1-888-601-9980

1-888-601-9980What is whole life insurance and how does it work in Canada? (2024)

Whole life insurance is a type of permanent life insurance that covers you for your entire life. It can be used to help pay for final expenses like funeral costs or managing estate taxes after you pass away. Whole life coverage also gives you a cash value that increases your death benefit and that you can use in your lifetime. Some types are also called “participating,” and can pay you dividends in addition to the cash value.

- What is whole life insurance?

- How does whole life insurance work in Canada?

- What is cash value and cash surrender value?

- What are the different types of whole life policy?

- What are the advantages of whole life insurance?

- What are the disadvantages of whole life insurance?

- How much does whole life insurance cost in Canada?

- What are the other types of life insurance I can get in Canada?

- Is whole life insurance a good investment?

- Frequently asked questions

If you’re the kind of person who likes to cut your cake and eat it too, whole life insurance could be your perfect financial solution. It combines the peace of mind of life insurance with investments that let you pocket some extra cash while you’re still around.

Think of this article as your easy guide to understanding what is whole life policy, how it works, and how you can best use it to your advantage. Let’s take a look.

What is whole life insurance?

Whole life insurance is a type of permanent insurance that covers you for your entire life and allows you to access a part of the death benefit as cash value during your life. Some policies also pay dividends, further helping you to grow your wealth over time.

It’s the perfect coverage for long-term needs such as estate planning or leaving an inheritance for your loved ones.

Also check out our quick video on Whole Life Insurance Explained below!

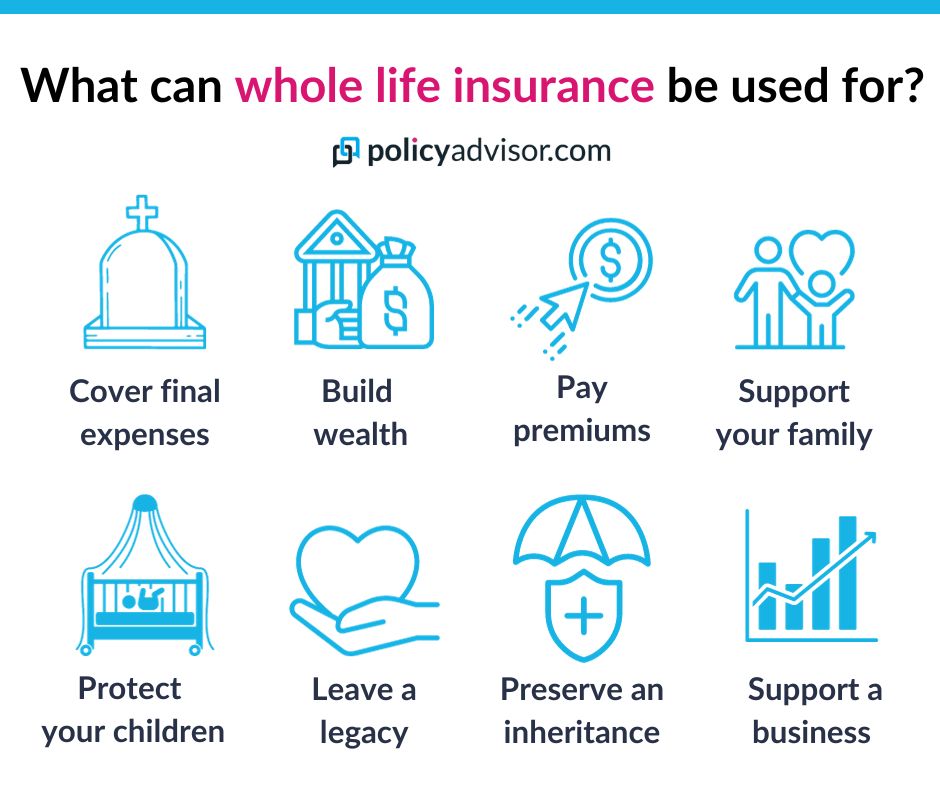

Whole life insurance can be used for:

- Cover funeral expenses

- Build wealth

- Pay premiums

- Support a family

- Protect your children

- Leave a legacy

- Preserve an inheritance

- Support a business

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

How does whole life insurance work in Canada?

