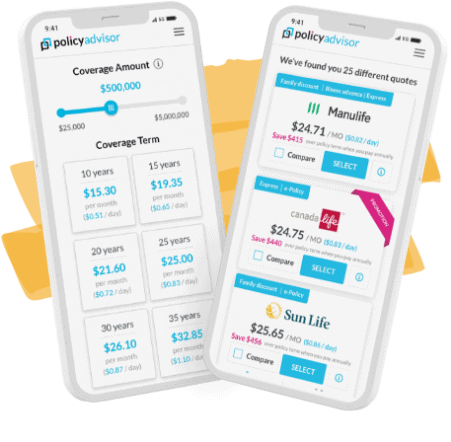

Compare & Buy Canada’s Best Term Life Insurance

Lowest quotes from Canada's 30 best insurers

Trusted by Canadians

Trusted by Canadians

99% of customers recommend us

I'd previously reached out to one of the big insurance companies directly but found them so unresponsive and uninterested. I'm glad we found PolicyAdvisor. They made comparing options easy so we found something that worked…

They are the Gold Standard of Client Experience. The whole process was simple, hassle-free, uber transparent and all of this at no cost. Our advisor’s knowledge and attitude reeled us in from the first call. We felt as if…

Very knowledgeable and helpful in determining the best plans for my son and I and he took the stress out of the process. Fully explained all of the options available to me, and answered all of my questions. I know that I…

What is term life insurance?

Term life insurance is a type of life insurance that lasts for a specific period of time, which can be a fixed number of years or until you reach a certain age. You pay a level premium to the insurance company until the expiry of the term.

In return, your beneficiaries are entitled to receive a tax-free, lump-sum death benefit if you die within the term of the policy. Once the term ends, your coverage also expires and you can stop paying premiums.

The term in term life insurance refers to the exact time period you are covered.

Some typical terms are:

Additionally, some insurance providers let you pick your own term between 5 and 40 years that best suits your needs. These are all examples of level term policies where the death benefit and monthly premium remain the same through your chosen term.

Lastly, there are specific term policies for unique applications:

How does term life insurance work?

Term life insurance is a contract between you (the individual being insured) and a life insurance company (the insurance provider you choose). The insurance company agrees to make a lump sum, tax-free payment to a beneficiary should you (the insured individual) die during the entire term of the policy.

Life insurance providers use detailed statistics and actuarial models in the application process to determine the premiums for this coverage. Premiums are the monthly or annual fees you pay to ensure your policy is in force. Insurance companies use this data to assess life expectancy and the likelihood they will have to pay out the full death benefit. If the likelihood is higher, the premium rates are higher. If the likelihood of a payout to your beneficiaries is lower, the premiums are lower (or you may even qualify for preferred rates).

A beneficiary is a person (or people) the policyholder chooses to receive their death benefit. While they are typically a spouse, partner, or children, the beneficiary can be anyone you choose, including charities or trusts.

In some cases you may need to go through a medical exam to qualify for your term life insurance policy, but there are no-medical insurance options for those who wish to skip medical underwriting.

Unlike other types of life insurance, term policies hold no cash value or savings component. This is one of the reasons why term life insurance is one of the most cost-effective insurance plans for Canadians.

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them.

What does term life insurance cover?

A term life insurance policy can cover any expense or lost income that disappears when an insured individual dies.

For example, the death benefit from term life insurance coverage can pay mortgage payments, outstanding loans and credit card debt, children’s education costs, income replacement, cost of living expenses for dependents, and funeral costs and expenses.

The lump-sum payment from a death benefit can be used however the beneficiary chooses to help them grieve or retain their quality of life after the loss of your income.

Does term life insurance cover accidental death?

Simply put, term life insurance pays out for most causes of death and does not differentiate between natural death, one due to terminal illness, or accidental death.

