1-888-601-9980

1-888-601-9980What is term life insurance and how does it work in Canada? (2024)

Term life insurance is a policy that lasts for a specific number of years, called a “term”. Many Canadians use term life insurance to help cover their mortgage, pay off debts, take care of young children, and more. Once your term is finished, you can choose to renew your policy, get a new policy, change it, or let it end.

- What is term life insurance?

- Key features of term life insurance

- Should I get term life insurance?

- What are the advantages of term life insurance?

- What are the disadvantages of term life insurance?

- How does term life insurance work?

- What happens when my term ends?

- How much does term life insurance cost?

- How to get the lowest term life insurance quotes in Canada?

- FAQs

Term life insurance is right up your alley if you’re just getting started with #adulting — like getting your finances in order, learning how taxes work, and thinking about whether you should start investing.

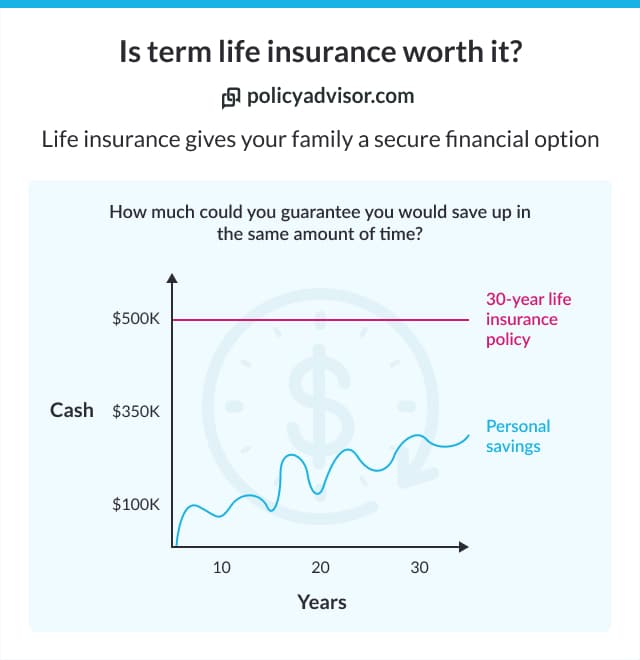

Life insurance is a great way to build a better financial future for your family. And term life insurance is the most affordable and easy option for this kind of security.

This article is your handy guide to the basics of life insurance. We explain what it is and how it works. And, we answer your biggest questions, like how much does term life insurance really cost, what happens when the term ends, whether you can get your money back, and more.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What is term life insurance?

Term life insurance is a type of life insurance that lasts for a specific period of time known as a term, which can be a fixed number of years or until you reach a certain age. This is why it’s called “term life insurance”.

Term life policies are usually offered for periods ranging from 10, 20, or 30 years to specific ages such as age 65. Some companies will also allow you to pick a term, in which case you can choose your own life insurance coverage period to meet your needs.

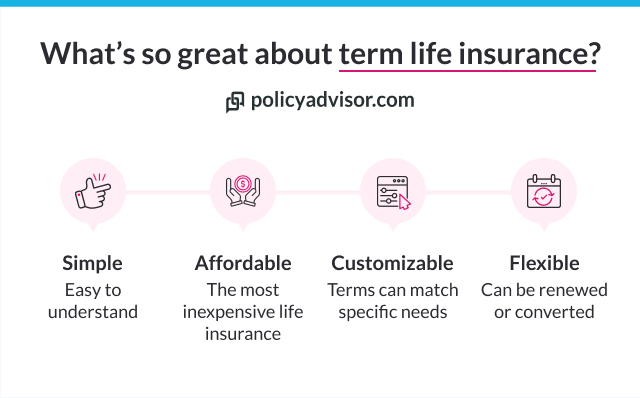

Key features of term life insurance

- Temporary

Term life insurance lasts for a specific period of time, usually 10-30 years. - Affordable

This type of policy has the lowest cost. Some policies can cost less than $20/month for young, healthy people. - Flexible

You can have a term policy for 5, 10, 20, or 30 years. Some insurance companies let you pick your own number of years too. So, you can match your term length to anything you need it to cover. - Simple

Term life insurance is very easy to understand because it doesn’t have an investment or savings component like some other types of life insurance do. - Renewable

At the end of your term, you have the option to renew your policy for another set number of years. Although, this may not always be the most affordable option. We’ll explain more later on. - Convertible

Term life insurance policies can be changed into permanent life insurance without having to take a medical exam. - Level premiums

The amount you pay an insurance company every month or year is called a “premium“. Term life insurance premiums stay the same for as long as the term lasts.

