: Regular payments continue for life, and after death, the insurer returns the initial investment to the nominee

What are the benefits of life annuities?

Life annuities offer a guaranteed income for life, ensuring financial security and protecting against the risk of outliving your savings. Annuities provide fixed payments to protect retirees from economic downturns and market volatility. This stability makes an annuity a reliable option if you’re seeking long-term financial peace of mind.

What is the downside of an annuity?

An annuity offers you guaranteed income, but it does come with a few limitations. It is less flexible than other investments, making it difficult to access funds once you purchase it.

Additionally, a life annuity may not provide an inheritance and fixed annuities may lose value over time due to inflation. You must also bear in mind, that returns on annuities are generally lower compared to market-linked products, and some even have high fees for management and early withdrawals.

Who should buy an annuity?

An annuity is a great option for risk-averse individuals who want a guaranteed income stream without worrying about market fluctuations. It is beneficial for retirees seeking financial stability, as it ensures predictable payments to cover essential expenses.

Additionally, those concerned about outliving their savings can benefit from annuities, as they provide lifelong income and financial peace of mind.

Who should not buy an annuity?

An annuity may not be suitable for individuals who need liquidity. This is because the funds become locked in and cannot be accessed for emergencies or other financial needs. Annuities are also restrictive for people seeking high investment growth due to lower returns than market-based investments.

Lastly, those who prioritize leaving an inheritance should carefully evaluate their options, as some annuities stop payments upon death unless additional features are included.

How much does a $100,000 annuity pay per month?

With a $100,000 annuity, your monthly payments will depend on your age at the time of purchase. If you start at age 60, you can expect around $600 per month; at 65, the payout increases to $660 per month; and at 70, it rises to $713 per month.

However, the exact payout may vary based on factors like interest rates, the type of annuity, and the insurer.

How much does a $50,000 annuity pay per month?

A $50,000 annuity for a 65-year-old woman purchasing an immediate single-life annuity could provide $300 per month or $3,596 per year. The exact payout depends on various factors, including the type of annuity, the insurer, and the annuitant’s age and gender.

How are annuities taxed?

Annuities grow on a tax-deferred basis, meaning you won’t pay taxes on your investment until you start receiving income payments. The timing and amount of tax you owe depend on the type of annuity you choose.

- Immediate annuities: Since payments begin right away, the income you receive is taxable in the year you receive it

- Deferred annuities: Taxes are postponed until you start receiving payments in the future, allowing your investment to grow tax-free in the meantime

Tax treatment: Registered vs. non-registered annuities

The taxation of annuities also depends on whether you purchase them with registered savings (such as an RRSP) or non-registered savings (personal funds).

An RRIF (Registered Retirement Income Fund) is a government-registered retirement account designed to provide a steady income stream in retirement. If you use funds from a Registered Retirement Savings Plan (RRSP) to purchase an annuity or fund an RRIF, the entire amount of each annuity payment is taxable as income when received.

With an RRIF, you must withdraw a minimum amount each year, starting the year after you open the account. The key benefit of an RRIF is that your investments continue to grow tax-free until you start withdrawing funds. However, once you receive payments, they are subject to income tax at your marginal rate.

How is term life insurance different from an annuity?

Term life insurance protects your family in case of your death. In exchange for regular premium payments, the insurance company guarantees a lump-sum payout (death benefit) to your beneficiaries if you pass away within the policy term, typically 10, 20, or 30 years.

While term life insurance and annuities both involve financial planning, they serve opposite purposes:

| Term life insurance | Annuity |

| Pays out upon death | Provides payments while you are alive |

| Death benefit is tax-free | Annuity payments are taxable income |

| Protects beneficiaries financially | Provides income to the policyholder |

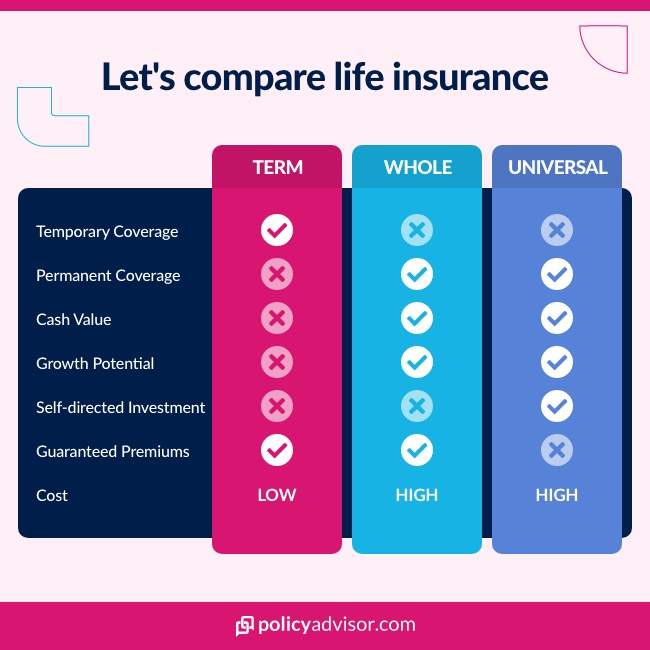

How is whole life insurance different from an annuity?

Whole life insurance differs from term life in that it provides lifelong coverage and builds cash value over time. With participating whole life policies, policyholders may receive dividends, which can be reinvested or taken as cash.

While whole life insurance has features similar to an annuity, such as the ability to generate periodic income, the returns are generally lower.

| Whole life insurance | Annuity |

| Provides lifelong coverage with a death benefit | Designed for income during life |

| Accumulates cash value over time | Converts savings into guaranteed income |

| Policy dividends may provide periodic income | Typically offers higher returns (3-5%) compared to whole life (1-3%) |

While whole life insurance offers some financial flexibility, annuities are generally better suited for retirement income, whereas life insurance primarily serves as a financial safety net for loved ones.

How to buy an annuity?

Buying an annuity is a strategic way to secure guaranteed income for retirement. We recommend that you start by assessing your financial needs to see if an annuity aligns with your retirement goals. You must choose the right type: fixed, variable, immediate, or deferred based on your risk tolerance and income preferences.

Then, we recommend scheduling a call with our expert advisors to compare quotes from 30+ top insurance providers in Canada. Our advisors can also help you understand different ways to fund the annuity and the various payout options you can choose from.

Finally, our insurance advisors will help you complete your application and finalize your annuity contract.

Frequently asked questions

Is an annuity a good investment?

An annuity can be a smart choice if you want guaranteed income during retirement and protection from market fluctuations. It may offer better returns than RRIFs or whole life insurance policies, ensuring financial stability. However, annuities are not suitable for everyone.

Since they limit access to funds and may have lower growth potential, it’s essential to consult a licensed financial advisor to determine if an annuity fits your financial goals. At PolicyAdvisor, we specialize in integrating life insurance into retirement plans, while our trusted partners across 30+ financial institutions provide expert annuity advice.

What is an annuity period?

An annuity period refers to the duration over which you receive annuity payments. It can range from just one year to 30 years or more, depending on the type of annuity you choose. Generally, longer periods provide higher returns, while shorter ones offer smaller payouts. Annuity contracts also come with different payment schedules and features, so it’s important to understand the terms before committing.

Can an annuity be fully cashed out?

Yes, an annuity can be cashed out, but restrictions apply depending on the type of annuity. Surrender charges may apply if you withdraw funds before the term ends, and deferred annuities may incur income tax and early withdrawal penalties. Some policies also include a free-look or cooling-off period, allowing you to cancel without penalties.

What happens at the end of an annuity period?

At the end of an annuity period, you can either withdraw your accumulated funds or roll them into another annuity. If you cash out, any earnings beyond your initial investment may be subject to income tax and withdrawal penalties. However, rolling over your funds into a new annuity allows you to continue earning returns without immediate taxation or fees.

An annuity is a financial product that provides a predictable stream of income, often used for retirement planning in Canada. It works by converting a lump sum investment into regular payments to ensure financial security for a set period or for life. Annuities come in various types, including immediate and deferred, as well as fixed and variable options, each offering different risk levels and payout structures. Annuities provide guaranteed income and protection from market fluctuations but also have limitations like restricted liquidity and potential tax implications. This guide explores how annuities work, their benefits, tax treatment, and key considerations to help you decide if an annuity is the right fit for your financial plan.