1-888-601-9980

1-888-601-9980How much does life insurance cost in Canada? (2024)

The cost of life insurance depends on a lot of factors. Age, gender, health, lifestyle, and smoking status influence your price for a life insurance policy. Policy type, insurance provider, and coverage amount will also directly impact the cost of life insurance premiums. In general, you can expect to pay around $10 a month for $100,000 in coverage for a 10-year term policy if you are young and healthy.

- How much does life insurance cost in Canada?

- Life insurance rates by age in Canada

- Life insurance rates by coverage amount

- Life insurance rates by policy type

- How is the cost of life insurance premiums calculated?

- What affects life insurance prices?

- How can I lower the cost of my life insurance premiums?

- Frequently asked questions about life insurance costs

Life insurance can cost anywhere from $10-70 per month on average. But it also depends a lot on your personal factors and on your policy details.

In this article, we provide specific quotes for life insurance based on some of the most common factors, like age, amount of coverage, and policy type. And, we tell you how you can lower your premium costs.

How much does life insurance cost in Canada?

The average cost of term life insurance in Canada is about $10 per month for $100,000 in coverage for a 10-year-term policy, if you are young and healthy (30-40’s, non-smoker). But, as we noted, this can change depending on a lot of factors.

We’ll take a look at life insurance premiums (the amount you pay monthly or yearly for your policy) based on the different factors below.

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

Life insurance rates by age in Canada

Age is one of the biggest factors in the cost of life policies, because it’s directly linked to your life expectancy.

Check out our life insurance rates by age charts for Canada below to see the average life insurance cost per month for someone in their 30s, 40s, 50s, and 60s.

Average Term Life Insurance Premium Costs by Age

| Age | $250K | $500K | $1M |

|---|---|---|---|

| 30 | $18/month | $30/month | $52/month |

| 35 | $19/month | $31/month | $54/month |

| 40 | $27/month | $45/month | $84/month |

| 45 | $43/month | $72/month | $138/month |

| 50 | $70/month | $124/month | $236/month |

| 55 | $125/month | $214/month | $407/month |

| 60 | $224/month | $403/month | $787/month |

| 65 | $374/month | $675/month | $1,283/month |

This quote is for a 20-year term for an individual in good health and a non-smoker, organized by gender. Please note that coverage for a 20-year term is only available up to age 65.

Life insurance rates by coverage amount

Canadian life rates vary a lot based on the amount of coverage you buy. This is how much your family would get when you pass away, and is usually the same thing as the life insurance death benefit amount.

Check out the quotes prices below to see rates for insurance by coverage amount at different ages.

Average Term Life Insurance Premium Costs by Coverage Amount

| Age | $50K | $500K | $1M |

|---|---|---|---|

| 30 | $10/month | $30/month | $52/month |

| 35 | $11/month | $31/month | $54/month |

| 40 | $12/month | $45/month | $84/month |

| 45 | $14/month | $72/month | $134/month |

| 50 | $21/month | $124/month | $236/month |

| 55 | $35/month | $214/month | $407/month |

| 60 | $58/month | $403/month | $787/month |

| 65 | $100/month | $675/month | $1,283/month |

This quote is for a 20-year term for an individual in good health, organized by gender and smoking status. Please note that coverage for a 20-year term is only available up to age 65.

How much life insurance coverage do I need to buy?

In general, you should get at least 10-15x your annual income in coverage. But, the amount you need depends a lot on your individual circumstances and needs. You should think about how much your family would need for things like:

- Your outstanding debts like student loans, credit card bills, etc.

- Your end-of-life expenses like funeral costs and other final expenses

- Future estate taxes or capital gains taxes on your assets

- Their everyday household expenses and other long-term financial goals

- Childcare costs and future education funds

- Replacing your income

- Supplementing any other existing insurance coverage

- Any other special factors unique to your family

Use our free calculator to help figure out how much coverage you should buy, or book some time with one of our licensed advisors for personal help.

Life insurance rates by policy type

Different types of life insurance policies have different premium costs. How much you pay will vary based on if you have:

- Term

- Whole (permanent)

- No-medical

- Children’s insurance

- Seniors’ insurance

- Couple’s insurance (joint policies)

- Smokers’ insurance

Keep reading to see costs for each of these below.