Should I get term life insurance?

You should get a term life insurance policy if you:

- Want affordable life insurance for a set number of years

- Are going through a major life event as a young adult, like getting married, having children, buying a home, etc.

- Have temporary needs like supporting a financial dependent, paying school fees, paying debts, etc.

- Have outstanding mortgage payments

- Are on a tight budget

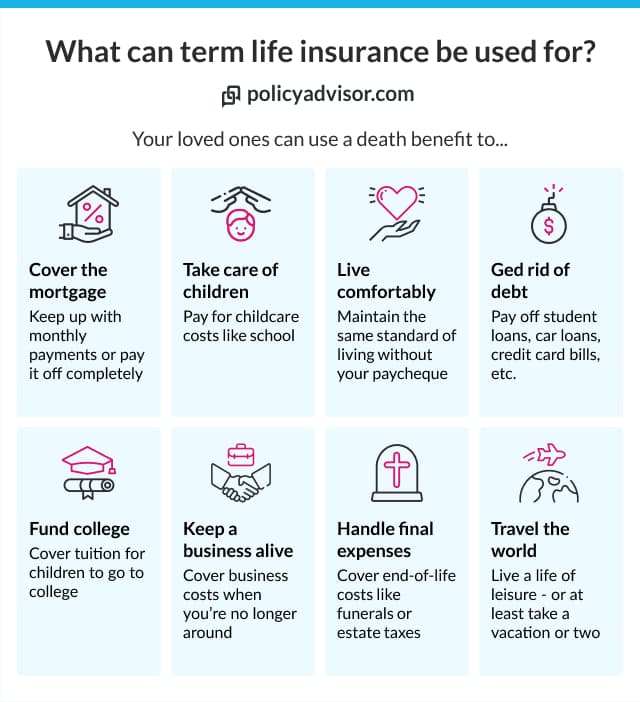

Term life insurance has many uses that can help your family cover the cost of temporary needs if you unexpectedly pass away in the near future and they don’t have your income to support them anymore.

For instance, most Canadians buy term policies to protect their mortgage or make sure young children can go to college in the future.

If you’re not sure about whether term insurance is a good plan for you, speak with a licensed life insurance broker. We’ll be able to assess your unique circumstances and give you personal, honest guidance to make the best choice.

What are the advantages of term life insurance?

The main advantages of term life policies are:

- Affordable coverage

- Simple to understand

- Flexible

- Renewable

- Convertible

- Level premiums

What are the disadvantages of term life insurance?

The main disadvantages of term life policies are:

- Temporary

- No cash value, investment components, or dividends

- Premiums increase dramatically on renewal

- Death benefit not guaranteed if you outlive your policy

How does term life insurance work?

With term life insurance, you pay a certain amount of money, called a premium, to an insurance company for a set number of years. In turn, the company agrees to give money to anyone you choose if you die within your term.

The person you choose to receive the money is called your beneficiary. Most people choose their close relatives, like their spouse, children, or parents. But you can pick a friend, business, or charity too if you want.

Let’s look at how some of the key factors of term life insurance work.

You decide the number of years you want your term to be. Most Canadians get between 10 to 30-year terms. But you can also get a policy to match a specific time, such as:

- The term of your mortgage

- Until you reach retirement age

- Until your children have graduated

- Any specific needs you have

Usually, the shortest term you can get for term life insurance in Canada is 1 year and the longest is up to 40 years. But this also depends on the provider.

Some companies won’t offer less than 5 years and some may not offer more than 30 or 35 years, especially for seniors.

You could get a 1-year term that renews every year. But this is quite expensive, so we don’t recommend it.

You can make premium payments every month or every year. Some companies give discounts if you pay yearly, so you could save up to 8%. We talk more about term life insurance premiums and show you some figures in the section on cost in this article.

You can usually get anywhere from $50,000 to $10,000,000 in insurance coverage for a term policy. It depends on the insurance company.

The coverage amount is how much money the insurance company would pay to your beneficiaries if you pass away while you have an active term life policy.

In general, the oldest age you can get a term life policy in Canada is 70 years old. It’s not a good idea to wait until later in life, though.

Insurance costs more the older you are. It also costs more if you have health concerns. It’s normal for us to develop health concerns as we age. Your premiums would be a lot higher if you wait until you’re older.

