1-888-601-9980

1-888-601-9980Different types of life insurance in Canada: choosing the right plan

In Canada, there are two main kinds of life insurance: one that lasts for a certain period (term life insurance) and one that lasts your whole life (permanent life insurance). But there are many sub-types and other options available, such as policies with cash value growth and investment opportunities. The best type of insurance for you depends on your unique circumstances, needs, and goals.

- What are the different types of life insurance in Canada?

- What is term life insurance?

- What is permanent life insurance?

- Compare the different types of life insurance policies

- What is the best type of life insurance for me?

- How do I get life insurance?

- Frequently asked questions about types of life insurance

Many people think there are only two kinds of life insurance in Canada: term life insurance and whole life insurance. It is true that most policies are either one or the other of these two types of life policies. But there are many more options and different types of life insurance Canada has to offer!

Read on to find out about your options for life insurance and types you should choose.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What are the different types of life insurance in Canada?

There are two main types of life insurance policy in Canada:

- Term life insurance, which covers you for a set period of time called a “term”

- Permanent life insurance, which covers you for your entire lifetime

All policies can fit into one of these two major categories of life insurance, which we take a closer look at in this article. But, there are many different types of coverage, based on the type of policy or type of underwriting you choose. See more below.

Types of life insurance by policy

Term

- Traditional term life insurance — the standard term policy that lasts a certain number of years. The most popular and affordable type of life coverage

- Annual renewable term life insurance (ART) — a type of policy that lasts for one year and gets renewed every year. Premium payments start low but can increase a lot over time

Permanent

- Non-participating whole life insurance — has an investment component that builds cash value over time but does not pay dividends

- Participating whole life insurance — has a cash value component and also pays annual dividends

- Universal life insurance — has an investment component that the insured person manages his or herself. Also called indexed universal life insurance policy

- Term-to-100 life insurance — a policy that lasts for the rest of your life but does not build cash value like other types of permanent coverage

- Funeral or final expense insurance — a permanent life insurance option that is designed to cover a person’s end-of-life expenses like funeral costs and also help with estate planning

Can be either term or permanent

- Joint life insurance — a type of policy that covers two people under one plan. Can also be called “survivorship life insurance” and is usually purchased by couples

- Group life insurance — a type of policy provided through your work or employer. Usually only provides term coverage up until you reach retirement age or leave the company

- Supplemental life insurance — a type of policy you can buy to enhance your group coverage, by adding additional coverage or a longer term

Types of life insurance by underwriting

- Fully underwritten policies — a type of policy where the life insurance company asks a lot of personal questions about your health, job, and more to figure out how risky it is to insure you. They might also ask you to do a medical exam

- Accelerated policies — a type of policy that does underwriting more quickly by using technology and sometimes skipping the medical exam

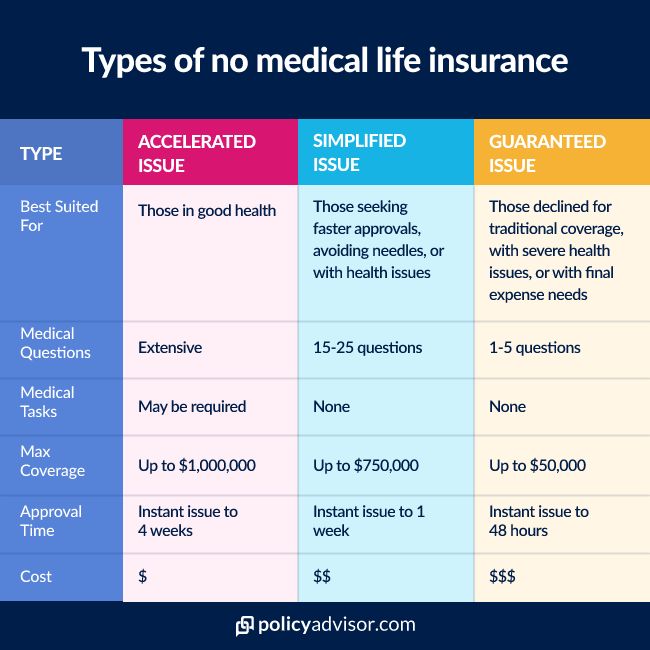

- No-medical life insurance

- Simplified issue life insurance — a life policy that only asks a few health questions and does not need a medical exam. Gives you a higher chance of being approved but at a higher cost and with less flexibility

