1-888-601-9980

1-888-601-9980What is permanent life insurance?

Permanent life insurance lasts a lifetime – literally. As long as premiums are paid, permanent insurance will remain active until you die. When that day comes, your beneficiaries will receive the policy’s death benefit. Permanent life insurance also has several options when it comes to savings and investments, which can enable you to grow and pass down wealth.

Protecting your loved ones in the event of your untimely death is serious business. That’s why insurance companies offer you so many options. But understanding those options can be a bit of a challenge. We sat down to explain one of the least understood types of life insurance out there – permanent insurance, and its various types including whole life insurance.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What is the definition of permanent life insurance?

Permanent life insurance represents a category of life insurance products that provide lifetime coverage. In other words, permanent insurance offers coverage until the policyholder passes away.

As the name suggests, permanent life insurance is best suited to protect ‘permanent’ or ‘lifelong’ needs such as estate tax liabilities, care for a disabled child or dependent, liquidity for closely-held businesses and even funeral expenses.

How does permanent life insurance work?

Most kinds of permanent life insurance policies tend to include a savings or investment component, in addition to the pure lifetime insurance coverage. Part of the premium is used to pay for investments, which accumulate within the policy on a tax-deferred basis and generate a cash value that can be accessed as needed by the policyholder.

The policyholder may use the cash value as savings available for retirement through partial or full withdrawals or by taking loans against the cash value by offering it as collateral to a lender. Due to the lifelong coverage and the embedded investment component, the premiums for permanent life insurance are much higher than other products.

Term life insurance is better suited as a strict protection product rather than an investment and planning tool.

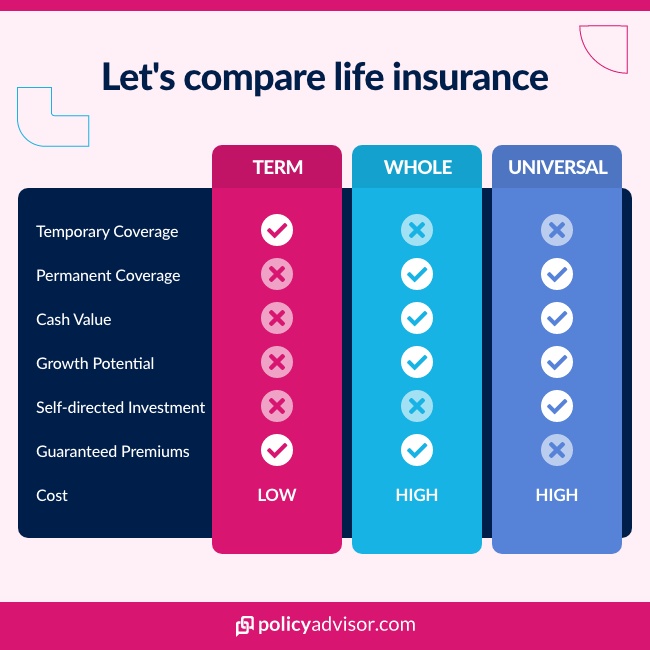

What’s the difference between term insurance and permanent insurance?

The difference between a term life insurance policy and permanent life policies is pretty easy to understand. Permanent life insurance provides financial protection for an unspecified amount of time, from whenever you start the policy until the day you die. The policy will pay the death benefit to your beneficiaries at any time you pass away as long as you have been paying the policy premiums and have not cancelled the policy.

On the other hand, with term life insurance, you are covered and benefits are paid if you pass away within a specific period of time. The usual terms tend to come in increments of ten years, although some life insurance companies allow you to pick the specific years of coverage you want.

You see – with term life insurance coverage, you pay less as you get to choose the period of your life when you feel you need the most protection; it’s a bit more nimble than permanent insurance.

Also, term insurance does not have a savings or investment component in it, a feature that is associated with many kinds of permanent insurance policies, in particular with whole life policies.

Is permanent life insurance the same as whole life insurance?

Whole life insurance, implying that you are covered for your entire life, is sometimes loosely used to refer to all categories of permanent insurance. However, there are different types of permanent life insurance Canadians can choose from. Besides whole life insurance, many Canadian companies also offer universal life insurance, term-to-100 insurance, or even variable life insurance. We cover the different types of permanent insurance in great detail here.

The most important differences between the different types of permanent life insurance products have to do with whether you want:

- To have an investment component and

- To actively manage the investment account or let the insurance company managers run with it

Read more about the differences between whole life vs. universal life insurance.

Once you understand the differences you can choose between whole life insurance, universal life insurance or term-to-100 insurance.

The advantages & disadvantages of permanent life insurance

It can feel reassuring that permanent insurance is not limited to a specific period of time – or “term.” You keep paying and it keeps covering you in return until you die.

It also has an automatic savings component. If you weren’t savvy with investing your money (who are we to judge!), permanent policies can guarantee you some growth on your excess savings.

Permanent insurance products usually build up a cash value that grows tax-deferred. If you surrender the policy at any time, the cash value (or most of it) can be returned to you.

You can use the cash value to cover any premium shortfalls if you are not able to temporarily make premium payments.

With bigger gains, come higher costs. The major drawback of permanent insurance is that the premiums tend to be much higher than those of term insurance. It stands to reason: you’re exposing the insurer to more risk by asking them to insure you for an indefinite period of time including through your riskier years, from a health perspective. Once you start paying the high premiums of a permanent insurance policy, it doesn’t feel great to let it lapse.

The returns on whole life policies tend to be modest. It may take several years for a whole life policy to accumulate significant cash value than if you invested on your own.

Most policies have a surrender charge, which is essentially a fee you will have to pay if you decide to cancel the policy and withdraw the cash value. If you surrender, there will also be income tax consequences on some portion of the returned cash value. Did you hear that? It’s the sound of your accountant shopping for a new wallet as he dreams about your next invoice.

Is permanent life insurance a good investment option?

The investment component of permanent (read whole life) policies has merits in facilitating a disciplined investment schedule, ability to access surplus cash when needed, like retirement, and tax-efficient estate transfers. While all of these sound alluring, make no mistake: the primary purpose of permanent life insurance is still protection so that your dependents have financial security when you pass away.

Permanent insurance should not be treated as a primary investment vehicle. The return embedded in such policies, while guaranteed is usually modest. The built-in management fees are higher than what fund managers may charge. There is a cost (‘surrender charge’) to accessing such cash during your lifetime.

Premiums for permanent life insurance may be better deployed in alternative investment vehicles such as RRSPs, RESPs or even to pay down your mortgage. So if you have maxed out on some of those registered products, then whole life policies can be a good place to deploy some of your surplus cash.

How can I get permanent life insurance quotes?

If you are looking to purchase a permanent life insurance policy in Canada, there are many options available to you. As the best online life insurance brokerage in Canada, we have access to permanent life insurance quotes from the best life insurance companies in Canada. Schedule a call with one of our in-house insurance brokers so you can help you find the best whole life insurance quotes from leading Canadian insurance companies.

Do you still have some questions about the different types of life insurance plans out there? That’s understandable and exactly why we wrote the Honest Guide to Life Insurance. Check it out, or jump straight into our life insurance calculator to instantly see how easy it is to protect your loved ones for less.

- Permanent life insurance offers lifelong coverage and a guaranteed death benefit when you die

- Permanent life insurance policies also come with a savings component, increasing in cash value as the policy matures.

- There are different types of permanent life insurance, including whole life insurance, universal life insurance, and term-to-100 insurance.