With that in mind, it is important to know that some policies contain exclusions for life insurance payouts. These exclusions can include deaths that occur in certain restricted geographic locations, if it’s discovered you lied on your application, if the death occurred during an illegal activity, and others.

Learn more about if life insurance pays out for natural death

Does term life insurance cover disability?

Term life insurance policies do not cover disability by default. You can add disability riders to many insurance policies to cover circumstances where you are injured or ill and are no longer able to earn an income. For more robust disability coverage, you can purchase an individually owned disability insurance policy that can be tailored to your needs and income level.

How much does term life insurance cost?

The cost of a term life insurance policy depends on personal factors and the details and depth of your desired coverage. Age, smoking status, and health are some of the biggest personal determiners of the cost of a term life policy.

A term policy is less expensive when you are younger, non-smoking, and in good health. Generally, term life insurance costs less than permanent policies. While we can’t give you a one-size-fits-all premium payments cost here for different amounts of coverage, an experienced advisor (like us) can help you find the best coverage within your budget. You’re in the right place to find affordable life insurance to secure your dependents' financial future!

Pro tip: You can save on insurance coverage if you opt for annual premiums: paying your premium yearly instead of once a month. The annual cost can be 10-15% lower than if you pay your premiums monthly. Ask your advisor about it!

Get complete details about the cost of life insurance in your 20s, 30s, 40s, and 50s.

| Age | Male | Female |

| 25 | $31 | $22 |

| 35 | $33 | $26 |

| 45 | $75 | $54 |

| 55 | $223 | $155 |

| 65 | $716 | $487 |

Term life insurance premiums, $500,000 death benefit, non-smoking, 20-year term

What happens after your term life insurance ends?

Depending on your policy, you may have four options for how you proceed with coverage when your initial term life insurance policy ends.

What to do when your term life insurance expires?

1. Let your coverage lapse: If you decide you no longer need life insurance coverage, you can let your policy expire and go on without an active policy

2. Renew your coverage: If you opted for renewable term life insurance coverage with your current provider, you can renew coverage without a medical exam or medical questions - but at a higher premium

3. Convert your coverage: You may also have the option for convertible term life insurance - turning your current coverage into a permanent life insurance policy

4. Get a brand new life insurance policy: If you are at the end of your term and still need coverage, applying for a brand new term or permanent policy may be the least expensive way to continue your coverage

Learn more about what to do if you outlive term life insurance

What’s the difference between term life insurance and whole life insurance?

Term life insurance and whole life insurance are different ends of the protection spectrum. While we’ve already described term life insurance’s temporary nature, whole life insurance offers coverage for life. It is a lifelong policy and is in force as long as your policy premiums are paid.

While term life insurance provides coverage for temporary needs like diminishing mortgage debts and providing for dependents, whole life (or permanent) insurance can provide for permanent needs and cover you for your entire life. This can include providing for final tax expenses, funeral arrangements, or leaving a tax-advantaged legacy behind for children or grandchildren.

Read more about term versus whole life insurance or other types of life insurance like universal life insurance and term-to-100 insurance.

Frequently asked questions

Is there a catch with term life insurance?

There’s no catch or “gotcha” moment with term life insurance products. It’s a straightforward, affordable type of insurance that maximizes the amount of financial protection you can purchase while sticking within your budget.

Can you renew a term life insurance policy?

Almost all life insurance companies offer renewal options as one of the benefits of term life insurance policies. For example, if your term life policy is for 10 years, the coverage automatically renews at the end of the term for another 10 years, unless you specifically cancel your coverage. However, the renewal is subject to a higher premium (and many Canadians can still get approved for a lower premium by applying for brand new coverage).

Most companies allow for renewal of the policy up to a certain age, such as 70 or 75 years old. Once you reach that age, the policy can no longer be renewed and the coverage expires.

Who offers the best life insurance policy in Canada?

PolicyAdvisor helps Canadians find the best life insurance policy for their needs. But let’s be frank. There is no best insurance provider. There is – however – the best insurance provider for you.