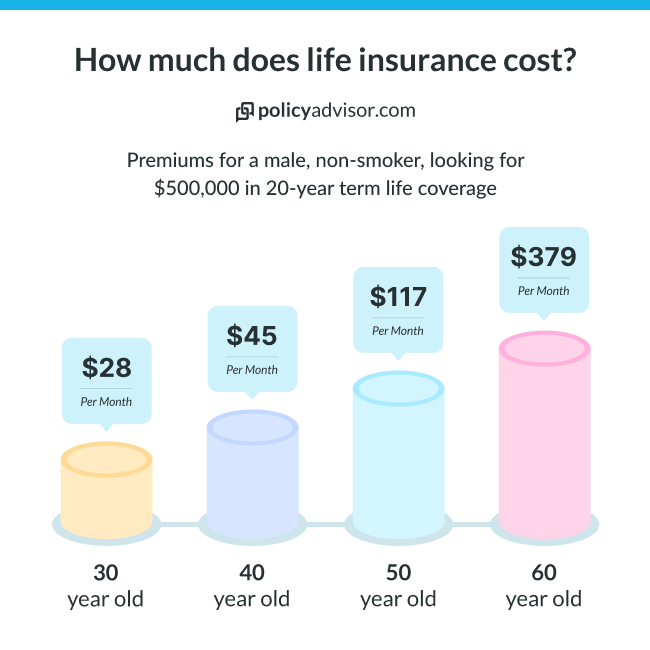

Term life insurance quotes in Canada*

| Age | 10-year term | 20-year term | 30-year term |

|---|---|---|---|

| 20 | $22/month | $29/month | $34/month |

| 30 | $22/month | $30/month | $45/month |

| 40 | $28/month | $45/month | $88/month |

| 50 | $62/month | $117/month | $239/month |

| 60 | $180/month | $380/month | Not available |

*Quotes based on $500k in coverage for a non-smoker in regular health.

Whole life insurance quotes in Canada*

| Age | $100K coverage - non participating | $100K coverage - participating |

|---|---|---|

| 20 | $47/month | $54/month |

| 30 | $65/month | $75/month |

| 40 | $92/month | $110/month |

| 50 | $149/month | $164/month |

| 60 | $245/month | $263/month |

*Quotes based on $100k in coverage for a non-smoker in regular health. Participating policies have cash value and dividends. Non-participating policies only have cash value.

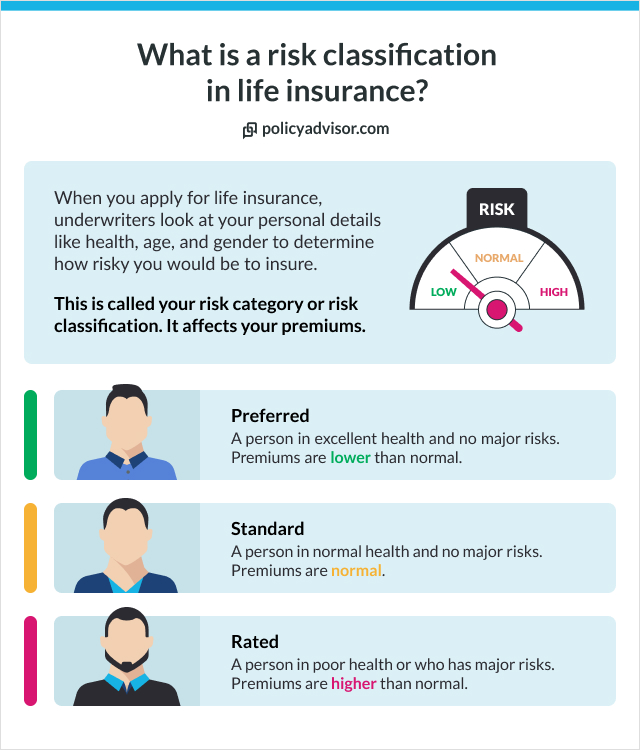

How do insurance companies calculate the cost of your life insurance premiums?

