1-888-601-9980

1-888-601-9980Using life insurance as loan collateral

You can use the cash value of your life insurance policy as collateral on a bank loan. If you default on your loan and the policy value has to be used, this will cut into your death benefit, plus interest. It may take a few years for your policy to accumulate enough value to loan against.

- Can you borrow against your life insurance policy in Canada?

- How does using cash value as collateral work?

- What are the benefits of using life insurance as loan collateral?

- What are the risks of borrowing against life insurance in Canada?

- Other ways to leverage your life insurance cash value

- What's the difference between life insurance policy loans vs collateral loans?

- When you borrow against a life insurance policy, is the loan taxed?

- FAQs About Life Insurance as Loan Collateral

Life insurance isn’t just about protecting your family after you’re gone. A certain type of life insurance builds cash value that can be the key to your next business or personal loan.

Read on to find out the types of life insurance you can use as loan collateral, how much you can borrow, and the benefits and drawbacks of using life insurance as loan collateral.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

Can you borrow against your life insurance in Canada?

Yes, you can borrow against life insurance in Canada, by using the life insurance policy as collateral for a bank loan, immediate financing arrangement, or other type of credit facility. But it only works with a permanent life insurance policy that has cash value that grows over time.

When you use your life insurance as collateral, it’s considered a secured loan. Lenders accept life insurance policies as collateral because they’re certain of its cash value and the death benefit. They’ll usually lend you anywhere from 50% to 90% of your policy’s cash value.

What kind of insurance can be used as collateral?

You can only use permanent life insurance policies that build cash value growth as loan collateral. These policies include:

Most lenders won’t accept term life insurance policies as collateral, because they don’t accumulate cash value. They also only last for a limited time — sometimes, the term is shorter than the loan repayment period. That creates a risk for the bank or lender, since it’s possible that the money won’t get paid back to them.

How does using cash value as collateral work?

Using your life insurance policy as loan collateral starts with buying an insurance policy and waiting for cash value to grow. Let’s look at the step-by-step process:

NOTE

If you’re unable to repay the loan, the lender can either cash in the insurance policy for the cash surrender value or wait until you pass away and deduct the loan amount from your death benefit.

What are the benefits of using life insurance as loan collateral?

Canadians get 3 major benefits by using life insurance as collateral for a loan:

- Your personal property and assets are safe — If you’re unable to pay back the loan, you’re not risking your home, car, or other belongings

- Loan proceeds are tax free — You pocket more of the loan amount from the bank since it’s tax-free

- You can get affordable interest rates — Secured loans mean less risk to the lender, and that means a lower interest rate for you

What are the risks of borrowing against life insurance in Canada?

While it is considered a “secure” option as far as loans go, borrowing aginst life insurance does come with some risks:

- Outliving your projected death — If you live past the date your lender believes you may pass away, they could ask for additional collateral or ask you to pay off a portion of the loan

- Interest and return rates can change — Bank loan rates can increase, or the rate of your cash value growth could decrease, leaving your cash value unable to keep up. Your lender can again ask for more collateral or early repayment in this case

- Your policy could be cancelled — If you don’t pay the loan back, the bank is entitled to your cash surrender value and your policy would be cancelled. This would leave your family without coverage, and you would have to start over with life insurance

- Your death benefit could be reduced — If you don’t pay the loan back, the bank can also deduct the amount you owe from your death benefit, or they could take the whole thing, leaving your loved ones with less money or nothing at all