Whole life coverage works like this:

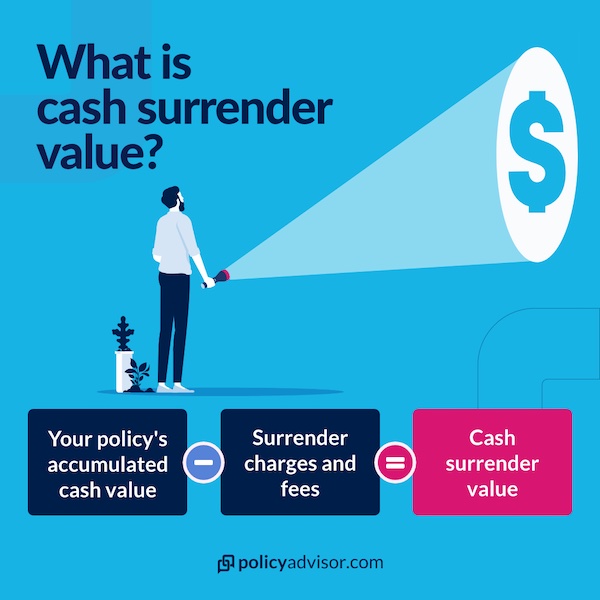

What is cash value and cash surrender value?

Cash value and cash surrender value are both “living benefits” that you can access from your whole life policy while you are alive.

Cash value is the amount of money that builds in a whole life insurance policy through the investment component. You can access this in multiple ways but only when you’re alive.

Cash surrender value is the actual amount of money you get from cash value after fees if you cancel or surrender your whole life policy.

What are the different types of whole life policy?

Permanent whole life insurance policies can either be:

What are the advantages of whole life insurance?

The main benefits of whole life insurance Canada are:

- Lifelong coverage – Your policy will never expire once premiums are paid

- Cash value – Premium payments are reinvested and grow cash value that you can access during your lifetime by borrowing against it, using it as collateral, withdrawing it, or more

- Dividends (participating policies only) – Annual dividend payments can be used to reinvest, withdraw, buy more insurance, or more

- No market volatility – The investment component is managed by the insurance company and it does not fluctuate with the market

- Guaranteed death benefit – Life insurance will pay out when you pass away no matter what

- Stable, growing death benefit – Your death benefit or coverage amount can grow over time with cash value or dividends

- Level premiums – The amount you pay will stay the same for the duration of the entire life insurance policy

- Limited pay options – Your policy can be paid off in a short time frame so you don’t have to worry about it later

What are the disadvantages of whole life insurance?

The main disadvantages of whole life policies are:

- Premiums can be expensive – Whole life policies can cost more than other types of life insurance

- You can’t choose a coverage period – You cannot select coverage for just a set period; it can only last forever

- Investment potential may not be as large as with other investments – Growth from a portfolio managed by the insurer will be moderate

How much does whole life insurance cost in Canada?

The cost of whole life insurance depends on personal factors like your age, sex, and health, and also on your policy’s details. Check the chart below for some sample quotes.

Whole Life Insurance Quotes in Canada (2024)

| Age | $100K Coverage – Non-Participating (Female) | $100K Coverage – Participating (Female) | $100K Coverage – Non-Participating (Male) | $100K Coverage – Participating (Male) |

| 20 | $42/month | $44/month | $47/month | $54/month |

| 30 | $57/month | $63/month | $65/month | $75/month |

| 40 | $85/month | $92/month | $92/month | $110/month |

| 50 | $127/month | $138/month | $149/month | $164/month |

| 60 | $202/month | $217/month | $245/month | $263/month |

| 70 | $376/month | $376/month | $462/month | $444/month |

*Quotes based on $500k in coverage on a life-pay plan. Quotes based on average prices from leading insurance companies in Canada.

What are the payment options for whole life policies?

You have several different ways and frequencies by which to pay your whole life premiums.

Case study: A whole life insurance example

Let’s look at how whole life coverage works in a case study. In this example we’ll look at John, a 30-year-old Canadian who’s thinking about estate planning. He wants a lifetime insurance policy so he can leave something behind for his family after he passes away.

The chart below shows his projected cash value over time.

Age: 30

Gender: Male

Policy type: Whole life (non-par)

Death benefit: $250,000

Annual premiums: $1,565

Payment type: Life pay (premiums paid every year for entire life)

| Policyholder age | Policy year | Death benefit | Annual premiums | Projected cash value |

|---|---|---|---|---|

| 30 | Year 1 | $250,000 | $1,565/year | $0 |

| 40 | Year 10 | $250,000 | $1,565/year | $6,210 |

| 50 | Year 20 | $250,000 | $1,565/year | $21,897 |

| 60 | Year 30 | $250,000 | $1,565/year | $48,825 |

*Figures from an insurance illustration for a Desjardins non-participating whole life insurance policy purchased through PolicyAdvisor.com for a 30-year-old male in normal health.

Remember, John can use the cash value from his policy to build up his savings while still making sure his family would have enough money to carry on when he’s no longer around.

What are the other types of life insurance I can get in Canada?