The country’s top insurance companies offer unique policies to fit every Canadian’s individual coverage needs. What helps is having the choice and knowledge to pick the policy and provider that’s right for your situation.

That’s why PolicyAdvisor partners with 20+ of Canada’s top insurance companies – the most by any online broker. We make sure you have the greatest number of options when choosing the insurance company to protect yourself and your loved ones. We can help you obtain a life insurance plan from Assumption Life, BMO Insurance, Canada Life, Canada Protection Plan, Desjardins, La Capitale, Empire Life, Equitable Life, Foresters, Humania, iA Group, ivari, Manulife, RBC, Sun Life, SSQ, and Wawanesa.

When is the right time to get term life insurance?

As mentioned above, the main factors by which all life insurance providers determine their premiums are age and health. Considering those criteria, the earlier you apply for life insurance coverage, the better! Applying while younger is also advantageous as it is less likely any health conditions have affected you, which would further drive up the cost of your premiums.

Can I cash out term life insurance?

No, unlike permanent life insurance, term life insurance holds no cash value or surrender value. This is one of the reasons why term life insurance is less expensive than permanent life insurance options and a more cost-effective method of financial protection.

Do you get your money back at the end of a term life insurance policy?

No, you do not get any money back at the end of a term life insurance policy. Your coverage expires and you are no longer required to pay premiums. You can think of term life insurance as insurance that you lease for a temporary need, instead of paying extra to own the policy permanently.

How much term life insurance do I need?

A common rule of thumb is to choose 8-10 times your annual income as your death benefit. For a more precise answer, take into account any debts you have, your family's living expenses, future education needs of your children, plan for end-of-life expenses and any other allocations (for example, charitable donations) you may want to make. Head to PolicyAdvisor’s Life Insurance Calculator to get the most accurate estimate for your life insurance plan and needs.

Do single parents need life insurance?

Anyone with dependents or loved ones needs life insurance, but due to their circumstances single parents often bear a greater responsibility in the raising and protection of their children and that extends to life insurance and financial protection.

Can I insure my loved ones, like a spouse, parents, or children?

Yes, you can buy insurance for your loved ones but not without their consent or without their knowledge that their life is being insured. The only exception would be in the case of children below the age of consent where you are their legal guardian. In short, we’ll need to speak to anyone you intend to insure - including your loved ones.

Learn more about purchasing a life insurance policy for someone else.

Can I get an insurance policy, even if I have health problems?

Health problems don’t necessarily preclude someone from purchasing life insurance, but they will most likely affect the price of premiums. Depending on the nature of your ailment, when it was diagnosed, and how it currently affects your health, our experienced advisors can help review coverage options and match you with a life insurance company with policies tailored to your situation. Our in-house insurance advisors help our clients apply for simplified non-medical insurance policies or guaranteed non-medical insurance coverage, wherever those are the best options for clients. Our expert advice is available whenever you need it.

How long should my term life insurance last? Should I get term 10, term 20, or term 30?

How long your term life insurance policy lasts should correlate with your life insurance needs.

A 30 year term life insurance policy can help cover a new mortgage. A 20 year term life insurance policy can provide financial security for a new family. A 10 year term life insurance policy can be used by a senior to cover final expenses or replace income for those they leave behind. You have the flexibility with online term life insurance to choose the length of policy you need, like those above, or other term lengths like 25 year term life insurance, 40 year term life insurance, or something in between.

How does PolicyAdvisor find the lowest rates for term life insurance Canada has to offer?

PolicyAdvisor represents the most insurance carriers of any digital brokerage, and thus can ensure you find the lowest priced term life policy for your needs and budget. You can shop for rates from 25 of the country’s best life insurance companies.

How do I compare quotes & apply for term life insurance?

This is an easy one. Click here to compare term life insurance rates and apply for the coverage you need in minutes!