1-888-601-9980

1-888-601-9980How does group health insurance work in Canada?

Group health insurance plans are an excellent employee benefit that an organization offers to its members. It typically requires at least 70% enrollment rates so that an insurer’s risk is spread out. Unlike Canada’s provincial health plans, group health benefits offer supplemental coverage like coverage for prescription medications, dental and vision care, critical illness care, etc. It is the most affordable and accessible type of health insurance in Canada.

A group health insurance is a type of health coverage typically offered by an employer or organization to a “group” of people—the employees or members of the organization. Group health insurance is typically cheaper for members of the insured group as compared to separate individual plans since the insurer’s risk is spread across a large number of participating members of an organization. It is an important part of an employee benefits program and employers should know how group health insurance works in Canada.

Whether you’re an employer who is looking to offer group health insurance to your employees in Canada or someone who is simply curious about how an employee benefits plan works in Canada, this blog is for you!

Need group health insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What is group health insurance?

Group health insurance, also known as a group plan or employer-sponsored coverage, is a type of health insurance that an employer purchases and offers to its employees and their dependents. This group of people is accordingly covered under a single policy, offering benefits such as dental and vision care, hospitalization, prescription drugs, and other healthcare services.

Employers or organizations usually negotiate the terms of the insurance policy and may subsidize part or all of the premium costs for their employees or members. Group health insurance is typically offered to all full-time or part-time workers as part of an employee benefits program.