By the time you’re in your 60s or 70s, you may also not have not short-term needs. Most older Canadians have a permanent insurance policy instead of term.

What happens when my term ends?

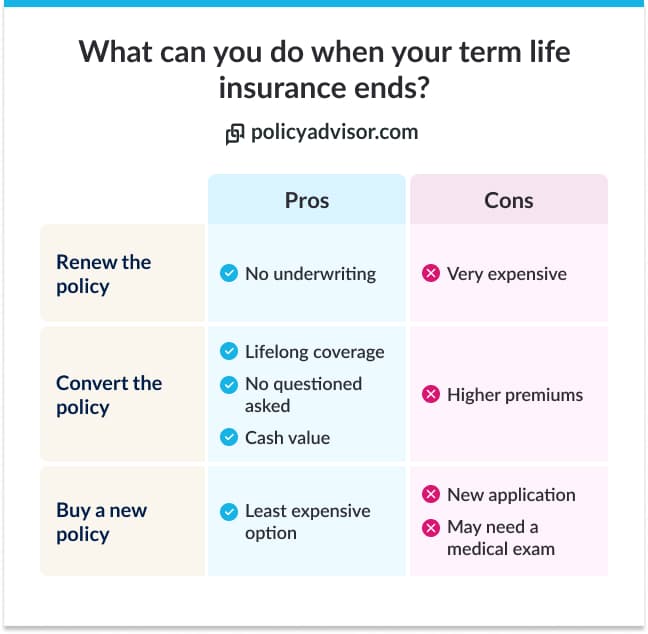

If you reach the end of your policy’s term, you have a few options:

1. Let your policy expire

You can stop paying premiums and walk away from your insurance coverage.

2. Renew your policy

If you still need insurance, you can renew for another term. We don’t recommend this because your premiums will be a lot more expensive.

The insurance company won’t ask you to do a medical exam again if you renew. So, they won’t be sure about your risk profile. Because of this, they’ll charge you more.

3. Get a new policy

This is a better option if you still need coverage. Buying a new term life policy will often cost less than if you renew your old policy.

4. Convert your policy

You could also change your term life policy into a permanent life policy. There are some rules about doing this. Some life insurance companies may ask you to wait until a few years into your policy to convert. Or before you reach a certain age.

You don’t have to do a medical exam to switch your policy from term to permanent coverage. So, it’s a good option if your short-term needs are over but you still have long-term needs.

Renewing vs converting your policy

There’s no one-size-fits-all answer for whether you should renew your term life insurance or switch to a permanent policy. It will depend on your unique situation and needs.

If you’re unsure about your options, speak with one of our licensed insurance experts. We can take a look at your current needs and help you determine which course of action would be in your best interest.

How much does term life insurance cost?

Term life insurance costs vary depending on several factors. In general, people who are young, healthy, and don’t smoke get the lowest life insurance rates in Canada.

Term life insurance products are the cheapest in the market. Premiums are often lower than it would cost you to buy a cup of coffee every day.

Take a look at the chart below to see some of the average Canadian term life premiums from some of the country’s leading companies.

Term life insurance quotes in Canada

| Age | 10-year term | 20-year term | 30-year term |

|---|---|---|---|

| 20 | $14 | $20 | $24 |

| 30 | $15 | $22 | $33 |

| 40 | $20 | $34 | $64 |

| 50 | $45 | $83 | $166 |

| 60 | $140 | $281 | Not available |

*Quotes based on $500k in coverage for a non-smoker in regular health.

What affects term life insurance premiums?

Term life insurance premiums depend on factors like:

- Age

- Sex

- Health

- Medical history (including family history)

- Smoking status

- Occupation

- Lifestyle/hobbies

- Type of policy

- Term length

- Amount of coverage

Life insurance costs less the younger you are because, in most cases, you don’t have a high risk of passing away soon. This is why it’s a good idea to sign up when you’re young, because then you can get low prices and keep that same low price for as long as your term lasts.

Policies also cost less if you don’t smoke or do risky activities like skydiving. And, they also often cost less for women because Canadian statistics show women tend to live longer than men.

Things like term length and coverage amount don’t work this exact same way. You may think that a shorter term means a lower price. Sometimes that is the case. But sometimes it may be more cost-effective to go with a longer term.