If you’re looking for alternatives to whole life insurance, these are the other types of life insurance that you can get in Canada:

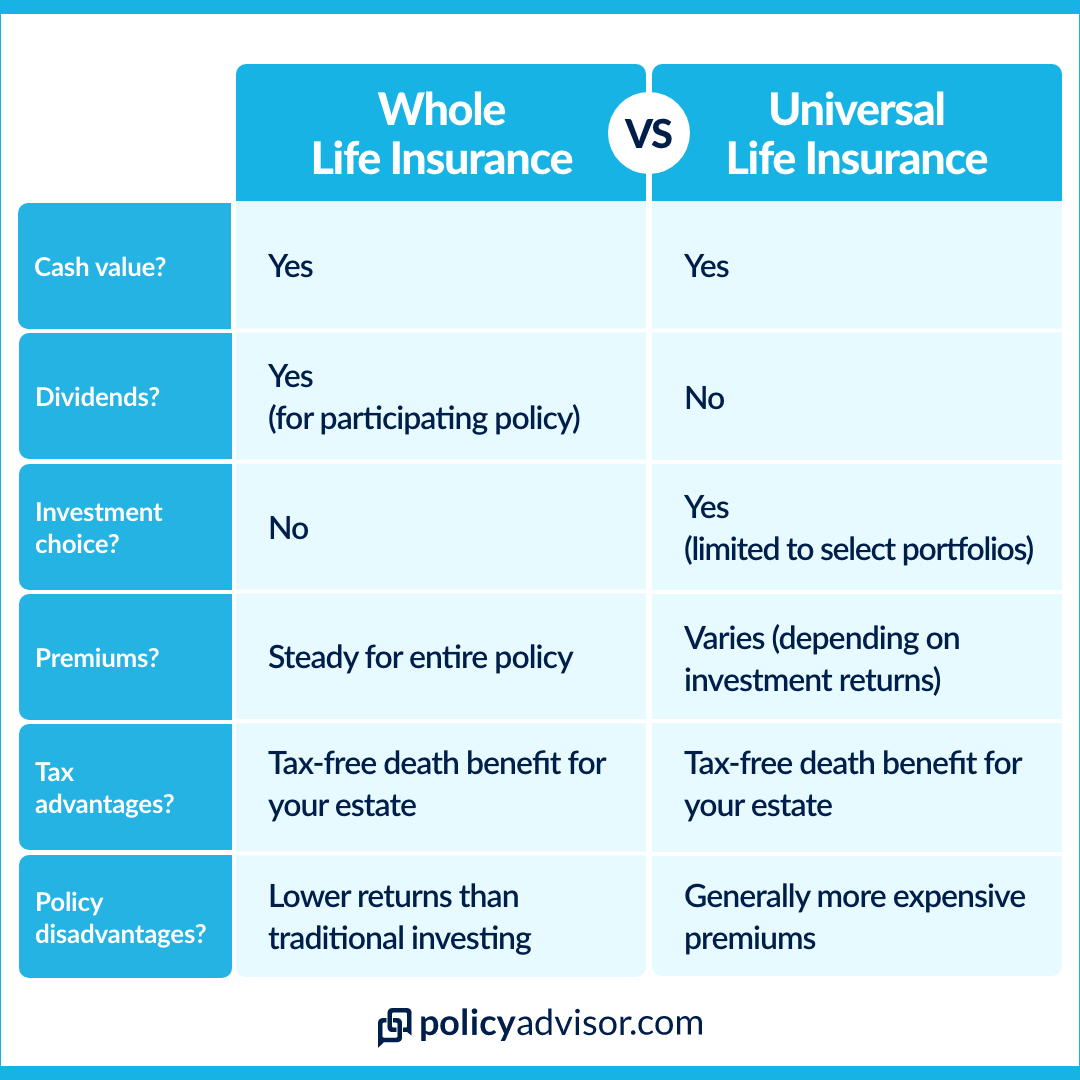

What’s the difference between universal and whole life insurance?

Universal and Whole are both types of permanent life policy. But one of the main differences between a universal policy and a whole life policy is that universal gives you more control over your investments. This means it has greater growth potential, but it’s also more risky.

Learn more about it in our article on Whole Life vs Universal Life Insurance.

Is whole life insurance a good investment?

We do not recommend buying life insurance exclusively as an investment strategy. Its purpose is to provide lifelong protection and financial security your family can rely on, not to provide capital gains.

The average rate of returns for whole life insurance varies, but is usually around 2-4% per year. This is not bad. But, if you’re only looking for an investment vehicle to generate high returns in a short amount of time, you would be better off with other options.

Should I buy whole life insurance or put my money into savings?