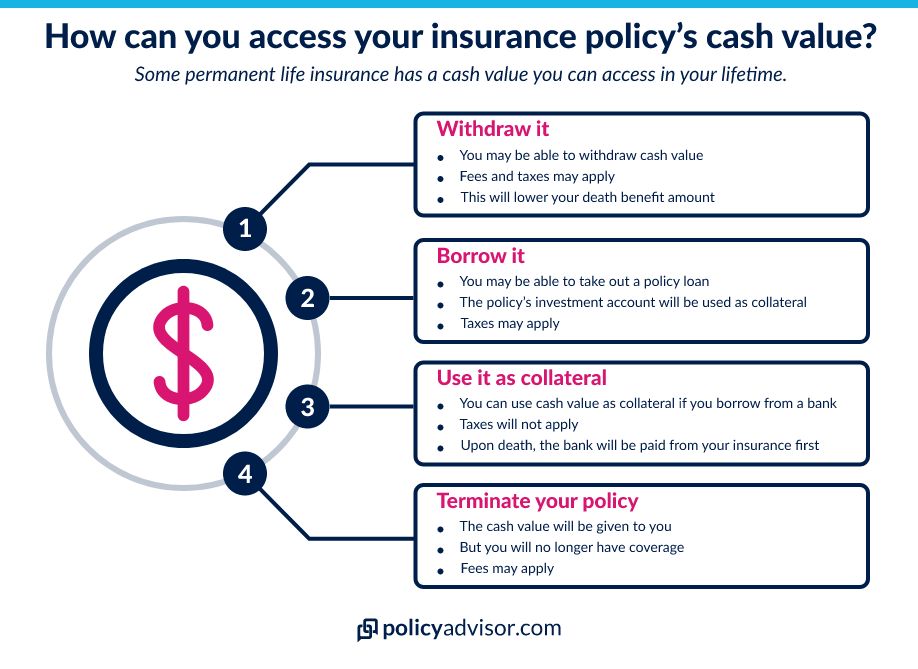

Other ways to leverage your life insurance cash value

Other than using your cash value as collateral on a bank loan, you can leverage your life insurance policy’s cash value in the following ways:

Get a policy loan

It’s possible to take out a loan on life insurance policies through something called a policy loan. This lets you borrow money from your life insurance policy, kind of like using your policy as collateral for a bank loan. But the difference is that, with this type of collateral loan, you get the money from your insurance company instead of from the bank.

You can repay this loan, so your death benefit doesn’t take a hit. This is a great option if you need cash, but wouldn’t be able to get a loan from the bank due to low credit score.

How much can you borrow from your life insurance policy?

The amount you can borrow from life insurance as a policy loan will depend on your policy’s cash value and your insurance provider’s rules. Some let you borrow up to 90% or even 95% of your cash value amount. Meanwhile, if you use it as collateral for a bank loan, you can only get 50-90% of the cash value.

Withdraw your cash value

Some policies also allow you to withdraw some or all of your cash value, for a fee. You might use this option if you need to make a large purchase and are low on funds.

There are generally penalties for early withdrawal of the cash, also referred to as the surrender fees. Your policy’s cash value minus the surrender fees is what your “cash surrender value” will be. In some cases, this penalty can be a few hundred dollars, but in other cases, it may be a percentage based on the cash value accumulated.

With policy withdrawals, the loan is final and cannot be repaid—whatever you take will reduce your death benefit. This can be an option if you’re short on cash, but you run the risk of wiping out your death benefit altogether depending on the withdrawal.