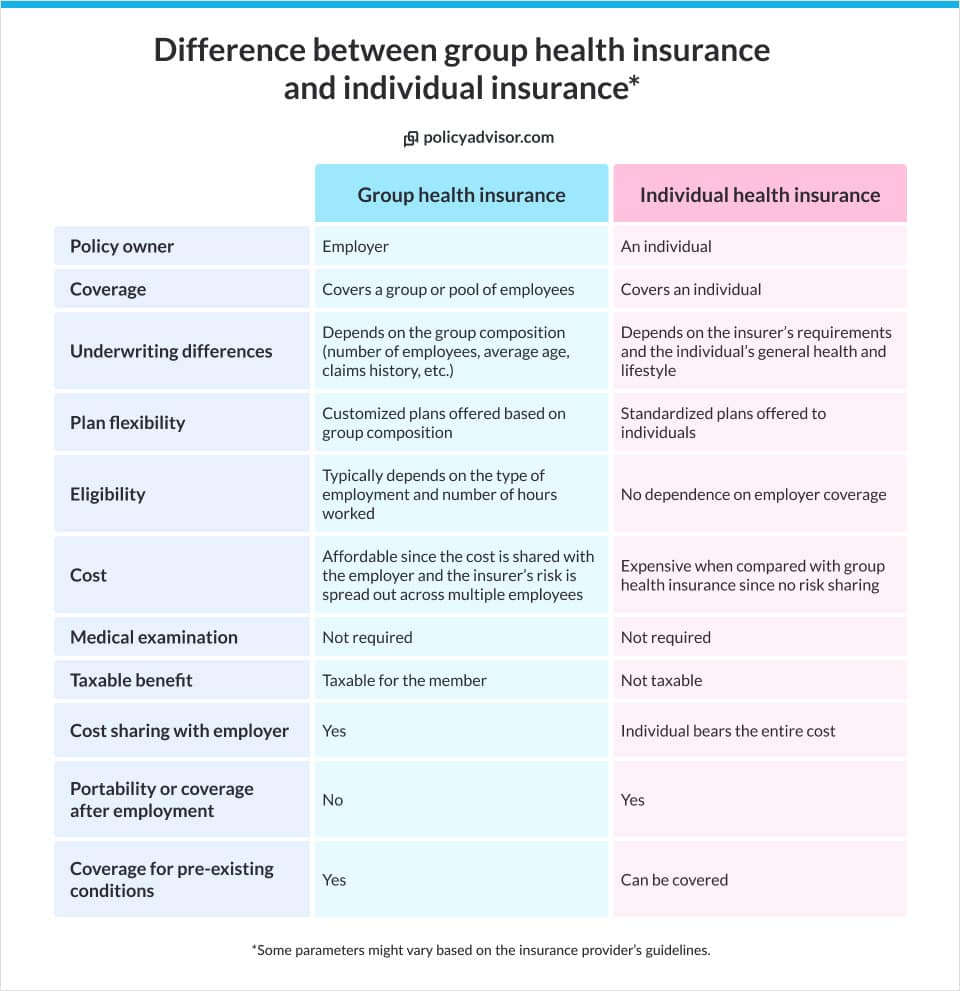

How is group health insurance different from individual plans?

While group health insurance is purchased by an employer and covers the employees of an organization, an individual health insurance plan, as the name suggests, is purchased independently by an individual for their own needs. Individual health insurance plans, also known as personal health insurance or private medical insurance, vary based on the individual’s age, medical history, and lifestyle (whether they’re smokers etc.).

Benefits of group plans for employers

Offering group health benefits is an effective way to promote employee well-being and morale. It also:

✅ Helps organizations attract and retain talent

✅ Can be written off as a business expense, hence saving tax for the organization

✅ Encourages employees to seek preventative care, promoting a more healthier and productive workforce

✅ Depending on the location of the organization, offering health insurance coverage to employees may be required by law. Providing group health insurance ensures compliance with applicable regulations

Group health benefits for employees

With a group health insurance plan in Canada, employees also get:

✅Access to a wider range of medical services like dental care, vision care, prescription medication, emergency travel, life insurance, etc.that are not covered under provincial plans

✅ Lower premiums as compared to other individual plans

✅ The option to add family members and current and future dependents to their policy

✅Coverage for pre-existing medical conditions

✅Incentives for preventive care and wellness programs, motivating employees to adopt healthier lifestyles

How does group health insurance work in Canada?

Group health insurance in Canada provides employees with access to comprehensive healthcare coverage beyond what is provided by the provincial healthcare system. Most group health insurance policies in Canada typically work in the following way:

- Employer sponsorship: Employers choose a plan they want to offer to their employees. The employer negotiates the terms of the insurance policy with an insurance provider and may subsidize part of the premium costs for their employees. Within the plan, the employer can choose to add various types of benefits such as health, dental, vision and prescription drug coverage, plus optional access to life insurance, disability and family assistance plans.

- Employee enrolment: Employees can choose to enroll in or decline a group health insurance plan during the specified annual enrollment period. They have the option to choose from a few plan options and coverage levels. To mitigate risk across a larger group and prevent adverse selection, most insurers require a minimum 70% participation.

- Premium payments: The premiums are typically split between the employer and employees. Employers pay directly to the insurance company and deduct the employee’s contribution through payroll.

- Access to dependents: Employees can add family members and current and future dependents to the group health insurance plan at an additional cost

- Employee usage: Employees can thereafter claim on the benefits as needed. Pharmacies, dentists, as well as health and vision practitioners directly bill the insurance company for covered expenses

- Annual renewal: Employers work with the insurance company for annual renewal and repricing of the insurance contracts

- Administration: The administration of group health insurance plans can vary. Some employers choose to manage the plans themselves, while others may contract with insurance companies or third-party administrators to handle claims processing, customer service, and other administrative tasks.

Group health insurance is cheaper than individual policies. This is simply because of the higher number of participants in the group health insurance plan, making it one of the most affordable health care policies available in Canada. One of the key implications of group health insurance is that healthier individuals effectively subsidize the costs of those who require more medical care.

What do employee benefits cover?

Group health policies and employee benefits, although distinct, are often used interchangeably. A group health insurance plan is part of an employee benefits package, offered by employers to their employees. While group health insurance is a significant component of employee benefits, it is not the only one. Other common employee benefits may include life insurance, disability insurance, paid time off (such as vacation days and sick leave), wellness programs, and more.