If you’re wondering whether you should buy whole life insurance or put the money into savings, a whole life policy is a much safer bet. Here’s why:

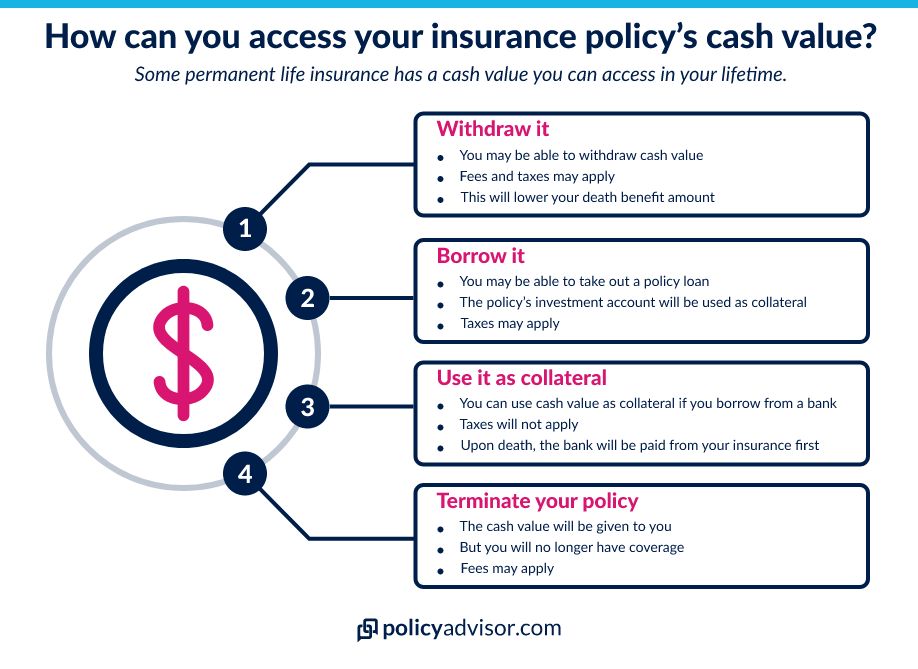

What happens if I surrender my whole insurance policy?

You can surrender your policy by ending it at any time. In that case you would get the cash surrender value and no longer have coverage. You may have some options to change your coverage into a policy with a lower death benefit, or to a term life policy.

But it depends on your provider — you should ask your insurance advisor about your options.

How soon can I cash out my whole life insurance policy?

It depends on your provider. Most Canadian companies will let you access your policy’s cash value on the anniversary after 5 or more years. This is whether you want to withdraw it, borrow against it, or access it any other way.

But you may want to wait. The longer you let whole life insurance cash value accumulate, the bigger the amount you can use and the more benefit you can have.

How much can I borrow from a whole life policy?

You can normally borrow up to 90% of your policy’s cash value if you want to take out a policy loan directly from your insurance provider. If you want to borrow from a bank or lender and just use your policy as loan collateral, you can borrow up to 100% of the premiums you paid.

Speak with an advisor

If you’re not sure whether whole life coverage may be right for you, contact us! Our licensed insurance advisors are happy to assess your needs and help you compare options to make the most informed choice.

Book some time with us to see what your coverage options are and if whole life insurance coverage is right for you.

FAQs about whole life insurance

Find the cheapest whole life insurance quotes online using our free quoting tool. Our platform scans the market in seconds to show you your best life insurance match instantly.

You an also check out our listing of current life insurance promotions in Canada. Or book a free consultation call with one of our licensed advisors.

It usually takes years to build up a substantial amount of cash value — anywhere from 10 years or more. You can also help speed things up by paying more into the policy.

Alternatively, some policies are made to help you build cash value as quickly as possible. UV Insurance Company is a great example of this with their Whole Life High Values permanent policy.

Yes, you can add life insurance riders to a whole life insurance policy. It just depends on what your insurance provider has available, but you can get:

- Term rider

- Child rider

- Accidental death & dismemberment benefit rider

- Guaranteed insurability rider

- Return of premiums rider

- Critical illness rider

- Disability waiver of premiums rider

- And more

It depends, but a medical exam is not needed in many cases. In general, if you’re a Canadian citizen or resident in good health and you’re getting under $500K in coverage, you will probably not be asked to take a medical exam.

The relationship between tax and whole life insurance can be looked at from a different angles. In general:

💸 Non-taxable

- Death benefit payout

- Dividends — if reinvested in the policy

- Policy loans proceeds — if below the adjusted cost basis

- Third-party collateral loans using the cash value

🏦 Taxable

- Cash dividends

- Policy withdrawals above the adjusted cost basis

- Policy loans above the adjusted cost basis

There are many scenarios that can apply, so you should be sure to speak to a licensed insurance advisor or a tax professional to find out what applies to you.

No, you cannot use your insurance policy to become your own bank.

You may have seen this claim on social media platforms like TikTok, where some people claim you can use whole life insurance for “infinite banking.” But if something seems too good to be true, it usually is.

The concept of “infinite banking” does exist, but it’s very complicated. And it doesn’t work the way some catchy videos suggest.

- Whole life insurance covers you for your entire life

- Whole life insurance gives you a guaranteed and growing death benefit, and living benefits you can use during your lifetime

- Premiums depend on personal and policy details