- Guaranteed life insurance — a life policy that does not ask any health questions or need a medical exam. You are guaranteed to be approved but there are many drawbacks

Different underwriting options exist for both term and permanent types of insurance. Although, no-medical policies usually only offer lifelong protection.

Other life insurance types

While these are the major types of policies you can get from an insurance company, there are alternative options available through a bank or lender. These include:

- Mortgage life insurance — a type of life insurance that will pay off outstanding mortgage debt if you unexpectedly pass away. Benefits the lender, not your family

- Credit life insurance — a type of life insurance that will pay off eligible debt you owe if you unexpectedly pass away. Benefits lenders, not your family

We normally do not recommend this type of insurance from lenders because a life insurance policy from an actual insurance company gives you better options.

Below, we’ll do a deeper dive into the two main categories of life insurance in Canada.

What is term life insurance?

Term life insurance is the most popular and most affordable type of life insurance in Canada. It pays a tax-free, lump-sum payment to your beneficiaries if you die within the coverage period.

You can usually choose between 5 to 50 year-terms, and some companies let you customize your term length. This lets you match it to your needs, like covering your mortgage or providing future college fees for young children.

- Flexible term lengths

- Options to renew or convert your policy

- Level premiums don’t change

- Most affordable

What is permanent life insurance?

Permanent life insurance lasts for your entire life, rather than just a short time. It’s useful for long-term needs like covering estate taxes, final expenses, or more.

Most permanent life policies have an investment feature that builds cash value you can use during your lifetime. Some also pay annual dividends. You may sometimes see it called Cash Value Life Insurance.

- Lifetime coverage

- Investment component with cash value growth and dividends

- Guaranteed payout

- Options to pay policy off early (limited pay)

- Death benefit amount can increase

What is whole life insurance?

Whole life insurance is the most popular type of permanent life policy. It has most of the features of permanent policies, including:

- Lifelong coverage

- Cash value growth

- Annual dividends (participating or par policies only)

- Guaranteed payout

- Higher premiums than term insurance

What is universal life insurance?

Universal life policies are similar to whole life insurance, except you control the investment options yourself. Normally, the insurance company does it for you.

Experienced investors may use universal policies because it has the potential for a higher rate of return when they manage it themselves. But, it also means there’s a higher risk of loss.

Universal life offers:

- Lifelong coverage

- Self-directed investment component with cash value growth

- Growth potential depends on market conditions

- Guaranteed payout

- Higher premiums

- Flexible premium amounts can change

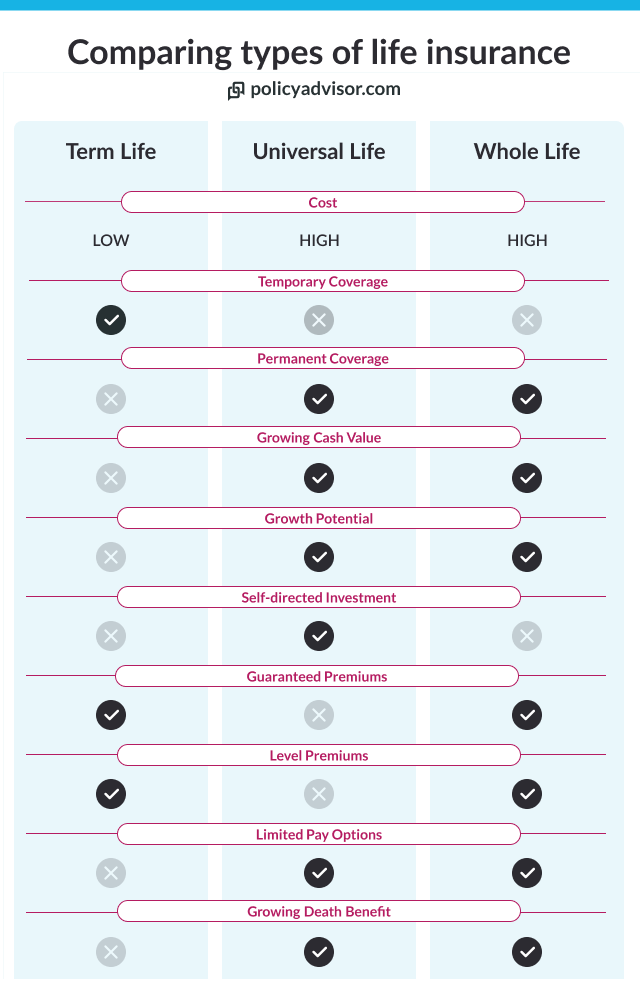

Compare the different types of life insurance policies

While all life insurance pays out a death benefit, not every policy is built the same. So how do they compare? The chart below shows how some of the most popular types of life policies compare.

What is the best type of life insurance for me?

Finding the perfect plan type can be a challenge and the answer isn’t always straightforward. In general:

If you’re not sure about your needs, connect with our licensed agents. Our clients come from all walks of life and we have years of experience working with the Canadian insurance industry. We can help you figure out what plan would be best for you!

How do I get life insurance?

You can get an individual life insurance policy by applying online using our website! Use our free quoting tool below or our life insurance needs calculator to get a customized quote in seconds.

Or, simply book some time with our life insurance experts. We’re happy to help you determine how much life insurance you need to protect your family and achieve your financial goals. Reach out and get a quote!

Frequently asked questions about types of life insurance

Term life insurance policies are the cheapest type of insurance policy. It has the most affordable premiums because it does not have investments like whole life insurance. And, the death benefit payout is not guaranteed — you can outlive your policy.

A lot of Canadians overestimate how much life insurance costs, and how low monthly premiums can be. Get personalized quotes in seconds on our website and see just how little a term life policy would cost you.

Term life insurance is the most popular type of life insurance because it’s an affordable option that can be used for a lot of different needs. Most Canadians get term life insurance for things like covering outstanding debt or providing for dependents.

You can only borrow from permanent life insurance policies that build cash value, or what some people call “cash value life insurance.” These are:

- Whole life insurance

- Universal life insurance (or indexed universal life insurance)

Permanent life insurance policies are the only ones that come with an investment component built in. You can either get:

- Whole life insurance, where the insurance company handles all the investments for you and you get modest returns

- Universal life insurance, where you handle investments yourself and get bigger potential returns — but also bigger potential losses

The main differences between term and whole life insurance is that term covers you for a certain number of years and does not have cash value, while whole life covers you permanently and has an investment component. They each have pros and cons that make them best suited for different purposes.

Learn more about the differences and which is right for you in our article on term life insurance vs. whole life insurance.

Whole and universal are both types of permanent insurance policy. The key difference between these kinds of insurance is that whole life insurance’s cash value investments are managed by your insurance provider but universal life lets you manage it yourself. With universal, your growth potential is higher, but so is your risk.

Learn more about the differences and which is right for you in our article on whole life insurance vs. universal life insurance.

Group insurance is a life insurance policy that you get through your employer, job, or other group you’re part of. On the other hand, individual life insurance is a policy you buy on your own. Some of the key differences are:

- Group policies are convenient but limited. They may not provide adequate coverage for your needs, and coverage usually is not portable — it ends when you retire or reach age 65, or if you decide to leave the company.

- Individual policies grant far more flexibility. You can customize coverage type, amount, length, and more to meet your exact needs.

- Term and permanent are the two main types of life insurance in Canada

- But there can be many more types of coverage based on type of policy, level of underwriting, and more

- The best type of life insurance for you depends on you and your family's needs