Insurance companies base your premiums on your risk profile — this is their assessment of how risky it would be for them to cover you.

- Insurance companies want to avoid risk as much as possible

- The shorter your life expectancy, the higher the chance that they will have to pay out a lot of money soon — and that’s a risk for them

- Insurers look at personal information about you and your lifestyle to gauge your life expectancy

- They then compare your life expectancy against how much you’re asking them to cover you for, and use that to decide how much it will cost you — and whether to cover you at all

What affects life insurance prices?

The key factors insurance companies look at to determine the cost of your life insurance premiums can be separated into two categories:

1. Your personal health and lifestyle

The younger you are, the cheaper your premiums will be. And, if your birthday is in less than 6 months, the insurance company will consider you to be that age instead of your current one.

Canada’s statistics shows women have a life expectancy around 4 years higher than men. This means rates for women are usually lower than for men.

As we showed above, smokers have much higher premiums because it’s not healthy. This includes marijuana, vaping, and e-cigarettes.

The healthier you are, the better your insurance rates will be. Insurance providers look at things like your weight and BMI, previous illnesses, history of drug use and more. This will affect how much you pay and what type of coverage you can get.

Some health conditions can be passed down through your family. So, insurance companies look at your family’s health history to see how likely it is you might get certain illnesses and pass away sooner than expected.

If you have risky hobbies like sky diving, race-car driving, or mountain climbing, you may be charged more. Companies may also ask if you have a criminal history.

Similarly, some jobs are considered more risky than others. Think of firefighters, police officers, pilots, and even fishermen who lives can be at risk on the job. They also have higher premiums.

If you travel a lot to high-risk countries, you may also be charged more. Or, you could be denied completely.

2. The details of your insurance policy

In general, term is the cheapest type of life insurance plan. Term life insurance policy quotes are the lowest, then whole life, and no-medical costs the most.

In many cases, a longer term costs more than a shorter term. A 20-year term usually costs more than a 30-year term. But, bear in mind that this isn’t always the case.

The more coverage you get usually means you pay more for premiums. This is why it’s important to use a calculator to make sure you’re not buying more than you actually need.

You can buy optional life insurance riders to give you more coverage, like insurance for critical illness or disability. But it will cost you a bit more.

How can I lower the cost of my life insurance premiums?

There are some ways you can lower your insurance premium.

Frequently asked questions about life insurance costs

Premiums are the amount you pay for your insurance policy. This is the same thing as your rate, price, cost, etc.

Life insurance payments can be made either monthly or annually. Most people choose monthly payments. But, you can get lower prices by switching to a yearly plan.

For permanent insurance, you also have the option to condense your payments so you only pay for a certain amount of years. This is called a limited-pay plan.

The cheapest form of coverage is term life insurance. This type of insurance policy provides coverage for a set period of time or term. So, term life insurance rates tend to be less than permanent coverage that lasts your entire life.

Learn more about the cheapest life insurance in Canada.

Preferred rates are only offered to people who have a low risk profile. This usually means they:

- Maintain excellent health

- Don’t smoke or have quit smoking

- Don’t participate in risky activities like extreme sports

- Have regular checkups

Learn more about how life insurance ratings work.

Yes, life insurance is well worth the cost. Especially since premiums are often very affordable. You get the benefit of:

- Financial security for your family

- Peace of mind in knowing that they’ll be provided for

- Reliable estate planning

- A way to clear outstanding debts

- Future college funding for young children

- A business continuity strategy

- Tax-free savings

Yes, inflation can affect life insurance rates by:

- Increasing the cost of new premiums

- Making the death benefit have less buying power

- Making your whole life cash value increase

Learn more about how inflation affects your life insurance.

© PolicyAdvisor Brokerage (PAB) Inc., is an insurance brokerage licensed to sell life insurance products in Ontario, British Columbia, Alberta and Manitoba. Not available in other provinces. Policy obligations are the sole responsibility of the issuing insurance company. Issuance of coverage is subject to underwriting by the respective insurance company. Please see policy documents for full terms, conditions, and exclusions. The logos and trademarks used here are owned by the respective entities. Refer to our Privacy Policy and Terms of Service sections for additional information.