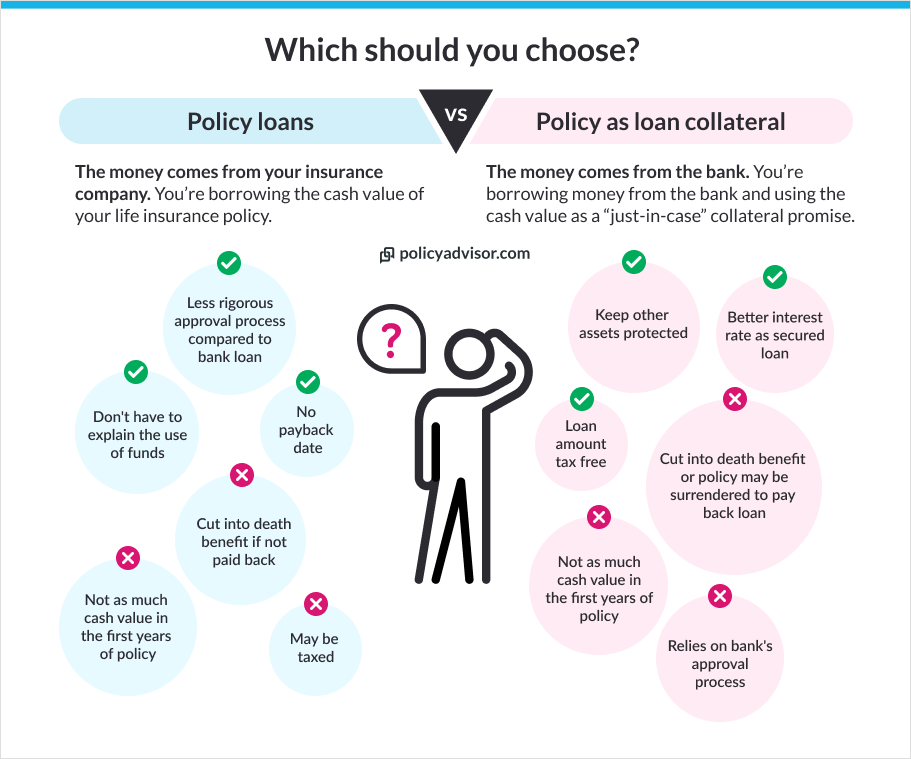

Life insurance policy loans vs collateral loans

The main difference between a life insurance policy loan and using your life insurance as loan collateral is who you’re getting the loan from.

Policy loans – The money comes from your insurance company. You’re borrowing the cash value of your life insurance policy.

Collateral loans – The money comes from the bank. You’re borrowing money from the bank and using the cash value as a “just-in-case” collateral promise.

Both options use your death benefit as a guarantee that the lender will get their money back.

Deciding which option is best for you will depend on your specific financial circumstances. While collateral loans are more secure, you may not be able to get a bank loan at all due to your credit score or other factors. In that case, a direct life insurance loan may be a better option.

When you borrow against a life insurance policy, is the loan taxed?

No. If you use your life insurance policy as loan collateral, the loan amount is tax free. However, if you take a policy withdrawal or policy loan (different from loan collateral), it may be taxed.

When determining if loans and withdrawals will be taxed, regulatory bodies look at the policy’s adjusted cost base (ACB). In the case of the life insurance policy, the ACB is what the policyholder pays for above the base cost of the death benefit coverage. This could include policy administration fees or other costs associated with the policy.

For example, if someone had a whole life insurance policy, their ACB may be calculated as follows:

Policy type — Whole life insurance

Annual premium — $5,000

Cost to cover death benefit — $1,500

Cash value investment — $3,000

Policy maintenance fee — $500

Policy ACB — $5,000 minus $1,500 = $3,500

Then, using the ACB, they determine whether the loan or withdrawal is taxable.

| Policy Withdrawals | Policy Loans | Policy as Collateral |

|---|---|---|

| Whenever the amount withdrawn exceeds the policy’s ACB, the whole loan will be taxed. | Only the amount over the ACB will be taxed. | Loan amount can be received tax-free. |

Set up your life insurance as loan collateral

PolicyAdvisor’s licensed insurance experts can advise you on which life insurance products are most suitable for using as collateral for loans, and how to maximize the benefits of using life insurance in this capacity.

Schedule a consultation with us below to explore how you can structure your life insurance to serve as effective collateral for your borrowing needs.

FAQs About Life Insurance as Loan Collateral

Generally, banks will let you borrow 50 to 90 percent of your policy’s cash value when you use it as collateral. The percentage you can borrow depends on factors like your credit score and the growth rate of your cash value over time.

For example, you may only be able to get a lower percentage if:

- You have bad credit — If you have poor credit history, a lender may be wary of lending your full cash value amount

- Your cash value grows too slowly — If your cash value growth can’t keep up with the bank’s loan interest rates, the lender may be more hesitant to approve you for the full amount

If you’re borrowing from your life insurance directly, you can generally borrow as much as 95% of your cash value.

If you find yourself unable to pay your lender back based on the terms you agreed to, they may:

- Cash in the insurance policy for the cash surrender value — Your policy will be cancelled and the bank will get your policy’s cash surrender value as loan payment

- Use your death benefit as repayment for the loan after your death — If you pass away without repaying the loan, the bank will receive the policy’s death benefit as loan payment. They may take a portion of that money or the entire amount, depending on what was owed

Your lender will tell you which option they’ll take in your loan collateral agreement.

Most major banks, credit unions, and financial institutions will accept life insurance with a cash value as loan collateral. That includes banks like:

- RBC

- Scotia Bank

- TD Bank

- And many others

Each lender will have specific requirements about the types of policies they will accept as collateral and how much cash value they require to secure the loan.

- Permanent policies let you utilize the policy’s cash value as a living benefit

- You can borrow against this cash value when you need a bank or lender loan

- You can also take a life insurance policy loan where you borrow some of your death benefit