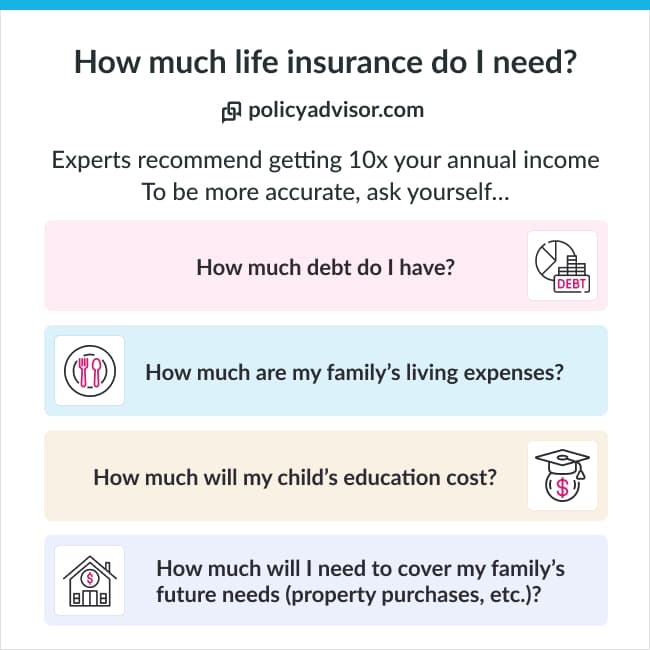

How much term insurance coverage should I buy?

A general rule of thumb is to get at least 10-15x your yearly income in life insurance coverage. But how much coverage you should buy also depends on things like:

- Your budget

- Any bills or outstanding debt that would have to be paid off

- How much your family would need to keep up with the cost of living

- Inflation

Most of us would want to leave a lot of money behind for our loved ones. But you may not really need a million-dollar policy.

The best way to find out how much term insurance you should buy is to use a life insurance calculator. We have a free one you can use to find out how much insurance you would need in minutes.

When is the best time to buy term life?

The best time to get term life coverage is when you’re young and healthy. This is when your premiums will cost the lowest. And, this is when you’re most likely to benefit from a term life policy.

The best time to buy life insurance will always be today. Your premiums will always cost less the younger you are, and you can also avoid the risk of something happening without having the coverage you need.

How to get the lowest term life insurance quotes in Canada?

If you’re ready to start checking out term life insurance options, you can get the lowest term life insurance quotes in Canada all in one place on PolicyAdvisor.com!

Our easy platform lets you compare online quotes from the best providers. This is an easy way for you to find the lowest rates and best deals.

Or, you can speak with our licensed life insurance brokers. We’re here to help, so book a call and let us help you find the lowest rates!

How can I apply for term life insurance?

You can apply for term life insurance online at PolicyAdvisor.com. Our easy-to-use platform lets you browse plans and submit an application in minutes. It’s a simple process. Just input your preferences and some information. We handle the rest!

Connect with an advisor

Compare the best term life insurance quotes on PolicyAdvisor.com. And our expert life insurance agents are happy to connect if you need some help!

We’ll answer your questions, explain everything in simple terms, and help you find the best life insurance plan for your family. You don’t have to pay a dime either! We offer personal help free of charge. There’s no obligation to buy.

Frequently asked questions

Do I have to do a medical test to get a term insurance policy?

It depends. These days, insurance companies may not ask for a medical test in many cases. They may just ask a few health questions.

In general, if you’re a Canadian citizen or resident in good health and you’re getting under $500K in coverage, you will probably not be asked to take a medical exam.

Do I get a refund if I cancel my term life insurance policy?

No, you will not get money back if you cancel a term life policy. Think of it this way: term life insurance coverage is like renting an apartment. During your “lease” term, you get the benefit of housing. When the lease is up, you walk away.

Term life policies work the same. During the term, you have the benefit of financial protection. Once the term is up, you can walk away knowing you had peace of mind for the agreed term.

What are the other kinds of life insurance?

Aside from term, the other kind of life insurance you can get in Canada is called permanent life insurance. These policies cover you for the rest of your life and have an investment component.

Some of the most common types of permanent life insurance are:

- Whole

- Universal

- Term-to-100

- Participating

- Non-participating

Most people who buy permanent life insurance get a whole life policy.

If you’re not sure which is better for you, contact us. Our friendly licensed advisors are here to help and happy to help you figure out which plan would work best!

- Term life insurance is a policy that lasts for a specific number of years

- It's affordable and easy to understand, so a lot of Canadian families get it for short-term needs

- Once your term ends, you have several options depending on your unique needs