Depending on the plan an employer chooses, group employee benefits typically include a variety of health and other non-medical benefits.

| Coverage Category | Covered Services & Items |

| Healthcare | – Private hospital coverage |

| – Medical expenses | |

| – Medical equipment | |

| – Some elective surgeries | |

| – Care homes and nurses | |

| Vision care coverage | – Eye exams |

| – Glasses | |

| – Contacts | |

| Dental coverage | – Teeth cleanings |

| – X-rays | |

| – Cavity fillings | |

| – Orthodontics (braces) | |

| Prescription drugs | Generic and branded medications |

| Health spending account | A fixed annual amount that employees can spend on any item or service that improves their health |

| Employee assistance and wellness | Access to preventative health assessments and wellness resources including clinical counselling |

| Virtual access | Some insurers have online access to doctors and health service providers which an insured employee can avail of |

| Hospitalisation | Access semi-private rooms upon hospitalization and ambulatory care |

| Medical emergency travel | – Coverage if you have a medical emergency while travelling |

| – Trip cancellation/interruption | |

| Critical illness | A lump sum payment if you are diagnosed with a critical health issue |

| Life insurance | A lump sum payment if you pass away from natural or accidental reasons |

| Short & long-term disability insurance | Salary replacement if you become disabled and cannot work for a short or long period of time |

| Accidental death and dismemberment (AD&D) insurance | Financial assistance if you have an accidental death, are dismembered, or lose your sight or upon loss of use of limbs. This would be in addition to a life insurance payment |

How can I enroll in group health benefits?

Once hired, you need to enroll in the group health insurance plan within a deadline. If this deadline is missed, you might have to wait until the annual enrollment window is open. Typically, a new employee who joins after the enrollment period is over has to wait for a period of 30-90 days before they can get group health benefits. This period is designed to ensure a degree of commitment from the employee to the employer before benefit enrollment.

Some group health insurance plans offer supplemental benefits like dental and vision care. During the enrollment process, you can choose any additional benefits you might want and add your family members and/or dependents.

Who pays for group health insurance?

Different organizations have different rules when it comes to paying group health insurance premiums. Generally, there are three ways in which the premiums for group health insurance are paid. These are:

- Employer-sponsored plans: The employer pays the entire cost of the group health benefits plan and the employee is not expected to contribute.

- Cost sharing with employees: An employer and their employees split the premium costs at a predefined rate. Commonly used splits are50 percent each or 70 percent by the employer and 30 percent by the employee. These arrangements can differ depending on the specific plan and the agreements between the employer and their employees.

- Employee add-on costs: If employees want to add dependents or get an advanced plan with additional benefits, they have the option to pay the extra premium

How much do group health plans cost?

The cost of a group health plan varies depending on the type of package an employer purchases with options such as basic, advanced, premium offering different levels of coverage. Each package offers different coverage and depending on who is covered, the premiums can vary. For small businesses, a benefits plan can cost about 5-15 percent of the total payroll on an annual basis.

In the following table, we’ve included representative average premium costs for a group health insurance plan based on who is covered, the plan type, and coverage options:

| Coverage type | Benefits offered | Premium |

| Basic |

|

|

| Advanced |

|

|

| Premium |

|

|

What are the eligibility criteria for group health insurance?

To be eligible for group health insurance, an employee should be on the payroll of an organization. Unlike personal health insurance, group health insurance doesn’t require any medical examination or evidence. Employees are eligible for coverage based on the number of hours they work for an organization and after completing a waiting period. The plans that an insurer offers are based on the average age of employees and the industry they are working in.

What are the coverage options and limitations of a group health plan?

Although group health insurance is by far one of the most affordable, comprehensive, and inclusive types of medical insurance in Canada, it does come with some limitations. These are:

- Limited customization

- Employer dependency

- Limited portability

- Coverage gaps

- Limited portability

- Cost sharing (some costs are still paid by employees)

- Taxable to the employees

Temporary hires, independent contractors, and retirees are often not covered under group health insurance in Canada. Employees who are on unpaid leave might also lose their group health benefits until they resume work.

How does coordination work in group health plans?

Coordination of benefits (COB) is a process used by health insurance companies to determine the order in which they pay medical claims when a person is covered by more than one health insurance plan. COB ensures smooth and consistent processing of medical claims when someone has more than one health insurance plan. The primary insurer pays first, and the secondary insurer covers any remaining costs, up to the total allowed amount. COB prevents overpayment and ensures fair coverage from all insurers and also reduces costs for the members.

The rules and processes for coordinated group health insurance benefits differ from one insurer to another. It is wise to read and understand a policy document or to speak to an expert to understand coordination of group health benefits.

What are Administrative Services Only (ASO) plans?

An Administrative Services Only plan is a self-funded health insurance plan where an employer takes on the financial risk to cover the costs of the healthcare benefits offered to its employees.. Instead of paying fixed premiums to an insurer, the employer directly covers the costs of employees’ medical bills, prescriptions, and other health expenses. An employer offering an ASO plan hires an insurance company or a third-party administrator who processes claims, handles paperwork, and provides other administrative services on behalf of the employer. ASO plans offer flexibility and customization options for employers, allowing them to tailor benefits to their employees’ needs and potentially save costs compared to traditional fully insured plans. However, they also carry the risk of higher financial liability if healthcare claims exceed expectations.

Choose the right group health insurance for your employees

If you’re looking for the right kind of group health insurance plan, our licensed insurance advisors will be happy to help! We’ll ask for some basic information about your business (industry type, number of employees, claims history, etc.) and will help you find the perfect plan for your organization and employees.

Frequently Asked Questions

Who is eligible for group benefits?

All the employees of an organization are eligible for group health benefits. An employer/organization can choose to offer group health insurance to their full and/or contractual workers.

Who pays for employee benefits in Canada?

Employee benefit plans are typically offered as a perk and organizations pay the entire premium amount. However, some organizations might offer group health insurance on a cost-sharing basis.

Are group benefits mandatory in Canada?

No, group benefits are not mandatory in Canada. They’re offered as a perk in most organizations and are helpful in attracting and retaining talent.

What happens to my group health insurance coverage if I change jobs or leave my current employer?

Group benefits offered by an employer will end if you change jobs or leave an organization. However, certain benefits such as group accident insurance has portability options which means you can convert them to an individual plan if you leave your current organization.

Who is eligible for group health insurance?

An employer/organization can choose to offer group health insurance to their full and/or contractual workers.

Do employees pay for health insurance in Canada?

Employee benefit plans are typically offered as a perk and organizations pay most of the premium amount and offer these benefits on a cost-sharing basis.

Are group health plans mandatory in Canada?

No, group health plans are not mandatory in Canada. They’re offered as a perk in most organizations and are helpful in attracting and retaining talent.

What happens to my group health insurance coverage if I change jobs or leave my current employer?

Group benefits offered by an employer will end if you change jobs or leave an organization. However, if you are laid off your benefits may continue for a few weeks. In some cases, replacement coverage is also available if you apply within a certain time frame, usually between 60-90 days.

How can I get the cheapest group coverage?

To get the cheapest group coverage for your employees, you can:

- Compare different insurers and plans and choose the right coverage

- Pool your benefits plans with other organizations

- Speak to an insurance expert to build a cost-effective plan for your organization

What is the minimum size for group health insurance?

Most insurers require a minimum of two participants in a group health benefits plan.

- Group health insurance is purchased by an employer for their employees

- It is more affordable than individual health insurance plans

- Insurers typically require an enrollment rate of 70% or more

- Depending on the organization, group health insurance can be offered free of cost or the premium can be split between the employer and the employees